- Refined zinc production falls 2.6% in 2024

- Global lead mine production up 1.9% y-o-y

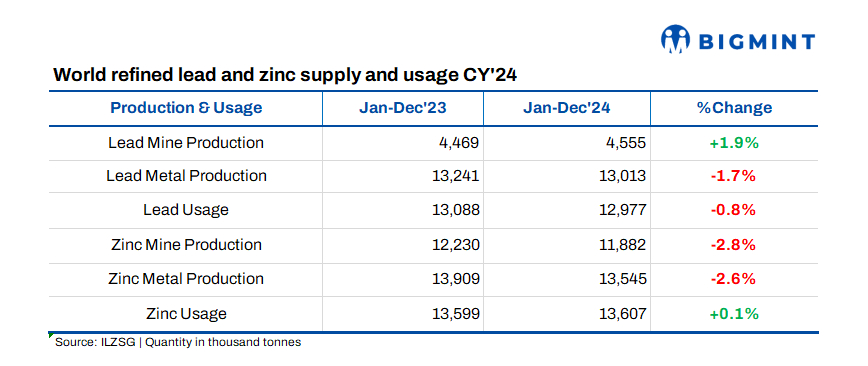

The International Lead and Zinc Study Group (ILZSG) has unveiled preliminary figures on global lead and zinc supply and demand for CY’24 (January-December of 2024).

Refined zinc supply, usage

ILZSG has shared early data showing a zinc deficit in 2024. Global inventories fell by 31,000 tonnes (t), totalling 791,000 t, while the refined zinc market recorded a deficit of 62,000 t.

Global zinc mine production dropped by 2.8%, driven by declines in Canada, China, South Africa, and Peru, where significant reductions occurred at the large Antamina mine. Production also fell in Europe, mainly due to decreases in Ireland and Portugal. However, production increased in Bolivia, Mexico, and the Democratic Republic of Congo, where Ivanhoe Mines started operations at the Kipushi mine in June.

Refined zinc metal production dropped by 2.6% in 2024, mainly due to limited concentrate availability. Reductions in China, Japan, South Korea, the Netherlands, Norway, and Russia were partially offset by increases in France, India, and Germany, where the Nordenham smelter resumed production in March. Canada’s output was impacted by a fire at Teck Resources’ Trail operations in September and modernisation at Glencore’s CEZinc refinery, completed in Q4.

Increases in apparent usage of refined zinc metal in Brazil, India, South Korea, Mexico, Turkiye, and Vietnam were largely offset by reductions in China, Europe, and the United States, resulting in a negligible overall global rise of 0.1%.

Chinese imports of zinc concentrates fell by 13.1% to 1.96 million tonnes (mnt) in 2024. Net imports of refined zinc rose by 15.5% to 0.429 mnt.

Refined lead supply, usage

ILZSG has reported on global supply of refined lead metal in 2024. Global supply exceeded demand by 36,000 t, leading to total reported inventories rising by 104,000 t to 549,000 t by year-end.

Global lead mine production rose by 1.9%, driven by growth in Australia, Bolivia, Bulgaria, Kazakhstan, Peru, Sweden, and the United States. These increases were partially offset by declines in China, Ireland, Portugal, and South Africa.

Refined lead metal production fell by 1.7%, mainly due to declines in China and Canada, where scheduled maintenance at Teck Resources’ Trail operations in Q2 impacted output. However, production increased in Australia, India, Japan, and the Republic of Korea. In Europe, output grew by 2.1%, largely due to rises in Bulgaria and Italy, despite declines in Poland, Sweden, and the UK.

Global demand for refined lead metal fell by 0.8%, as increases in Brazil, India, South Korea, and Vietnam were countered by decreases in China, Europe, Japan, Turkey, and the United States.

China’s net imports of lead concentrate rose by 9.6% to 712,000 t. Additionally, net imports of refined lead metal reached 126,000 t, a shift from net exports of 183,000 t in 2023.

Leave a Reply