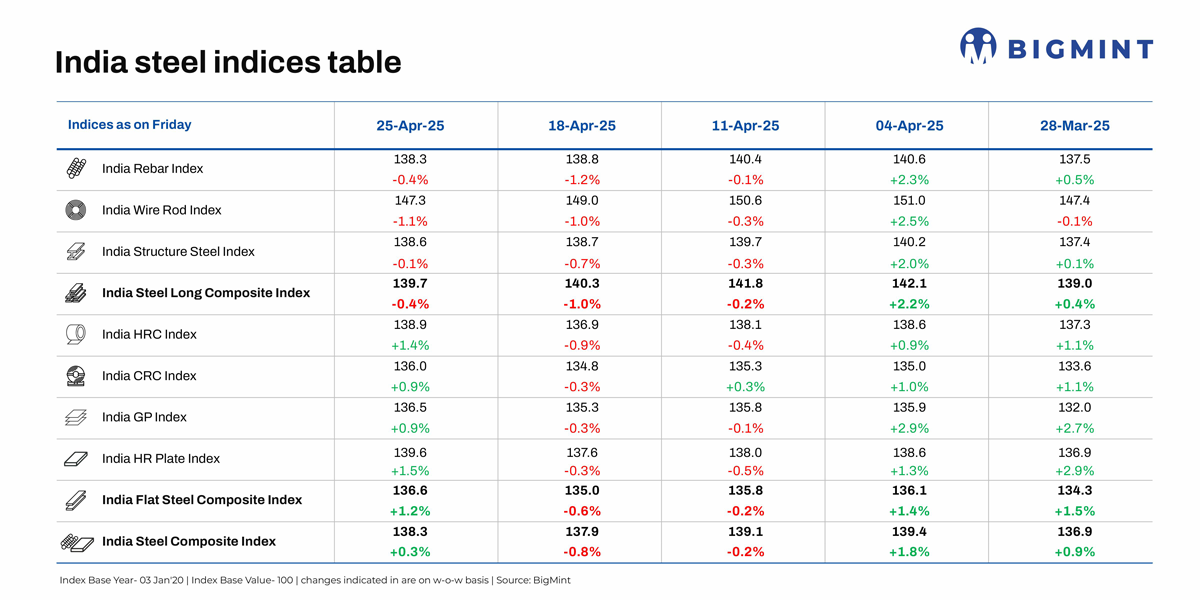

- Long steel composite index drops 0.4% w-o-w

- HRC trade prices edge up but buyers resist hike

- Supply issues, global headwinds to affect prices?

Morning Brief: BigMint’s India steel composite index, which offers a bird’s-eye view of price movements in the domestic steel industry, inched up by 0.3% w-o-w to 138.3 points on 26 April 2025 after declining by around 1% over the last couple of weeks.

The flat steel composite index gained 1.2% w-o-w, with HRC and plate prices trending upward. However, the long steel index edged down by 0.4% w-o-w.

Flats

HRC trade prices edge up: Trade-level prices of hot-rolled coils (HRC) rose w-o-w across markets, with Mumbai seeing an increase of INR 1,200/t w-o-w ($14/t) (IS2062, Gr E250, 2.5-8 mm/CTL) to INR 52,500/t ($615/t) on 25 April. Cold-rolled coil (CRC) prices also increased across locations, with an INR 1,000/t ($12/t) w-o-w hike to INR 59,500/t ($697/t) in Mumbai.

Overall, market sentiment remained cautious due to moderate demand and buyer resistance to higher prices.

Additionally, the high threshold value of $675/t CIF for HRC, sheets and plates under the safeguard duty regime allows some scope for local producers to raise prices. Indian prices may also be supported by global offers, which are slightly on the upper side at the moment. For example, Chinese HRC offers stood at $455/t FOB Rizhao, stable w-o-w. Japan’s offers stood at $465/t, stable since early-April.

Trade-level prices of hot-rolled (HR) plates (IS2062, grade E250 Br, 20-40 mm) rose by up to INR 1,800/t w-o-w to INR 54,500-57,000/t ex-Mumbai on 24 April. Prices of hot strip mill (HSM) plates (IS2062, grade E250 Br, 5-10 mm) increased by up to INR 1,000/t w-o-w to INR 52,000-53,000/t ex-Mumbai. Prices increased, following the implementation of the safeguard duty, mirroring the uptrend across the entire flat steel segment.

Steel imports drop, HRC export offers rise: India’s bulk imports of HRCs and plates touched 210,591 t as of 21 April, based on vessel line-up data with BigMint. Another 65,488 t are expected to arrive by month end. So, there has been a significant drop in imports of flat steel compared with over 408,000 t in March.

On the other hand, Indian HRC export offers to the EU rose by $10-15/t w-o-w to $645-650/t CFR Antwerp as compared to $630-635/t CFR a week ago. Despite this price increase, trading activity within the EU remained subdued due to the Easter holidays.

Longs

Trade-level BF-origin rebar prices drop: Trade-level blast furnace (BF) rebar prices dropped w-o-w across key markets amid sluggish demand. Buyers preferred to wait and watch, expecting a further decline in prices in the near term. But tight supply still prevailed in some regions, and mills struggled to fulfil orders amid limited inventories at their yards.

Prices edged down by INR 200/t ($2/t) w-o-w to INR 56,900/t ($666/t) exy in Mumbai on 25 April. Prices are exclusive of GST at 18%.

IF rebar prices drop w-o-w: Induction furnace (IF) rebar prices declined w-o-w across most markets due to subdued buying. Prices rose earlier in the week, driven by positive sentiment following the imposition of the safeguard duty, prompting buyers to secure significant volumes. However, as the week progressed, prices softened due to a lack of sustained demand at elevated tags. There was no inventory pressure on mills, with average holding periods of 7-8 days.

Outlook

It is evident that the domestic steel market has been unable to absorb the price hikes effected following the safeguard duty recommendation. This is most apparent in the decline of long product prices which are outside the ambit of the duty.

However, in the flats segment, too, prices are likely to remain firm in May. While demand is moderate at the moment, it is expected to pick up gradually. Prices may also be supported by tight supply, as certain leading steelmakers are expected to undertake production cuts for 30-35 days for maintenance reasons. However, once support from this quarter dissipates, prices may trend down in June and July.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply