- Global scrap consumption falls on sluggish steel demand

- Scrap demand rises in the EU, declines marginally in China

- Indian mills record higher scrap intake amid surging steel production

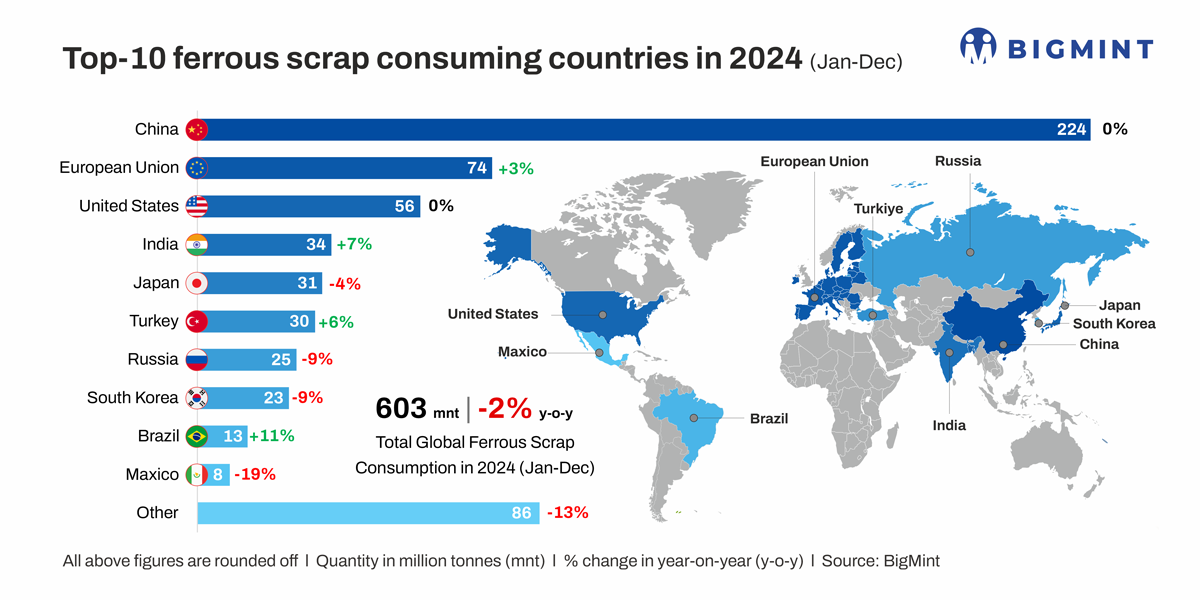

Morning Brief: Global ferrous scrap consumption inched down by 2% y-o-y in CY’24 to 603 million tonnes (mnt) compared to 616 mnt in CY’23, as per data maintained with BigMint.

The drop comes amid a 0.9% fall in global crude steel production. Subdued demand for steel, falling prices of finished products, and weak mill margins pressured steel production globally.

The drop in global consumption is attributed to lower scrap usage in Japan (-6%), South Korea (-8%), Russia (-7%), Mexico (-20%), Taiwan (-13%), and Canada (-14%). However, consumption increased in the EU (+3%), India (+6%), Turkiye (+7%), Brazil (+18%), and Vietnam (+14%), though this was not able to offset the overall decline. China recorded a marginal drop of 0.4%, while the US saw stable consumption.

Factors influencing world’s top 10 scrap consumers in CY’24

Realty sector woes curb China’s construction demand: China’s scrap usage edged down by 0.44% y-o-y in CY’24, as the property and construction sector remained in dire straits, keeping buying interest for steel subdued. Additionally, steel production declined by 1.7%, as the government focused on controlling China’s overcapacity, which has significantly affected both steel prices and mill margins.

EU scrap consumption rises on higher steel production: The European Union witnessed a 3% rise in scrap consumption, owing to a 2.6% uptick in steel production, the first growth in three years. Stability in the automotive and machinery sectors kept steel demand supported. Notably, the EU closed 2024 with a 0.8% growth in its automotive market, as per data from the European Automobile Manufacturers Association. The EU will obviously aim at increasing the share of scrap in crude steel production amid a gradual shift away from BF-BOF-based technologies and increasing carbon prices.

US steel production remains firm: Steel output in the US grew a minuscule 0.2% y-o-y, allowing the country to maintain stable scrap consumption. Automotive and manufacturing demand was overall firm in CY’24, supporting steel consumption, though fluctuating prices and sluggish construction activity posed hurdles.

Scrap consumption rises 6% in India: Scrap consumption in India improved by 6%, primarily driven by a 6.3% rise in steel production. EAF/IF mills increased their scrap usage. Additionally, Indian mills raised their usage of domestic scrap, and imported scrap volumes declined as a result. The construction and auto sectors showed robust demand for steel, while government policies such as end-of-life vehicle scrapping boosted domestic scrap generation.

Japan’s scrap consumption declines: Japan’s scrap consumption decreased by 6%, mirroring a 6% drop in crude steel production. The country’s automotive and machinery sectors suffered from weak demand, with new car sales dropping by 7.5% y-o-y. Certain key sectors, such as construction, were afflicted by labour shortages. As a result, amid flagging demand for steel, Japanese scrap suppliers turned to exports.

Turkish market upbeat on healthy export demand: Scrap consumption in Turkiye climbed up by 7% y-o-y amid a 6% increase in steel production. Turkiye recorded healthy steel export volumes in CY’24, with billet shipments increasing while construction demand in the Middle East and Europe remained solid. Fresh investments and capacity expansions in 2023 raised steel production in CY’24.

Trade sanctions compel Russia to cut steel output: As the war with Ukraine progressed, Russia continued to face sanctions and trade barriers. This limited its export opportunities and led to a 7% drop in steel production in CY’24. Additionally, domestic demand remained subdued, which pushed steelmakers more towards economical pig iron. These two factors ultimately reduced scrap consumption by 7% y-o-y.

South Korea faces weak steel demand: South Korea experienced an 8% decline in scrap consumption, tracking a 4% dip in steel production. First, the country’s scrap market was battered by weak steel demand amid high energy costs, which prompted mills to undertake maintenance shutdowns. Secondly, steel exports to Southeast Asia and China slumped, amid a supply glut in the latter. This forced Chinese mills to export material at aggressively low prices and cut off South Korea’s access to its major trading destinations. Thirdly, steelmakers preferred sourcing pig iron due to its competitive prices.

Strong government support benefits Brazil’s steel industry: A 12% uptick in steel production in CY’24 lifted scrap consumption in Brazil by 18%. The increase was driven by a supportive policy framework for Brazil’s steel industry. Strong infrastructure demand also propelled Brazil’s scrap consumption.

Mexico hit by weak auto, construction demand: Mexico’s scrap consumption plunged by 20% y-o-y in CY’24, though steel production fell a more modest 9%. Demand from the US auto and construction sectors softened, adversely impacting Mexico’s scrap usage.

Scrap consumption is expected to continue its downtrend in the first half of CY’25, with BigMint forecasting 322 mnt of usage in H1CY25, a slight 2% drop from 328 mnt in H1CY’24. However, H1CY’25 is expected to see a strong 17% recovery from the 275 mnt consumed in H2CY’24.

Scrap volumes are expected to steadily pick up in Q2CY’25, amid steady steel consumption. Increased infrastructure and auto sector activity are expected to be the primary drivers behind the surge. The steel industry decarbonisation drive globally will boost the usage of scrap, especially amid tightening carbon regulations affecting international trade.

In terms of country-specific trends, first, China could experience a drop amid speculation regarding steel production cuts. The EU and the US are likely to ramp up scrap usage. Japan and South Korea may continue to witness lower usage, as steel demand remains depressed. Solid market fundamentals are expected to support increased consumption in India even as steel production gains momentum following the implementation of the proposed safeguard duty.

Leave a Reply