- Crude steel, exports uptrend, iron ore imports dip

- Manufacturing, infra spends see m-o-m uptick

- Realty still floundering despite policy support

Morning Brief: China’s macro indicators in the first quarter (January-March, 2025) was a mixed bag although the m-o-m performance was slightly improved in March.

Crude steel production showed a slight increase in Q1. Manufacturing and infra investments looked up slightly m-o-m. Real estate continued to flounder – the rate of decline showed a slight easing towards January but failed to retain this initial positivity. Yet, the declining momentum is still lesser than the over -10% seen over May-December 2024. Steel exports retained their upward momentum, albeit at a marginally slower pace, but still offered the much-needed solace to China’s steel mills.

Crude steel output rises on better factory, infra performance: China’s crude steel production upped a minor 0.60% y-o-y to 259 million tonnes (mnt), which was actually a 2.10% increase over January-February, 2025, when it had declined by 1.50%. In March 2025, volumes rose nearly 5% to 93 mnt from 88 mnt in March 2024. Mills were encouraged to keep the production momentum going because of better performance from the manufacturing and infrastructure segments. Secondly, the market scenario reversed from one of panic caused by the US tariff storm to expectations of support from policies. Thirdly, with exports still continuing to show an uptrend, production mirrored an upside.

In keeping with the crude steel trend, pig iron production rose 0.80% to 216 mnt in these three months under review, reversing the decline of 0.50% seen in January-February, 2025.

Iron ore imports dip amid adequate stockpiles: Iron ore imports, however, continued to reflect a contrarian trend we are seeing for months now. Volumes fell almost 8% to 285 mnt y-o-y. One reason was the decline in crude steel by 2% y-o-y in January-February 2025 and by 1.70% for the full year 2024 to 1,005 mnt.

Secondly, port inventories showed a rising trend in 2024 because of low domestic steel demand, and which is having a spin-off effect in 2025. Rising inventories have been putting pressure on port storage infrastructure, leading to rising warehousing costs. There is also possibly a mismatch between crude steel production needs and import volumes. The Lunar holidays saw a slowdown in demand and offtake. Lastly, March imports fell to their lowest in 20 months because of supply disruptions in Australia caused by Cyclone Zelia.

Steel exports continue northward march: China’s steel exports continued to head north, rising over 6% to around 27 mnt y-o-y in the first three months of 2025. Some factors continue to support overseas sales. 1) Domestic demand has improved but there is still a long way to go. Manufacturing and infra are performing somewhat better but real estate, the main steel guzzler, is still lagging behind. 2) Predatory pricing is giving Chinese exporters an edge. Chinese average benchmark HRC offers in Q1 were still the lowest on FOB basis, amongst the key exporting countries at $470/t compared to Japan’s $473/t, India’s $502/t and Russia’s $482/t.

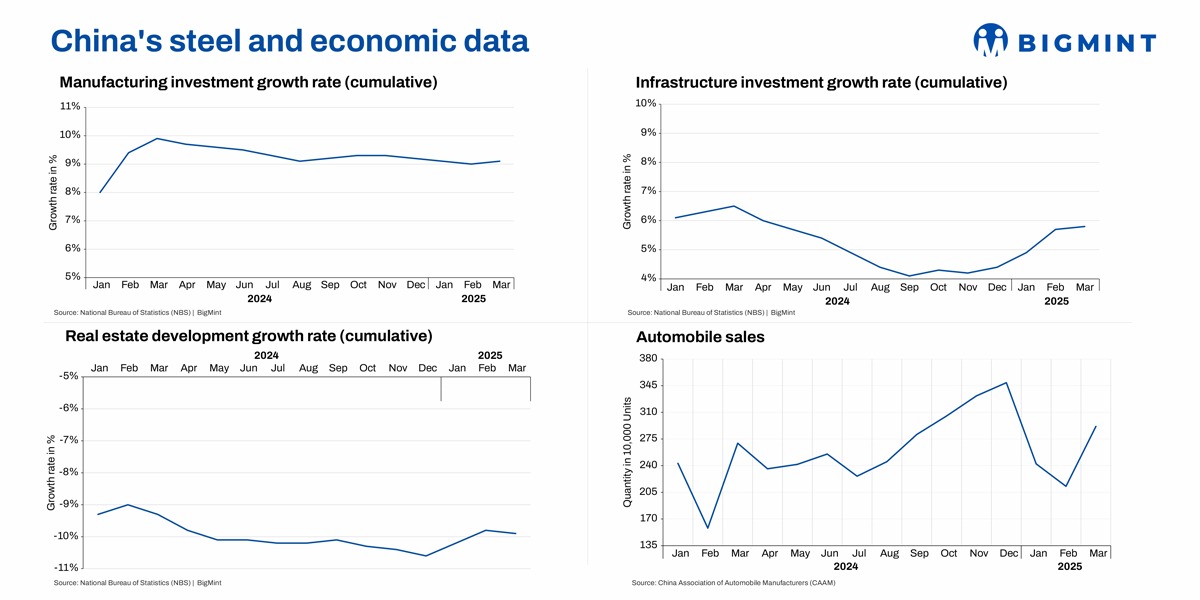

Meanwhile, China’s steel imports fell 11% to 1.55 mnt in the first three months amid slow domestic demand. Manufacturing investment growth range-bound: Manufacturing investment grew marginally to 9.1% in March 2025 against 9% in February. Y-o-y, the average growth in Q1CY’25 was at 9.03 against 9.1% in the same three months in 2024, indicating that the overall trend is range-bound and has remained so for around a year. Automobile production in January-March, 2025 rose a healthy 14.50% y-o-y to 7.56 million units. Plus, the PMI rose to 50.2% in February from 49.1 in January this year and further to 50.5% in March. A PMI of over 50% reflects expansion in factory output. Possibly, expectations of policy support kept manufacturing supported.

Manufacturing investment growth range-bound: Manufacturing investment grew marginally to 9.1% in March 2025 against 9% in February. Y-o-y, the average growth in Q1CY’25 was at 9.03 against 9.1% in the same three months in 2024, indicating that the overall trend is range-bound and has remained so for around a year. Automobile production in January-March, 2025 rose a healthy 14.50% y-o-y to 7.56 million units. Plus, the PMI rose to 50.2% in February from 49.1 in January this year and further to 50.5% in March. A PMI of over 50% reflects expansion in factory output. Possibly, expectations of policy support kept manufacturing supported.

Infra sentiments improve marginally m-o-m: Infrastructure investment growth showed a marginal m-o-m uptick of 5.8% in March against 5.7% in February. However, on a y-o-y basis, the growth was slower at 5.63% over January-March, 2025 compared to 6.3% in the same three months last calendar. But, infrastructure spending is reported to be improving, with the PMI for non-manufacturing activity, which includes construction, touching a three-month high. Overall, excluding the real estate sector, fixed-asset investment experienced a strong 8.3% increase in the first three months of the year. These developments point to some sense of positivity in the market.

Realty continues to lose ground: The real estate investment growth decline deepened marginally to -9.9% in March 2025 against -9.8% in February and -9.7% in January. Over January-March, the average decline was -9.8% against a slower -9.2% in the same three months in 2024. Property sales by floor area dropped 5.1% y-o-y, while new construction starts plunged 29.6%, highlighting the sector’s prolonged downturn, which started in 2021 with the collapse of realty behemoth Evergrande and has not made a recovery till date despite government support. The cement sector, in tandem, has been performing poorly — its production dipped 1.40% to 331 mnt in January-March, 2025.

Coal imports dip amid trade tensions, currency fluctuations: Coal production rose but imports dropped in January-March, 2025. Production upped 8% to 1,200 mnt while imports dipped almost 1% amid escalating trade uncertainties. Rising uncertainties from US President Trump’s trade war and the continued fluctuation in exchange rates impacted China’s coal imports. In fact, China’s cumulative imports of coal in Q1 declined for the first time since 2023. This was made up by increased domestic production.

Outlook

China’s economy posted stronger-than-expected growth in Q1 2025, with the GDP expanding 5.4% y-o-y, outperforming forecasts, thanks to a surge in exports.

But the IMF has slashed China’s GDP growth forecast for full year 2025 to 4%, down from its January figure of 4.6%, citing trade tensions and “high policy uncertainty”.

The US tariffs onslaught may keep China on its toes and push it to divert steel to other geographies, which can further pressure margins.

Leave a Reply