- Indian buyers inactive despite firm offers

- Pak, Bangla buyers cautious amid weak cues

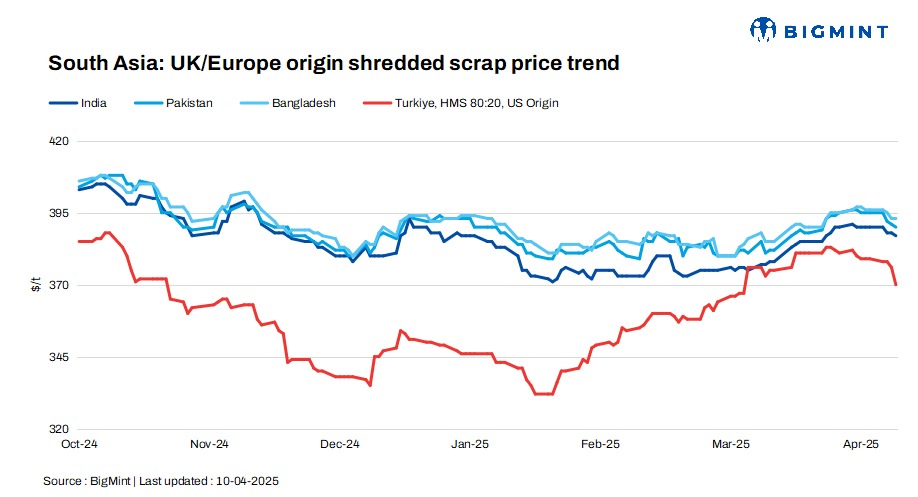

South Asia’s imported scrap market remained largely sluggish this week as buyers across the region continued to adopt a cautious stance amid weak demand signals and firm global offer levels. In India, despite steady finished steel sales, cheaper alternatives and a persistent bid-offer gap kept buyers on the sidelines.

Pakistan’s market failed to pick up post-Eid, with slow construction activity and security concerns further dampening sentiment. Bangladesh saw limited recovery, as LC issues and tight forex conditions restricted buying appetite. Meanwhile, Turkiye’s mills stayed out of the deep-sea market, citing weak rebar sales and better alternatives like billets, even as EU-origin scrap offers held firm.

UK-origin shredded offers edged down $1/t in India and Pakistan, while remaining unchanged d-o-d in Bangladesh. US-origin bulk HMS 80:20 offers to Turkiye dropped by $6/t d-o-d.

Overview

India: India’s imported scrap market remained largely inactive as buyers adopted a wait-and-watch approach amid a persistent bid-offer gap. Shredded scrap offers from the UK/EU were quoted at $390-395/t CFR Nhava Sheva, while buyers showed interest at $380-385/t. HMS 80:20 offers from the UK and Australia hovered at around $360-365/t CFR, but bids stayed lower by $5-7/t.

Despite strong domestic steel sales, cheaper sponge iron and domestic scrap, along with sufficient inventories, curbed import appetite. Sellers held firm on offers, backed by local demand and a stronger euro. Buyers, however, preferred ready cargo and awaited clearer policy signals before making fresh bookings.

Pakistan: Pakistan’s imported scrap market stayed muted post-Eid, with buyers cautious amid slow domestic demand and firm offer levels. UK/EU shredded scrap offers held at $390-395/t CFR Qasim, while UAE-origin scrap ranged from $395-400/t. Though electricity tariff cuts brought some relief to mill margins, activity remained subdued due to post-holiday inertia, security concerns, and limited construction momentum.

Domestic scrap hovered at PKR 135,000-140,000/t ($487-505/t). Mills are waiting for stronger cues from demand revival or budget policies before ramping up purchases.

Bangladesh: Bangladesh’s imported scrap market saw a quiet recovery after Eid, but activity stayed limited due to ongoing LC hurdles and selective buying. Prices for shredded and HMS dropped slightly by up to $5/t as mills held back from aggressive restocking, relying more on domestic scrap. Larger mills remained cautious, preferring to monitor the market despite a BDT 500/t hike in rebar prices driven by slightly better sales.

Offers for shredded hovered around $385-395/t CFR, while Australian HMS was quoted at $365-370/t. With HKC compliance worries and tight forex liquidity still clouding sentiment, most buyers remain conservative, eyeing gradual improvement in both demand and prices in the near term.

Turkiye: Turkish imported scrap prices fell as mills stayed out of the market due to weak rebar sales and growing interest in cheaper billet imports from the Far East. Despite softening collection costs in Benelux and ample scrap availability for May, sellers held offers firm, especially with a strong euro complicating price cuts from EU suppliers.

Mills delayed deepsea bookings, considering shortsea scrap and billet as better alternatives, while traders cited breakeven levels around $365-$370/t CFR for EU scrap. The subdued market sentiment and declining steel demand hint at possible production cuts ahead, reinforcing mills’ wait-and-watch approach.

Price assessments

India: UK-origin shredded indicatives were assessed at $387/t CFR Nhava Sheva, down by $1/t d-o-d.

Pakistan: UK-origin shredded indicatives edged down by $1/t d-o-d to $390/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives stood at $393/t CFR Chattogram, unchanged d-o-d.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $370/t CFR Turkiye, decreased by $6/t d-o-d.

Leave a Reply