- South African prices hit four-year lows

- Domestic prices unchanged on weak buying

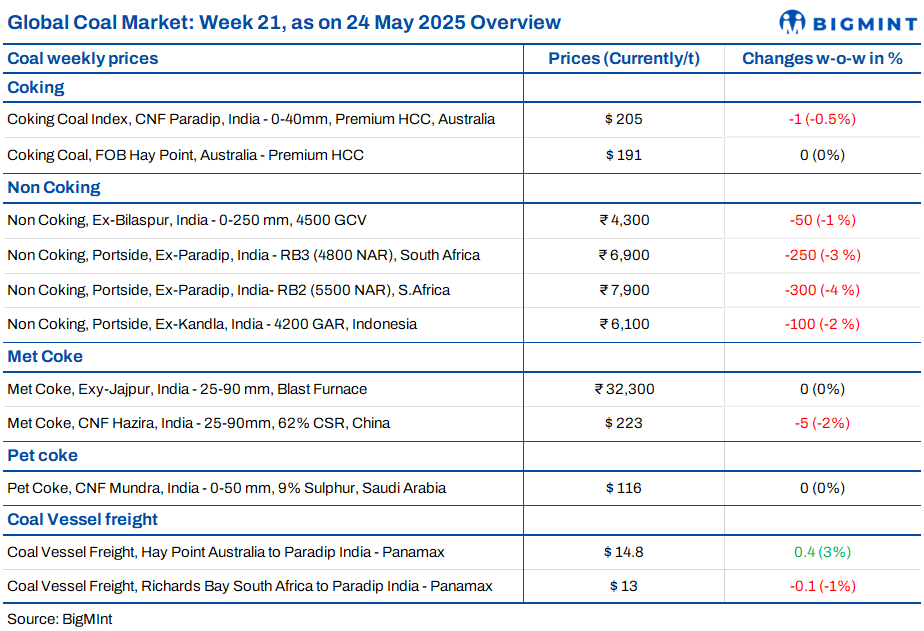

India’s coal market sentiment remained largely bearish this week, driven by weak demand across key regions, ample domestic coal availability, and cautious buying behaviour. Portside prices of both South African and Indonesian thermal coal continued to fall, hitting multi-year lows at some Indian ports. Despite steady freight rates and a slight decline in inventories, the overall outlook stayed muted. Market participants refrained from fresh bookings, awaiting clearer signals on demand recovery or further price corrections in the near term.

Indonesian portside prices fall on weak buying, rising supply

Portside prices of Indonesian thermal coal in India dropped w-o-w due to bearish sentiments, rising vessel arrivals, and weak demand. At Kandla, BigMint assessed 5000 GAR to be down by INR 50/tonne (t) to INR 7,750/t, while the 4200 GAR fell by INR 100/t to INR 6,100/t and to INR 6,000/t at Vizag. The 3400 GAR slipped by INR 50/t to INR 4,500/t at Navlakhi. Coal inventories at ports dropped to 14.62 mnt. Rainfall and minor port closures further curbed movement. Indexed prices also declined globally, led by a $1.18/t fall in 4200 GAR material. The market outlook remained subdued.

South African prices at 4-year lows, weak buying persists

South African thermal coal prices at Indian ports fell again w-o-w amid muted buying. RB2 (5500 NAR) dropped by INR 350/t to INR 7,900/t exw-Gangavaram, while RB3 (4800 NAR) declined by INR 250/t to INR 6,900/t. Paradip RB2 prices reached a four-year low. Inventories fell 2.2% w-o-w to 14.62 mnt. Export offers slipped by $1/t.

Sponge iron prices were also down by INR 200/t to INR 25,100/t in Rourkela, putting further pressure on buying interest. The market outlook was uncertain amid weak demand as sponge players are the largest buyers of South African thermal coals.

Domestic prices unchanged amid weak buying interest

Domestic coal prices in India held steady this week as demand remained subdued. The 4500 GCV grade was assessed at INR 4,350/t, while the 5000 GCV stood at INR 4,800/t exw-Bilaspur. Buying activity stayed weak due to sufficient supply and lower offtake from non-power sectors. Additionally, direct supply to power plants through auctions has limited open market demand. SECL’s spot auctions held on 22 May witnessed weak response, with just 0.19 million tonnes (mnt) of coal getting allocated. With no major buying triggers, prices are expected to stay range-bound in the short term.

Met coke prices stable on sluggish steel demand

Met coke prices held steady this week across key regions, with blast furnace-grade (25-90 mm) assessed at INR 32,300/t ex-Jajpur and INR 31,000/t exw-Gandhidham. Despite a $9/t rise in Australian coking coal since mid-April, coke prices in India were under pressure on weak steel demand. BigMint’s India Steel Composite Index fell 0.6% w-o-w, with pig iron prices also declining in the recent auctions.

Pet coke prices stable as demand stays weak

Imported pet coke prices remained unchanged this week with US-origin material assessed at $100-102/t CFR for both eastern and western India. Buying interest was muted as lower domestic prices, following price cut announcements by IOCL and BPCL for May, kept demand for imports subdued. Meanwhile, offers for Saudi-origin cargoes held firm at $116-118/t CFR. Market activity was limited, reflecting ongoing weak demand signals and steady availability.

Freights steady amid weak fixtures, mixed trade cues

Coal freight rates to India remained largely stable this week as steady power and industrial demand offset weak cargo volumes and cautious sentiment. Panamax freights from Australia rose $0.4/t w-o-w to $14.8/t, while South Africa-India rates dipped slightly by $0.1/t to $13/t on reduced enquiries. Supramax rates were flat as Asia-Pacific demand stayed weak. Baltic indices showed mixed trends, with BPI falling and BDI rising. Overall, limited fixture activity and cautious chartering kept rates in a narrow range across key routes.

Leave a Reply