- SA thermal coal falls on lower sponge price

- Met coke tags drop further on panic sales

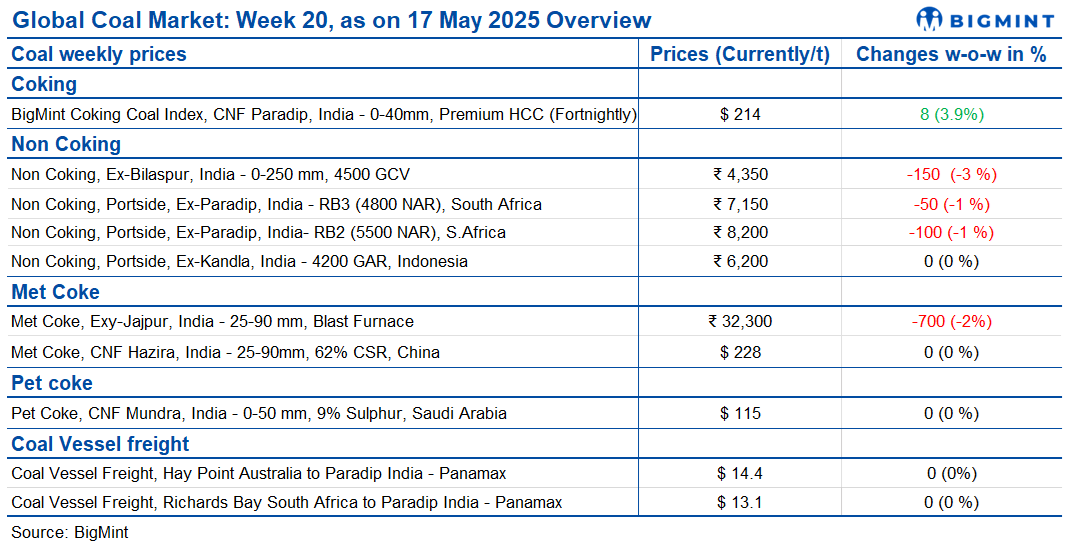

Sentiment across India’s coal and allied fuel markets remained largely weak. Sluggish demand and oversupply drove price corrections in South African, Indonesian, and domestic segments. Port congestion and adequate plant stockpiles limited fresh buying. Metallurgical coal showed brief strength on tight supply, but downstream demand stayed weak, capping gains. Met coke, pet coke, and sponge iron markets all saw price drops amid panic selling and cautious procurement. Freight rates held steady despite increased vessel availability, reflecting limited cargo movement. Overall, bearish sentiment persisted across the value chain.

SA thermal coal prices fall on high port stocks, falling sponge prices

South African thermal coal prices at Indian ports dropped due to weak demand and rising inventories. RB2 fell by INR 50/t to INR 8,250/t at Gangavaram, while RB3 declined to INR 7,150/t. Weekly coal stocks at Indian ports increased by over 5% to 15 mnt. Sponge iron prices also fell, with C-DRI down INR 300/t to INR 25,300/t. Overall, market sentiment remained soft with limited buying interest.

Indonesian thermal coal prices fall amid weak demand

Last week, Indonesian thermal coal prices at Indian ports declined due to oversupply and low demand. The temporary closure of Magdalla Port caused cargo congestion at nearby ports like Navlakhi, adding to the selling pressure. Prices of 5000 GAR remained steady at INR 7,800/t at Kandla, while 4200 GAR stayed at INR 6,200/t and 6,100/t at Kandla and Vizag respectively. The 3400 GAR grade dropped by INR 50/t to INR 4,550/t at Navlakhi.

Domestic coal prices ease amid ample supply, weak demand

Domestic coal prices softened further this week amid ample availability and subdued buying interest. The 4500 GCV grade was assessed at INR 4,350/t exw-Bilaspur, down INR 150/t w-o-w. The 5000 GCV grade fell by INR 150/t to INR 4,800/t. Buyers maintained adequate stocks, limiting fresh procurement. Ongoing auctions continued to support supply levels, keeping the market well supplied. Despite steady supply, muted demand kept prices under pressure.

Met coke prices declined further in eastern India on panic sales

Met coke prices in eastern India dropped for a third straight week due to weak demand and oversupply. BF-grade coke (25-90 mm) was assessed at INR 32,300/t ex-Jajpur, down INR 700/t w-o-w. In contrast, prices in Gandhidham stayed stable at INR 31,000/t exw. Panic selling by producers and falling pig iron auction prices also weighed on the market. SAIL sold pig iron at INR 32,800/t on 13 May, INR 700/t lower than in the previous week. NMDC booked only 4,500 t of pig iron at INR 32,500/t, indicating subdued buying interest.

BigMint coking coal index, CFR India up $8/t amid tight supply

BigMint’s PHCC index rose to $214/t CNF Paradip on 15 May, up $8/t since end-April, driven by tight Australian supply. A 25,000-t Goonyella cargo was booked at $214-215/t CFR for June. However, most buyers resisted high offers, expecting prices to fall due to weak demand. Some shifted to Canadian cargoes, while Goonyella-specific buyers held off. India’s coking coal imports rose 6% m-o-m in April to 5 mnt, led by Australia and Mozambique. Meanwhile, China’s first coke price cut in a month signalled softening demand and cost pressure in the steelmaking chain.

Refiners lower pet coke prices in May on weak demand

Indian refiners reduced pet coke prices for May 2025 due to weak demand and high availability. Reliance Industries did not declare prices for the second month, as all output was used for internal gasification. Nayara reduced prices by INR 1,070/t to INR 13,860/t. MRPL cut road prices to INR 10,430/t and rail/barge rates to INR 10,130/t. CPCL revised prices to INR 13,940/t, reflecting a smaller adjustment. Export tags at Panipat, Paradip, and Haldia stayed above domestic rake-based rates.

IOC announces fresh pet coke price cuts in May

Indian Oil Corporation (IOC) announced a second pet coke price cut for May, effective 10 May 2025, after its earlier INR 1,000/t reduction on 4 May. At Koyali, road supply rates fell to INR 10,880/t and by rakes to INR 10,680/t, down INR 1,080/t each. Panipat prices dropped by INR 1,090/t to INR 11,810/t. Paradip road rates declined to INR 11,100/t and by rakes to INR 9,900/t. Haldia’s prices were revised to INR 10,270/t (road) and INR 10,070/t (rake). Export rates were also lowered, with Paradip at INR 11,400/t and Haldia at INR 11,270/t.

India coal freights flat on weak demand, limited vessel movement

Coal freights to India remained mostly unchanged w-o-w due to muted vessel demand and slow chartering. Rates from Hay Point to Paradip held steady at $14.4/t, while Richards Bay to Paradip stood at $13.1/t. Indonesia-India (East Kalimantan to Paradip) freights stayed at $13.5/t despite soft market sentiment. Higher vessel availability was offset by a few prompt laycan inquiries, helping prevent sharp rate drops. Inventories at Indian ports rose 5.2% w-o-w to 14.95 mnt, reflecting subdued thermal coal demand. Baltic indices showed mixed trends: BDI fell 122 points w-o-w to 1,299, BPI dropped to 1,353, while BSI edged up to 969. Supramax time-charter rates in the Pacific remained firm, offering broader market stability.

Leave a Reply