- Longs prices hold steady despite weak demand

- Chinese, Indonesian NPI prices decrease

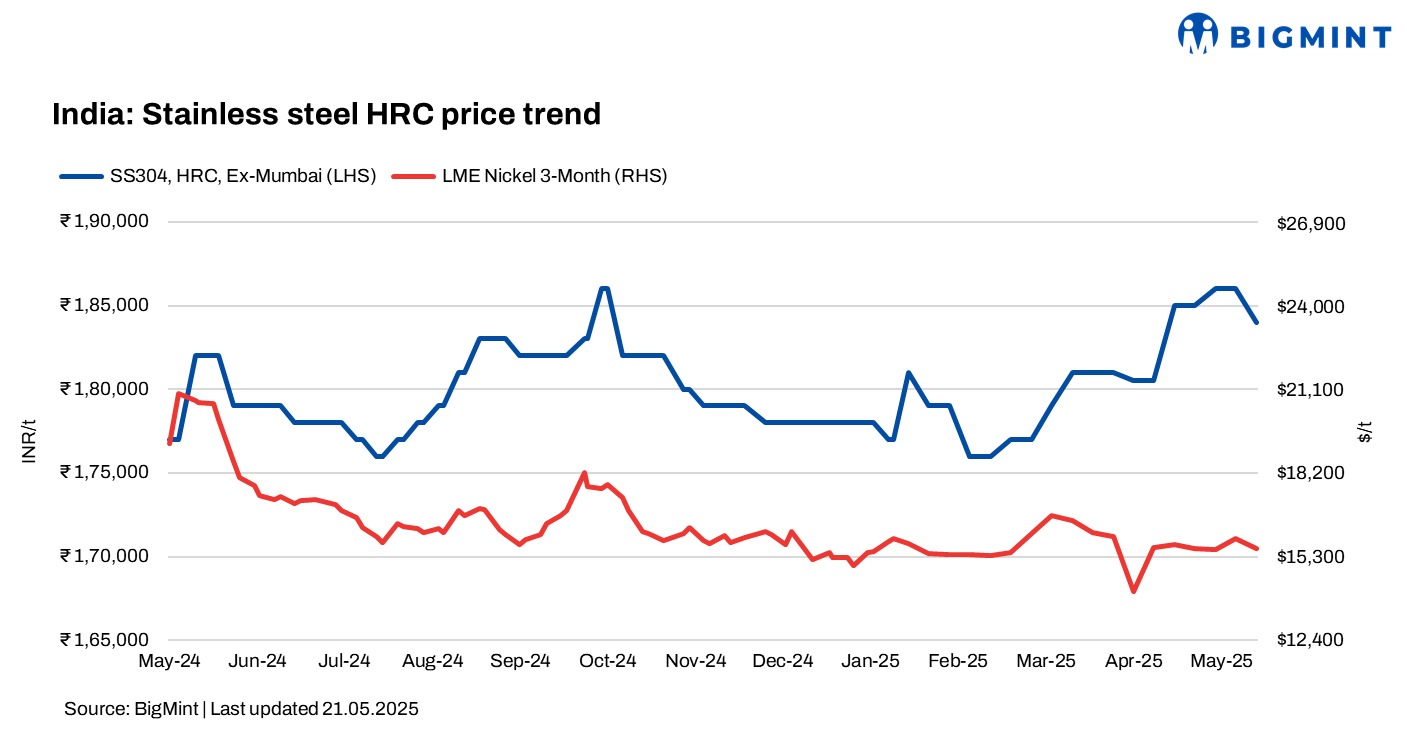

India’s stainless steel (SS) finished flats prices dropped slightly by INR 2,000/t w-o-w while longs prices remained stable this week amid persistent weak demand.

BigMint’s benchmark assessment for stainless steel 304 series hot-rolled coils (HRCs) dropped by INR 2,000/t to INR 184,000/tonne (t), while 304L (25-100 mm) black round bars stood at INR 160,000/t, both ex-Mumbai.

LME nickel tags dip, Asian NPI falls w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,605/t, down 2.1% against last week’s $15,940/t. Nickel stocks in LME-registered warehouses stood at 202,098 t, a 2% drop compared to 197,754 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) stood at RMB 945/metric tonne unit (mtu) ($131/mtu). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $114/mtu.

Market insights

Additionally, as per BigMint’s assessment, SS 316 HRCs stood at INR 323,000/t, down INR 2,000/t and 316 cold-rolled coils (CRCs) at INR 331,000/t ex-Mumbai, stable w-o-w.

According to market participants, “Infrastructure and project-based activities are advancing slowly. As the rainy season begins, market activity generally declines further, resulting in a quieter and more subdued trading environment.”

Meanwhile, SS 316L black round bars were priced at INR 270,000/t, while 316L (25-100 mm) bright bars were at INR 286,000-288,000/t, both ex-Mumbai. Furthermore, SS 304 (5-16 mm) wire rods stood at INR 156,000/t ex-Mumbai. Prices of all products were steady w-o-w.

Other updates

US stainless steel CRC prices surge amid supply shortage

As of mid-May, the US stainless steel cold-rolled coil market faces a significant supply crunch, pushing prices higher. A recent 25% tariff on foreign metals has restricted imports, straining local producers amid rising demand from construction and manufacturing. Meanwhile, Germany and China maintain stable prices and balanced supply, but US prices are expected to remain bullish due to ongoing tightness and robust end-user demand.

South Korea extends anti-dumping duties

South Korea’s Ministry of Economy and Finance has extended anti-dumping duties on flat-rolled stainless steel (≤8mm thick) from China, Indonesia, and Taiwan for five more years, effective 16 May, 2025. While most exporters face duties up to 25.82%, several major companies are exempt due to price commitments. Additional exemptions apply for specific high-grade or specialised stainless steel products.

Chinese stainless steel prices up

In China, prices of domestic stainless steel 304-grade cold-rolled coils (CRCs) stood at RMB 13,950/t ($1,936/t) exw, up by RMB 100/t ($13/t) w-o-w, while FOB tags of 304-grade CRCs were at $1,910/t.

China’s stainless steel prices have shown resilience, with futures rising 1.93% last week and spot prices following suit. The recent US-China tariff reduction agreement has supported market sentiment and encouraged traders to replenish stocks. While actual demand remains modest and buyers cautious, the price trend is currently upward, underpinned by improved trading activity and positive policy developments, despite expectations of future volatility as supply pressures build.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices remained largely steady w-o-w, inching down by INR 7,000/tonne (t) ($82/t) compared to the previous assessment on 14 May. As per BigMint’s assessment on 21 May, ferro molybdenum prices in India were at INR 2,497,000/t ($29,191/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,300/t ($1,173/t) exw-Jajpur, largely stable w-o-w.

Vedanta-Ferro Alloys Corporation (FACOR) will conduct an auction for high-carbon ferro chrome (0-150 mm) on 21 May’25. The minimum allowed bid quantity for all lots is 25-300 t. At the previous auction on 28 Apr, the larger lot of 10-150 mm fetched an H1 price of INR 99,500/t exw.

Ferro silicon: Indian ferro silicon (70%) prices remained stable as compared to the previous assessment on 12 May.

As per BigMint’s assessment on 19 May, ferro silicon prices in India were at INR 94,700/t ($1,115/t) exw-Guwahati.

Ferrous scrap: India’s imported ferrous scrap market remained largely quiet last week, with EU-origin shredded scrap edging up by $5-6/t to $367-368/t CFR Nhava Sheva. HMS 80:20 scrap prices held steady at $349-350/t CFR amid thin trading volumes.

The market continued to face pressure from sluggish steel demand, availability of lower-priced sponge iron, and a widening gap between bids and offers. With the monsoon season approaching and steelmakers facing margin pressure, buyer sentiment stayed weak and fresh bookings remained limited.

Outlook

In the short term, stainless steel prices are likely to stay range-bound, with market activity projected to remain moderate.

Leave a Reply