- Key suppliers see shipment declines

- Weak demand, LC issues impact imports

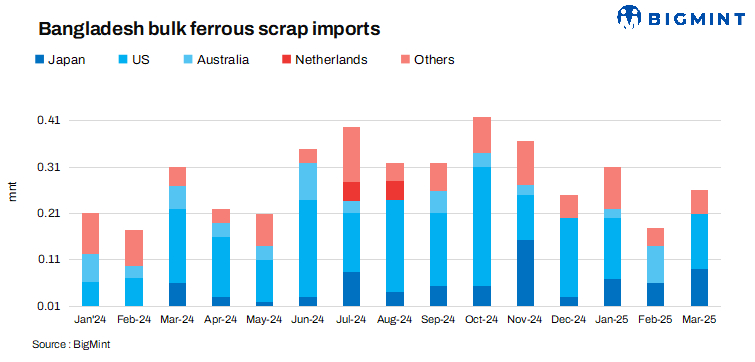

Bangladesh’s bulk ferrous scrap imports in Q1CY’25 dropped 35% q-o-q to 0.67 million tonnes (mnt), from 1.03 t in Q4CY’24.

On a y-o-y basis, imports decreased by 3% compared to 0.69 mnt seen in Q1CY’24.

In March 2025, the United States was the leading ferrous scrap exporter to Bangladesh with 125,418 t, followed by Japan with 92,295 t, New Zealand with 27,297 t, and Singapore with 17,549 t.

The drop in Bangladesh’s bulk ferrous scrap imports in Q1CY’25 was driven by weak demand from key suppliers, including the United States, Japan, Australia, Singapore, and New Zealand.

Country-wise exports

In Q1CY’25, the United States was the leading exporter to Bangladesh with 253,086 t, followed by Japan with 218,855 t, Australia with 94,151 t, New Zealand with 27,297 t, and others with 81,234 t.

United States: Exports to Bangladesh from the United States in Q1CY’25 fell a significant 52% from 531,291 t in Q1CY24, and saw a 10% decline from 281,337 t in Q4CY’24.

Japan: Exports to Bangladesh from Japan in Q1CY’25 fell by 8% from 236,952 t in Q1CY’24, but surged nearly three-fold compared to 65,397 t in Q4CY’24.

Australia: Exports to Bangladesh from Australia in Q1CY’25 rose significantly by 84% from 51,242 t in Q1CY’24, but declined by 31% from 136,039 t in Q4CY’24.

New Zealand: Exports to Bangladesh from New Zealand in Q1CY’25 dropped sharply by 64% from 76,845 t in Q1CY’24, and were down 61% from 69,167 t in Q4CY’24.

Factors contributing to scrap imports drop

Weak steel demand: Scrap imports into Bangladesh dropped in Q1CY’25 due to weak steel demand, delays in opening Letters of Credit (LCs), and low foreign exchange reserves, which restricted importers’ ability to secure funding. Additionally, mills limited bookings ahead of Ramadan and Eid, operating below capacity to manage cash flows, further affecting import volumes.

Global uncertainties: Global uncertainties kept scrap buying cautious, while some mills accepted tight or negative margins to sustain operations.

Currency depreciation: The depreciation of Bangladesh’s currency (BDT) to 121 per USD in Q1CY25, compared to 119 per USD in Q4CY24, likely made imports more expensive, contributing to the decrease in ferrous scrap imports.

Higher freight rates: Despite a drop in HMS 80:20 bulk scrap offers from the UK/Europe in Q1CY’25 to $367/t from $376/t in the previous quarter, import volumes dropped amid higher freight rates post-Red Sea crisis.

Additionally, buyers preferred to book more from nearby origins such as Singapore, Australia, Japan, and Hong Kong. The market remained subdued despite a slight recovery in finished steel demand post-holiday.

Outlook

Bangladesh’s bulk ferrous scrap imports may see a slight recovery as mills gradually resume bookings, but the pace of improvement will hinge on liquidity conditions, LC availability, and rebar demand. While some improvement in finished steel demand is expected, overall trade activity will remain sensitive to currency stability and supplier interest, particularly from key exporters like Australia and Japan.

Leave a Reply