The domestic steel market saw a downward trend in prices during week 15 ( 7 Apr- 12 Apr, 2025). Semi-finished steel prices decreased by INR 200-700/tonne (t).

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index remained stable w-o-w at INR 10,250/t ($120/t) DAP Raipur on 11 April. Around 64,000 t of pellet (Fe62.5/63%) deals concluded in Raipur by local and Odisha-based suppliers.

- NMDC auctioned around 68,200 t of iron ore from its Bacheli mines, Chhattisgarh on 11 April. The entire 25,800 t of DRCLO (10-40 mm, Fe 67%) booked at a premium of INR 630/t over the base price of INR 7130/t, while 8,000 t Baila-sized lumps (10-20 mm, Fe 65.5%) were booked at premium of INR 660/t on the base price of INR 6,500/t. Prices were set on FOR, ex-stockpile/mines basis, including royalty, DMF and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index decreased by $3/t w-o-w to $59/t FOB east coast, India, on 10 April. Indian exporters and miners concluded export deals for around 350,000 t of iron ore fines (Fe54-57%) from the east coast last week. BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) dropped by $8.5/t w-o-w to $88.5/t on 11 April.

Coal

- South African thermal coal prices in India remained stable w-o-w, with RB2 at INR 8,450/t ex-Gangavaram and INR 8,500-8,600/t at Paradip. RB3 coal also held steady at INR 7,200-7,350/t across key port locations.

- Domestic coal prices in Bilaspur stayed unchanged this week, with 4500 GCV and 5000 GCV grades at INR 4,500/t and INR 4,950/t respectively. Traders resisted further reductions, citing bottomed-out price levels despite limited buying activity in the market.

- Domestic met coke prices held steady at INR 34,300/t exw-Jajpur and INR 32,300/t exw-Gandhidham. Coking coal cost pressures, weak Chinese demand, and cautious buyer sentiment kept the market stable despite minor deals for imported Colombian coke.

- Pet coke prices remained mostly unchanged in April. RIL skipped offers due to internal demand, while Nayara and MRPL maintained previous rates. Yearly prices rose 12-17%, with Saudi-origin cargoes staying costlier amid steady flows to China.

Ferrous scrap

- India’s imported scrap market stayed quiet in early April with minimal trading activity due to a persistent bid-offer gap and weak buyer interest. Shredded offers held firm at $390-395/t CFR, while buyers quoted below $385/t. HMS 80:20 saw a similar disconnect, with bids trailing offers by $5-7/t. Sellers remained reluctant to adjust, citing stronger Euro, tight supply, and steady demand in local markets.

- Despite strong domestic steel sales, mills preferred local scrap and sponge iron, which remained more cost-effective. Seasonal demand supported finished steel prices, but this did not translate into stronger scrap buying, as mills managed operations with existing inventories. Amid ongoing uncertainty over safeguard duties sellers held firm on offers, backed by local demand.

- Around 5,000-6,000 t of imported HMS 80:20 scrap arrived in India this week, priced between $351-370/t from West Africa, Caribbean, Brazil, Ireland, Central America, Chile, Congo and Poland and HMS 1 at $384/t from Bahrain.

Ferro alloys

- Silico manganese: Indian silico manganese prices inched down w-o-w by INR 350/t ($4/t) to INR 71,500-72,500/t ($830-842/t) in the key regions of Durgapur, Raipur and Vizag. Prices fell slightly as buyers resisted higher quotes, favouring more competitive offers.

- Ferro manganese: Indian ferro manganese (HC 70%) prices decreased w-o-w to INR 75,000/t ($877/t) exw in Durgapur, inching down by INR 680/t ($8/t). Meanwhile, prices exw-Raipur also declined by INR 640/t ($7/t) to INR 75,000/t ($877/t). Prices dropped due to need-based buying and limited inquiries.

- Ferro silicon: Indian ferro silicon prices decline by INR 900/t ($10/t) w-o-w to INR 96,100/t ($1,116/t) exw-Guwahati. However, prices were unchanged in Bhutan to INR 96,500/t ($1,116/t) exw. Prices dropped amid weak demand, cheaper imports, and market adjustments.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices inched up by INR 200/t ($2/t) w-o-w to INR 100,300/t ($1,164/t) exw-Jajpur. Prices remained mostly stable as market uncertainty and bid-offer gaps clouded short-term direction for participants.

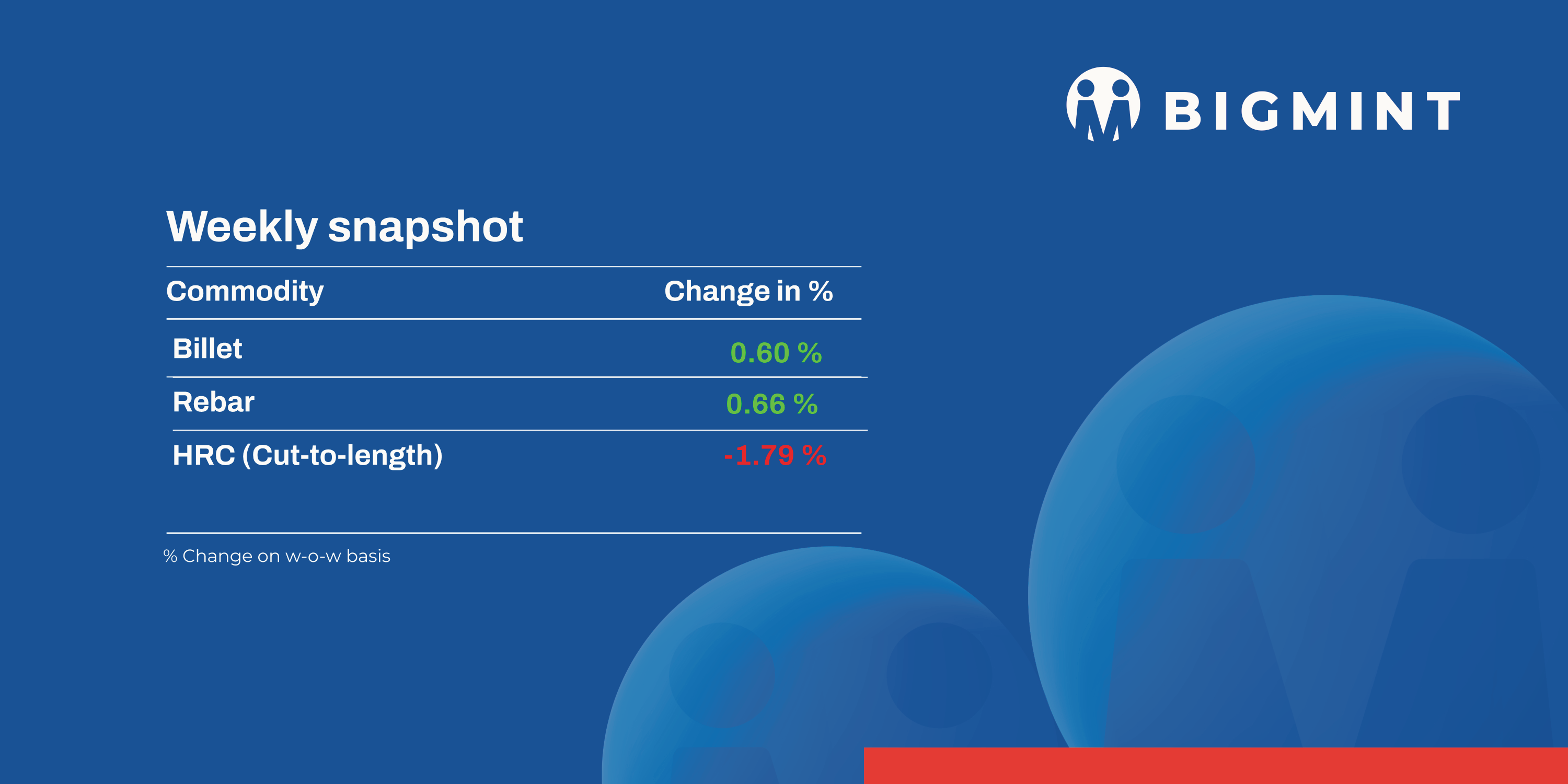

Semi-finished steel

- Indian semi-finished steel prices showed trended lower, as per BigMint assessment. Domestic billet prices in almost all key locations decreased by INR 200-700/t across regions with a major decrease of INR 700/t seen in Hindupur. Only Ahmedabad saw prices rising by INR 100/t. However, sponge iron prices showed mix trends in almost all key locations, moving down by INR 50-500/t, with a major decrease of INR 500/t seen in the Durgapur market.

- Indian DRI (Direct Reduced Iron) export offers decreased by $8 for CPT Raxaul to $362/t, while CPT Benapole offers decreased by $14/t to $363/t.

Finished long steel

IF-rebar: India’s induction furnace route finished long steel prices declined amid limited trading activity. Buying remained need-based throughout the week due to market uncertainty. Manufacturers maintained stable prices or offered trade-level discounts based on orders. Smooth dispatches of previously booked materials have reduced mill inventories to around five-eight days which vary location wise. Market participants expect prices to remain range-bound in the near term.

-

On a weekly basis, rebar steel prices fell in the range of INR 100-600/t across regions.

-

The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 45,800-46,200/t exw Raipur and INR 49,400-50,000/t exw Jalna.

-

Trade reference prices of heavy structural steel for base size 150mm channel are at INR 47,100-47,500/t exw Raipur.Trade reference prices of wire rods hovered at INR 46,300-46,800/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices increased w-o-w across major Indian markets, as some private steel mills announced a hike in list prices by up to INR 1,500/t, during the week. Post revision, list prices hovered within INR 57,000-58,500/t on landed basis. Demand in the distribution channel was need-based, impacted by lower buying interest. However, ongoing material shortages kept prices supported.

- This week rebar prices (12-32mm) in the trade segment increased by INR 200/t w-o-w to INR 57,200/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered at around INR 56,500-57,500/t FOR Mumbai. Demand from end-users remained moderate this week.

Flat Steel

-

- Trade-level hot-rolled coil (HRC) offers fell by up to INR 1,000/tonne (t) ($11/t) w-o-w to INR 51,200-53,500/t ($586-613/t) across markets. However, cold-rolled coil (CRC) prices remained stable w-o-w at INR 56,300-59,000/t ($654-689/t). Notably, limited demand and need-based buying kept prices in check.

- India’s bulk imports of HRCs and plates touched 70,430 t as of 7 April, based on vessel line-up data from BigMint. Another 86,109 t are expected this month.

- Indian hot-rolled coil (HRC, SAE 1006) export offers to the Middle East remained subdued after the Eid holidays, as buyers stayed cautious amid global market uncertainty triggered by the new US tariffs.

- Offers to the EU held steady at $630-635/t CFR Antwerp, supported by stricter safeguard measures. European domestic HRC prices rose due to limited imports and producer-driven hikes, though demand remained weak. The price gains were largely policy-driven, not demand-based.

Leave a Reply