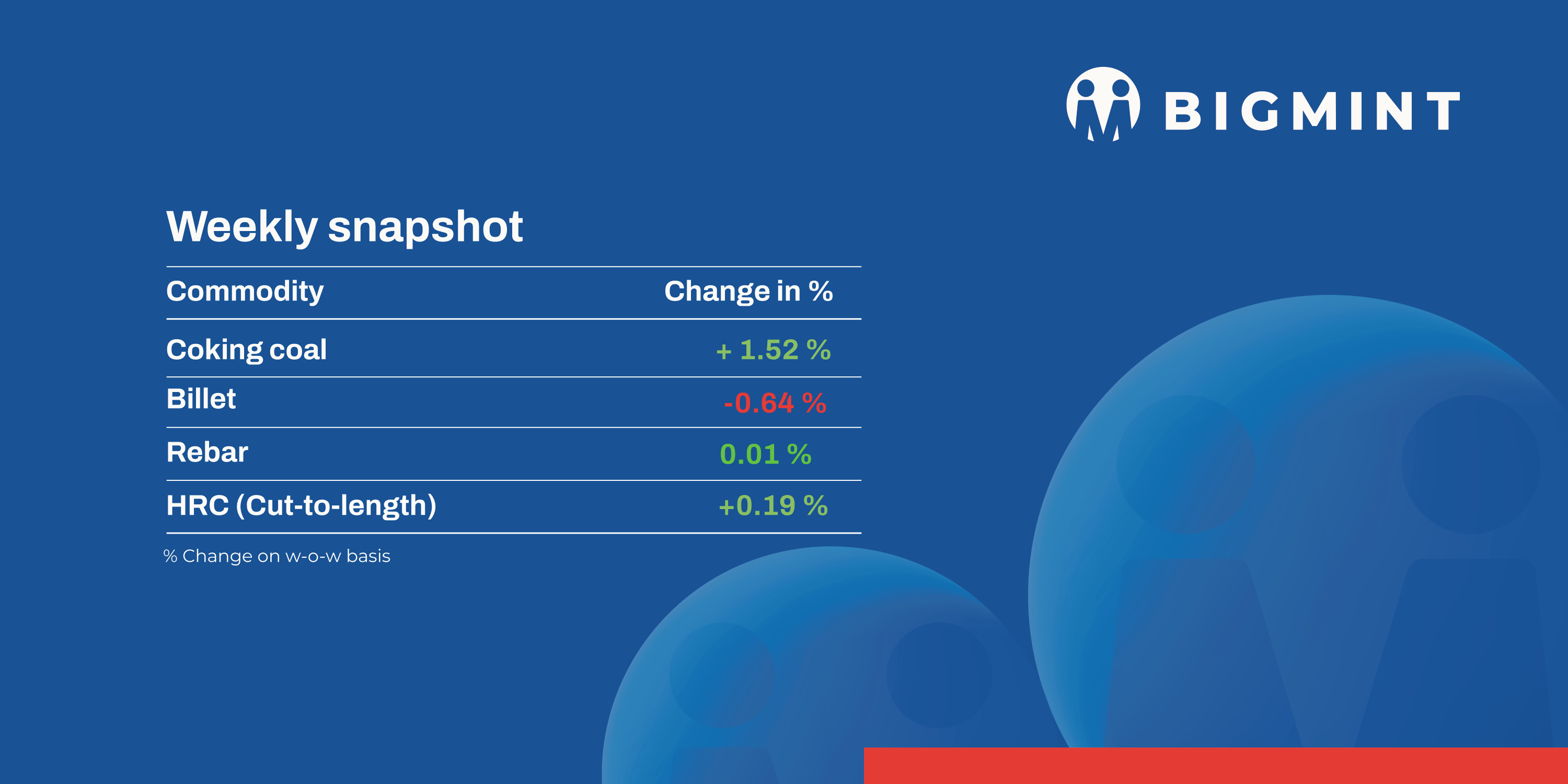

In the domestic steel market in week 6 (3-8 February) of 2025, semi-finished steel prices declined by INR 100-700/tonne (t). Flat steel prices edged up as Tier-I mills hiked prices, while the rebar market saw regional variations.

Iron ore and pellet

BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, decreased by INR 100/t w-o-w to INR 9,800/tonne (t) DAP Raipur on 7 February 2025. Around 25,000 pellet deals were recorded in the Raipur region this week. Pellet offers remained supportive with plants increased prices to INR 9,700-9,900/t exw recently.

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $0.5/t w-o-w to $68/t FOB east coast, India, on 6 February. A deal of 80,000 t of iron ore fines (Fe56-57%) was concluded from the eastern coast at $66/t FOB in this publishing window.

India pellet (Fe 63%, 3% Al) export index (FOB east coast rose by $0.5/t w-o-w to $105.5/t on 7 February. A domestic pellet maker concluded an export deal for around 100,000 t of pellets (Fe 63%, 2% AL2O3) at $108-110/t FOB India this week, sources informed BigMint.

Coal

South African thermal coal prices at Indian ports remained under pressure, with RB2 at INR 8,650/t and RB3 at INR 7,250/t ex-Gangavaram, as weak demand and limited trade kept prices subdued.

Thermal coal inventories at Indian ports increased by 2.4% to 13.66 mnt in week 5 of CY’25, reflecting steady inflows despite weak buying interest.

India’s domestic met coke prices rose this week, with 25-90 mm BF-grade at INR 34,000/t exw-Jajpur and INR 31,500/t exw-Gandhidham, driven by tight supply and active trades.

Ferrous scrap

India’s imported scrap market remained under pressure throughout the week as a weaker rupee, rising freight rates, and subdued steel demand dampened buying interest. Shredded scrap prices in India settled at $373/t CFR, marking a 1% decline from the previous week’s $375/t. The rupee’s depreciation against the dollar made imports costly, while weak domestic steel market support and an uninspiring Budget further hurt sentiment.

Buyers largely stayed on the sidelines, leading to limited deal activity, with bid-offer mismatches persisting.

Suppliers favored Pakistan for better prices, while strong US domestic demand limited exports to India. Rising freight rates, especially from the US West Coast, surged from $1,800/t to $2,400/t, further widening the bid-offer gap and restricting deals.

Approximately 7,000-8,000 t of scrap were booked, including 4,500-5,000 t of HMS (80:20) from South America, Wes Africa, Chile, Mauritius, Australia has booked at $345-360/t and 1,500-2,000 t of shredded scrap from the Australia and Mauritius at $360-365/t, and 1,000-1,5000 t of MS Turning, HMS-LMS mix and Bushling scrap.

Ferro Alloys

Silico Manganese

Indian silico manganese prices increased by INR 1,100/t ($13/t) w-o-w to INR 71,400-72,700/t ($825-840/t) in key regions of Durgapur, Raipur and Vizag. Post rise in MOIL’s price revisions for manganese ore for Feb’25 deliveries, a significant impact on the domestic silico manganese prices was seen.

Ferro Manganese

Indian ferro manganese (HC 70%) prices went up by INR 500/t ($6/t) to INR 75,000/t ($866/t) exw in Durgapur and stood at INR 75,400/t ($871/t) exw Raipur up by INR 900/t ($10/t). Prices increased due to a combination of factors, prices in the domestic market have risen. Limited supply has been a significant support for these prices.

Ferro Silicon

Indian ferro silicon prices dropped, by INR 1,300/t ($15/t) w-o-w to INR 100,900/t ($1,166/t) exw-Guwahati . Prices also dminished by INR 1,700/t ($20/t) in Bhutan too at INR 100,400/t ($1,160/t) exw. Bhutanese players announced a reduction of INR 4,000/t ($46/t) m-o-m in ferro silicon prices which reached INR 100,000/t ($1,148/t) exw for Feb’25 sales. Persistent bid-offer gaps and weak demand in the previous month have led to this price reduction, as noted by BigMint.

Ferro Chrome

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were largely steady with slight decline by INR 300/t ($3/t) w-o-w at INR 97,300/t ($1,124/t) exw-Jajpur.Prices were steady as routine trading activities were carried out at current prices.

Semi-Finished

Indian semi-finished steel prices showed downtrend, as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 100-700/t across regions, with a major decrease of INR 700/t seen in the Bhavnagar market. However, sponge iron prices showed mixed trend, almost all key locations decreased by INR 100-400/t, with a major decrease of INR 400/t seen in the Rourkela and Raigarh market. While Mandi Gobindgarh market showed up by INR 200/t

Indian DRI (Direct Reduced Iron) export offers decreased by $5 for CPT Raxaul, reaching $343/t while, CPT Benapole offers decreased by $4 stood at $339/t.

Finished Long Steel

IF-rebar: India’s induction furnace route finished long steel prices declined slightly week-on-week amid limited region-wise trading activity. Buying remained need-based in the early week but slowed later due to market uncertainty. Manufacturers maintained stable prices or offered trade-level discounts based on orders. Smooth dispatches of previously booked materials have reduced mill inventories to around 8-10 days. Market participants expect prices to remain range-bound in the near term.

On a weekly basis, in rebar steel prices witnessed fall of INR 100-1,100/t across the regions except in Bangalore and Hyderabad market where prices upside by INR 100/t and 500/t respectively as per BigMint assessment shows.

The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 41,900-42,300/t exw Raipur, INR 46,500-47,100/t exw Jalna.

Trade reference price of heavy structural steel for base size 150mm channel stands at INR 43,800-44,200/t exw Raipur.

Trade reference prices of wire rod hovering at INR 43,000-43,500/t ex Raipur.

BF-rebar: Indian tier-1 mills have increased rebar list prices by up to INR 1,000/t for early-February 2025. Following this, trade-level BF-rebar prices witnessed an increase w-o-w across markets. Meanwhile, demand in traders’ market continued to remain slow.

Current week’s rebar prices (12-32mm) in the trade segment rose by INR 500/t w-o-w to INR 52,700/t exy-Mumbai. Prices are exclusive of GST at 18%.

In the projects segment, prices rose w-o-w to around INR 49,500-50,500/t FOR Mumbai basis.

Flat Steel

Indian tier-I steel mills have raised HRC and CRC prices by INR 1,500-2,000/t for February 2025 sales, compared to end-January levels. While several mills have confirmed the hike, official announcements from others are awaited.

List prices of HRCs (2.5-8 mm, IS2062, Gr E250, Br.) stood at INR 48,200-49,800/t exy-Mumbai, while those of CRCs (0.9 mm, IS513 CR1) hovered at around INR 53,000-56,000/t. These prices exclude the 18% GST.

BigMint’s benchmark assessment prices (bi-weekly) of HRCs (IS2062, Gr E250, 2.5-8 mm) increased margnally by INR 200/t w-o-w to INR 48,700/t ($543/t). However, CRCs (IS513, Gr O, 0.9 mm) remained stable at INR 53,700/t, respectively, on 4 February 2025. The prices quoted are exy-Mumbai, exclude 18% GST, and are for cut-to-length (CTL) deliveries.

Market buzz indicates that JSW Vijayanagar’s HSM2 is undergoing major maintenance for 20-30 days, with an estimated production loss of 150,000-170,000 t. Additionally, AM/NS India has shut down its Corex-2 plant, impacting production capacity. As per market sources, other mills might also scheduled some maintenance this month.

As per BigMint’s vessel line-up data, the cumulative import volume touched 4,71,623 t in Janaury 2025. It was 4,73,222 t in December and 5,71,656 t in November.

BigMint’s India hot-rolled coil (HRC, SAE1006) export index (for the Middle East and Vietnam) remained stable w-o-w supported by a recent export deal from India to the Middle East (ME). Current prices are at $505/t FOB east coast India. However, European demand continues to remain subdued due to sluggish market sentiments and ongoing anti-dumping investigations.

Leave a Reply