- Eid slowdown impacts South Asian scrap markets

- Turkiye sees muted demand amid ample supply

South Asia’s imported scrap markets remained largely subdued amid the Eid holidays, financial year-end closures, and ongoing economic constraints. India faced a bid-offer disparity, which limited transactions, while Pakistan’s market stayed inactive, though there were expectations of a revival mid-week.

In Bangladesh, buyers remained on the sidelines due to letter of credit (LC) challenges, which delayed trade activity. Meanwhile, Turkiye saw a slight price dip, as EU-origin supply outweighed muted demand.

UK-origin shredded indicatives were stable d-o-d in India and Bangladesh, while they edged down in Pakistan. US-origin HMS (80:20) bulk prices dipped by $1/t d-o-d.

In the coming days, with market participants gradually returning post-holiday, attention will now shift to demand trends and price movements.

Overview

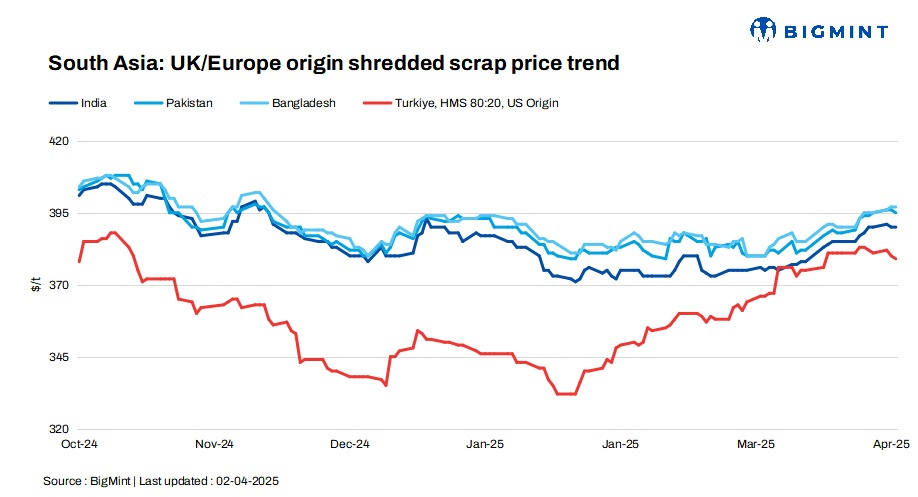

India: India’s imported scrap market remained moderate due to a lack of buying interest amid bid-offer disparities. Shredded offers stood at $390-395/t CFR, but buyer resistance above $385-388/t limited transactions. HMS 80:20 from the UK/Europe and West Africa was quoted at $360-370/t CFR, though buyers aimed for $355-365/t, further constraining trade.

Pakistan: Pakistan’s imported scrap market remained inactive due to the Eid holidays, with buying interest expected to revive by mid-week. UK/EU-origin shredded offers stood at $395-400/t CFR Qasim, but buyers eyed $390-395/t, while UAE-origin was offered at $400-405/t amid limited interest.

Domestic scrap ranged at PKR 140,000-145,000/t ($500-518/t), and mills operated at reduced capacity due to liquidity constraints and LC issues. While trading is set to resume, high global scrap prices and economic uncertainty may slow recovery.

Bangladesh: Bangladesh’s imported scrap market remained quiet post-Eid, with buyers staying on the sidelines until next month. LC constraints further limited trade, keeping domestic ship scrap at BDT 57,000-58,000/t ($471-479/t) exy, Dhaka rebars at BDT 82,000-83,000/t ($677-685/t) exw, and Chattogram rebars at BDT 85,500-86,000/t ($705-711/t) exw.

Turkiye: The Turkish imported scrap market saw a slight dip, amid muted demand and ample EU-origin supply during the Eid holidays. US-origin HMS (80:20) was assessed at $379/t CFR, down $1/t d-o-d, with tradable values for US/Baltic-origin scrap at $377-380/t CFR and EU-origin at $370-373/t CFR.

Market activity remained limited, though buying interest was expected to pick up post-holiday. EU suppliers were eager to sell, offering material for April-May shipments, while some mills continued seeking April cargoes despite the overall sluggish market.

Price assessments

India: UK-origin shredded indicatives were assessed at $390/t CFR Nhava Sheva, unchanged d-o-d.

Pakistan: UK-origin shredded indicatives edged down by $1/t d-o-d to $395/t CFR Qasim.

Bangladesh: UK-origin shredded indicatives remained unchanged d-o-d at $397/t CFR Chattogram.

Turkiye: US-origin HMS (80:20) bulk scrap prices were assessed at $379/t CFR Turkiye, down by $1/t d-o-d.

Leave a Reply