- Exports fall m-o-m as EU volumes decline

- Middle East sluggish ahead of Ramadan

- Dumping pressure eases but quota hurdles loom

Morning Brief: Continuing the downtrend seen for the entire 2024, India’s steel exports over January-February, 2025 cumulatively dropped a steep 41% to 1.17 million tonnes (mnt) against 1.97 mnt recorded in the same two months in 2024.

M-o-m, exports fell almost 16% in February 2025 to 0.54 mnt compared to 0.63 mnt in January.

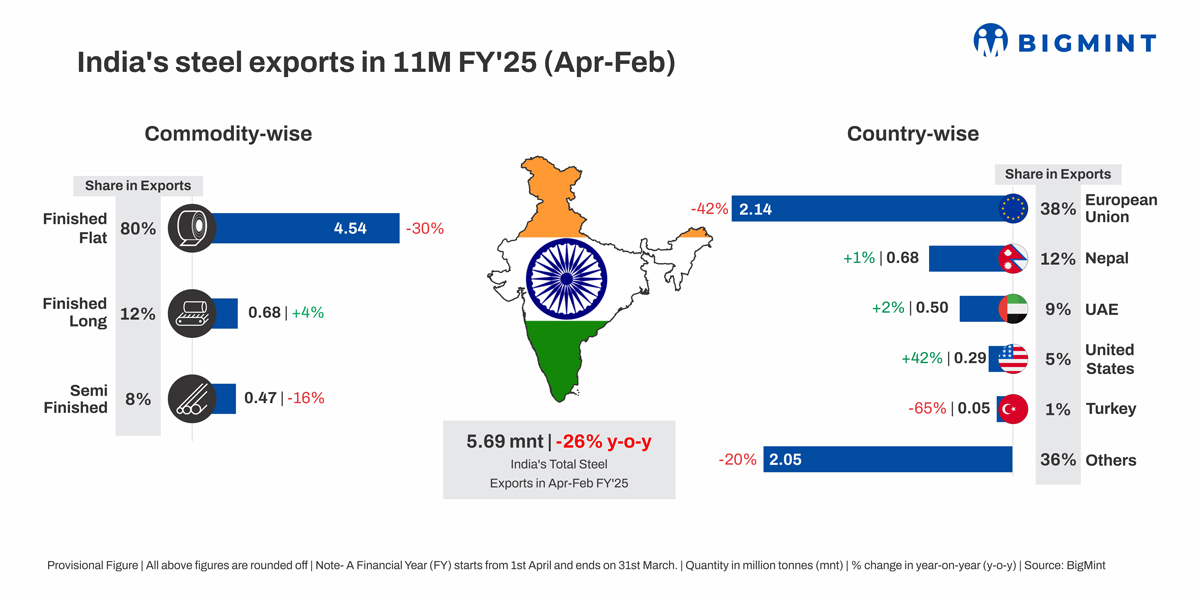

Commodity-wise break-up

Hot rolled coils (HRCs) and plates, which make up the bulk of India’s steel exports, have been showing a steady decline from around 600,000 tonnes per month in early 2024 to the current 83,000 tonnes. Y-o-y, these have plunged 84% to 0.17 mnt in January-February 2025, against a very robust 1.06 mnt.

Galvanised, which had gained a huge traction in 2024, fell 13% y-o-y to 0.30 mnt in the first two months (0.34 mnt).

Overall, flats fell 49% y-o-y to 0.90 mnt in January-February 2025 (1.77 mnt).

Finished longs dropped 35% in the first two months to 77,000 t (0.12 mnt). Semis, however, surged 147% to 1.92 mnt in the first two months (around 78,000 t) but plummeted 25% to 82,000 in February (0.11 mnt in January).

Country-wise break-up

M-o-m, exports were pulled down by Europe, where the bulk of the volumes have been going since the pandemic struck, but which dropped 18% to 0.24 mnt in February.

Volumes to the Middle East fell 22% m-o-m to 43,000 t (55,000 t).

Factors dragging down exports

China’s predatory onslaught continues: India continues to be no match against the Chinese dumping at predatory prices. Even though Indian offers have dropped off by over 16% y-o-y to an average of $530/t CNF Jebel Ali in January-February 2025 from $634/t in the same period last year, these are no match for the Chinese $499/t CNF Abu Dhabi in these first two months this year. It may be mentioned, China has been selling steel cheap across the world to offset its lack of domestic demand for months now.

Europe volumes fall as quota frenzy dies down: After the quotas frenzy died down by end of last month, Europe relapsed into a lacklustre mood, locked in a cycle of poor demand and high costs. Energy prices against soared northward to levels not seen since 2022. India shipped 1.2 mnt into its own quota last year. India was the most affected HRC supplier because of the safeguard review, with imports from the country falling by 23% to 225,000 t/quarter.

Middle East demand sluggish ahead of Ramadan: Demand from the Middle East became sluggish ahead of the onset of Ramadan from March. However, despite the market here being slow, in March, a major mill booked around 25,000 t and another deal closed for 10,000 t at around $515/t CFR. Prices remained range-bound at this level mid-March.

Outlook

The way ahead looks uncertain and complex for Indian exports with enablers and challenges inter-twined.

First, the European Commission has said it will tighten steel import quotas from April 2025, in a bid to give a leg-up to the domestic mills. The duty-free quotas per quarter will shrink by 12.1% to 1.90 mnt. What’s more, India’s quota will get truncated by 23%. New rules will impact India’s HRC, CRC and galavanised exports.

Secondly, on the other hand, a pre-disclosure to the EU’s anti-dumping investigation found no dumping on hot-rolled coil (HRC) imports from India, while imposing provisional duties on Egypt, Japan and Vietnam in a range of 6.9-33% from 7 April, 2025. It seems, Indian imports will be unconstrained, as they are subject to nil duty. But, with Vietnam subjected to a workable 12.1% duty, it can give India competition where the EU is concerned, going ahead.

Thirdly, Vietnam, in its turn, had launched an anti-dumping probe against Indian and Chinese steel exports last year. However, the findings eventually revealed, since the volume of investigated imports from India was insignificant (less than 3%), Indian products were excluded from the provisional anti-dumping duties. This can give Indian mills some respite and they can possibly resume exports to this Southeast Asian country.

Fourth, all eyes are now on China and its policies in the current year. The million dollar question now is, will China continue to aggressively export over 100 mnt of steel or will it slow down to help global markets stabilise?

Lastly, the 25% US tariffs on steel imports can have an indirect spin-off. Other countries will possibly direct their exports to India. The US, in 2024 imported $33 billion of steel. China, South Korea and Japan were key players, apart from Canada and Mexico, of course. There could be an 85% reduction in steel exports to the US and these countries are likely to find new geographies and India is a suitable destination, especially for Japan and Korea because of the FTAs. Dumping risk intensifies and steel prices, already at four-year lows, can further head downwards.

Leave a Reply