- Rebar sales improve amid sharp price drop

- Weak demand continues to pressures suppliers

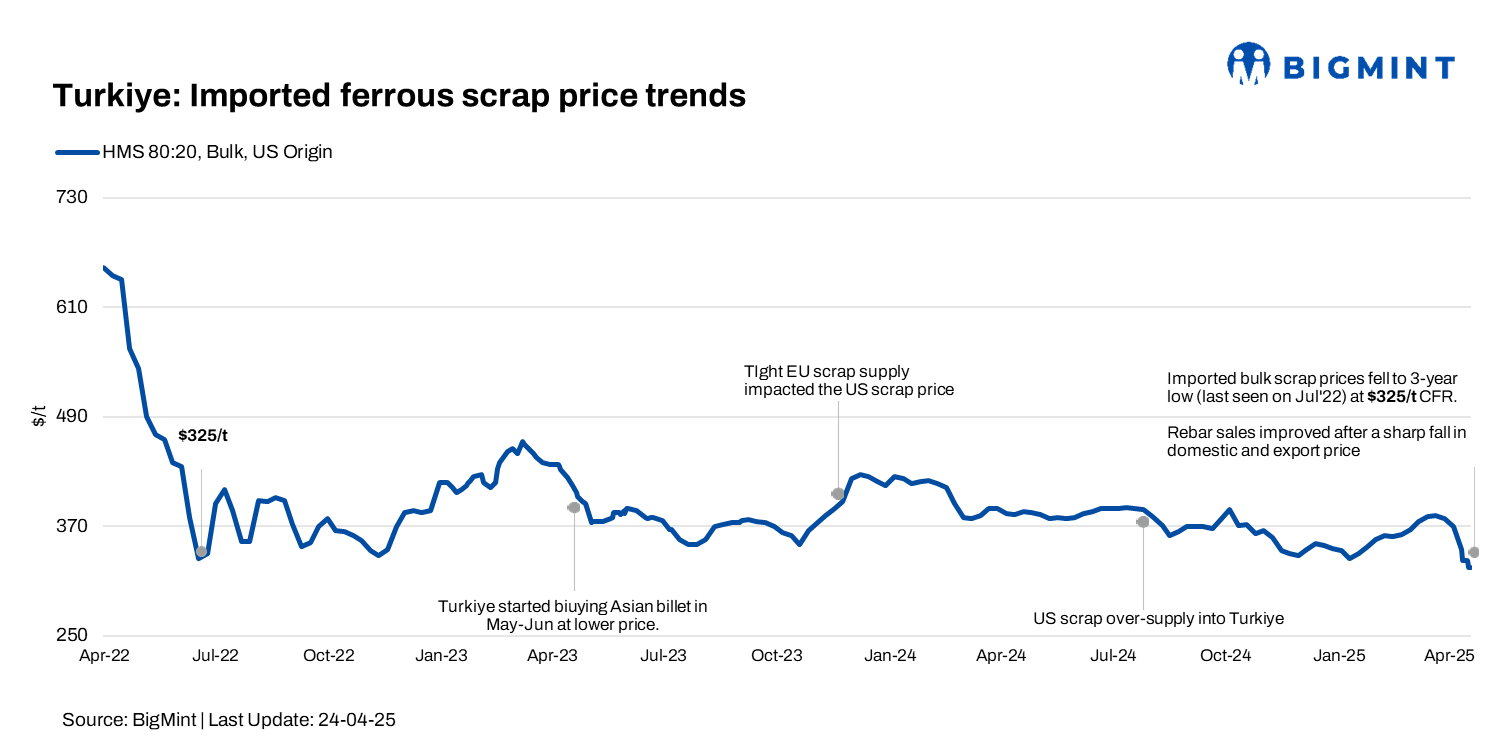

Turkish deep-sea imported scrap prices declined by $20/tonne (t) w-o-w, hitting their lowest level since June-July, 2022, marking a three-year low.

It is also noteworthy that prices have dropped by $50-60/t since the beginning of the month, when they stood at around $380/t. Mills continued restocking at reduced levels amid ongoing oversupply and weak finished steel sentiment.

The decline was further reinforced by sharp drops in domestic rebar prices, prompting Turkish buyers to maintain pressure on scrap import values.

BigMint’s price assessments

- US-origin HMS 80:20 bulk scrap stood at $325/t CFR Turkiye, down $20/t w-o-w.

- Bulk HMS 80:20 from the US East Coast was at $304/t FOB, down $20/t w-o-w.

The Turkish scrap-to-rebar spread stood at $215-220/t, as export offers for the latter dropped w-o-w to $535-540/t FOB.

Market comments

A Turkish mill representative noted that rebar FOB levels have dropped to around $540-545/t, with some domestic transactions dipping below $530/t. Current offers to Europe stand at $560-580/t CFR, implying FOB levels of $540-550/t. Interestingly, this price drop has led to an uptick in sales in both export and domestic markets this week. Meanwhile, Chinese billet is being offered at $455/t CFR Turkiye, adding more competitive pressure to the market.

Indicative offers for US and Baltic-origin HMS 80:20 were largely heard at $325/t CFR, but Turkish buyers were bidding lower. A $315/t CFR bid for Baltic material was reported but ultimately rejected by sellers.

A European trader noted, “Scrap sellers waited too long, causing inventories to build up at the yards. With buying interest now limited, sellers are starting to panic.”

A mill-side participant stated, “There is an oversupply of cargoes, and Turkish buyers are driving prices down.” However, another mill source noted cautious optimism, adding that that prices could rebound soon amid improving domestic rebar sales.”

A market participant commented, “Mills are cutting back production, and with reduced capacity utilisation driven by sluggish finished steel sales, scrap demand is also falling.”

A market participant noted, “There is significantly more low-grade scrap available compared to the premium variety. When demand softens, mills tend to prioritise premium-grade material. Recent restocking has primarily targeted US and Baltic cargoes, making it more challenging for European sellers, since much of the demand for May shipments has already been met.

Recent deals

- US-origin HMS 80:20 at $330/t along with shredded/bonus at $350/t were sold to a Mediterranean mill.

- US-sourced HMS 90:10, priced at $327/t was sold to a West Marmara mill.

- US-origin HMS 80:20 ($325/t) and shredded/bonus ($345/t) went to a Mediterranean mill.

- US-origin HMS 80:20, offered at $331.5/t was sold to a West Marmara mill.

- EU-origin HMS 80:20 ($330/t) went to a Mediterranean mill.

- EU-origin HMS 75:25, offered at $333/t was sold to an Aegean mill.

- Baltic-sourced HMS 80:20 ($320/t) went to two Mediterranean mills.

- UK-origin HMS 80:20, at $312/t was sold to a Mediterranean mill.

- US-origin HMS 90:10, priced at $328.50/t and shredded at $345.50/t went to an Aegean mill.

- EU-origin HMS 80:20 ($320/t) went to an Aegean mill.

Domestic market scenario

In the domestic market, major Turkish mills continued lowering scrap prices amid weak finished steel demand and falling import values:

- Erdemir cut prices by TRY 200/t to TRY 12,850/t ($335) for standard grade.

- Kardemir lowered busheling scrap to TRY 13,400/t and extra grade to TRY 13,165/t.

- Kroman began purchases at TRY 12,900/t (busheling scrap) and TRY 12,350/t (extra).

- Colakoglu held prices steady at TRY 13,335/t (busheling scrap) and TRY 12,830/t (extra).

Turkish rebar sales saw improvement, with domestic deals reported at around $530/t exw. However, Turkish rebar export prices are lower at $535-540/t FOB, reflecting a decline of $10-15/t.

Outlook

Despite a few signs of improving demand for finished steel, the scrap market remains under pressure from oversupply, weak buying interest, and cautious sentiments heading into May.

Leave a Reply