- Japanese H2 scrap prices continue to slide

- POSCO announces cuts in scrap buy prices

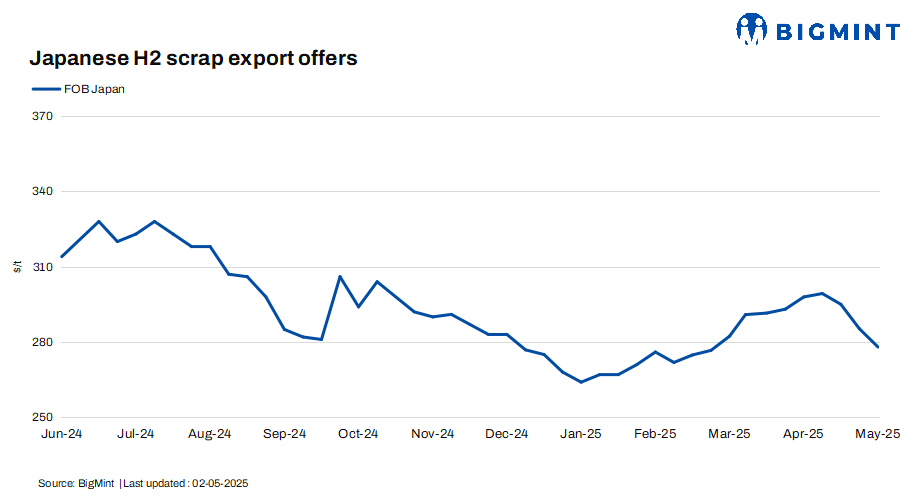

The Japanese H2 scrap export market remains weak due to sluggish domestic movement, limited operations during national holidays, and reduced export contract activity. The regional price gap where West Japan scrap prices stayed above those in East Japan since February was finally corrected in April.

The influence of the Golden Week (GW) holiday on Japan’s steel scrap market has gradually waned in recent years. Previously, continued operations by electric arc furnace (EAF) steelmakers during the holidays helped support prices. However, with widespread adoption of work-style reforms, many mills now scale back or suspend activity during this period, leading to limited market impact.

Japanese suppliers have reduced scrap offers amid falling deep-sea prices and lower domestic values. Scrapyards have also adjusted prices to stay competitive.

Despite a softer US dollar, the Vietnamese dong continues to depreciate due to the country’s export-driven focus, making it more difficult for buyers to match higher Japanese scrap prices.

BigMint’s weekly assessment stood at JPY 40,400/t ($278/t) FOB Tokyo Bay, down JPY 500/t ($3/t) from JPY 40,900/t ($282/t) the previous week.

As per latest data from the Japan Iron and Steel Association, the average price of H2-grade scrap across three major regions stood at JPY 38,300/t ($267/t) in the fourth week of April, down sharply by JPY 800/t ($6/t) from the previous week. Regionally, Kanto fell JPY 500/t ($4/t) w-o-w to JPY 43,000/t ($299/t), Kansai dropped JPY 500/t ($4/t) to JPY 38,300/t ($267/t), while Chubu saw the steepest fall of JPY 1,500/t ($10/t) to JPY 36,300/t ($251/t).

Other market updates

Vietnam: Vietnam’s imported scrap market saw further weakness this week amid soft global cues and weak finished steel demand. Japanese H2 scrap offers declined to $325/t CFR Vietnam, down from last week’s $335 – 345/t range, while bids slipped to $315 – 320/t.

A leading Vietnamese steelmaker reportedly secured a 5,000-t shredded cargo at $345 – 346/t CFR Vietnam, while other bids hovered around $340/t or lower.

Japanese scrap faced additional pressure from currency movements. Despite a weakening US dollar, the depreciation of the Vietnamese dong made Japanese offers relatively expensive.

Domestically, scrap prices remained stable, though some mills scaled back purchases due to weak demand and softening billet prices. With Bangladeshi buyers pulling back, Vietnamese mills booked premium scrap at reduced rates. However, continued bearishness in billet pricing and currency pressure are expected to keep the tone soft.

South Korea: South Korea’s ferrous scrap market saw a sharp pickup in activity during the fourth week of April as POSCO resumed imports after a one-month halt. The country’s major ports received around 41,800 t of incoming scrap, triggering concerns over rising supply amid subdued domestic demand.

Pohang led with a 15,000 t intake, while other ports Gunsan, Incheon, and Gwangyang received 10,000 t of SHRD, H2, and Shindachi grades, along with 5,500 t of HMS. Jinhae recorded a smaller shipment of around 1,300 t.

Steel scrap inventory at major South Korean mills remained flat at approximately 929,000 t in the fifth week of April, ending the previous trend of stock buildup. The central region saw a modest increase to 518,000 t, while southern stocks held steady at 411,000 t.

Additionally, POSCO announced a KRW 5/kg ($4/t) cut in scrap purchase prices at its Gwangyang and Pohang plants, effective May 2. This reduction, coupled with rising imports, is expected to weigh on market sentiment.

Reduced scrap output during the holiday season is restricting steelmakers’ ability to replenish inventories, which may alter the market’s course in early May.

Taiwan: Taiwan’s imported scrap market remained quiet this week due to the Dragon Boat Festival and Labour Day holidays. Limited activity kept market sentiment subdued.

Recent offers showed a downward trend: US-origin HMS 80:20 fell by $5/t w-o-w to $303/t CFR Taiwan, while Japanese H2 dropped more sharply by $10/t to $315/t CFR.

Outlook

Japanese H2 scrap exports are expected to stay under pressure due to sluggish domestic movement, reduced holiday operations, and weakening global demand. The depreciation of the Vietnamese dong could further limit buyer interest in higher-priced Japanese scrap.

In South Korea, the resumption of POSCO’s imports may increase supply, but weak domestic demand could prevent significant price increases. Vietnam’s market will continue to face challenges from soft steel demand and currency fluctuations, while Taiwan’s market remains subdued due to holidays, keeping overall sentiment cautious.

Leave a Reply