- Drop of $4-5/t seen in high-grade fines spot and future

- Chinese steel mills continue production cuts

- No iron ore export deals from India in last one week

The iron ore seaborne market remained under pressure in the last few days amid the lower demand from the Chinese steel mills for the raw material amid the ongoing production cuts. The higher inventory level at Chinese ports and weak steel demand in the Chinese market kept Indian fines southwards, leading to a drop in the transected volume and prices.

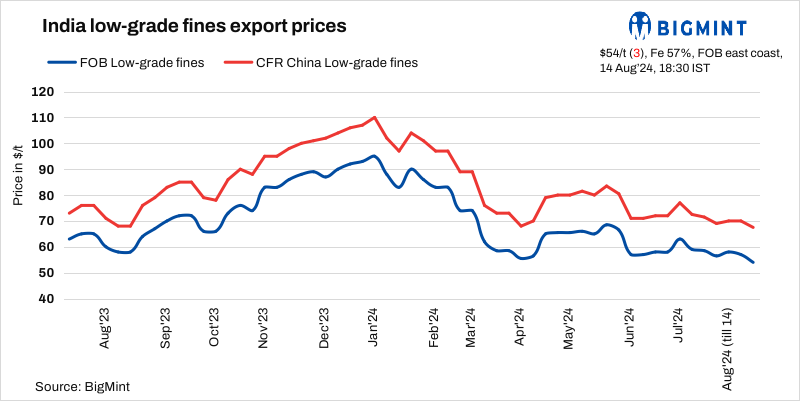

BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index decreased by $3/tonne (t) w-o-w to $54/t FOB east coast on 14 August 2024. The market remained silent as Indian sellers remained away from the market amid bids and offers disparity following the higher domestic ex-mines prices along with logistic and port charges.

Miners from Odisha said the bids from buyers were below $55/t FOB East Coast in the last few days. The inquiries also decreased from China as sellers’ prices were not accepted by the buyers which prevented the deals from India. Major miners are selling their material at domestic prices even at low prices amid the wide gap in domestic export realisation and current domestic realisation is way better against the seaborne market bids.

Sources stated that the ongoing production cut by Chinese mills due to the lower downstream steel demand has impacted the seaborne market as mills showed least interest for any seaborne trade against the ports side which is available at cheaper prices.

Iron ore inventories in China’s major ports dropped by 1.3 mnt to 150.4 million tonnes (mnt) on 8 August compared to the last week, according to SteelHome data.

Another exporter indicated that Indian sellers must await an uptick in market sentiments in the coming days. Given the current conditions in the seaborne market, prices for lower-grade fines are expected to hover around $65-70/t CFR China at least until the end of August. As a result, we have chosen a wait-and-watch strategy and will refrain from selling material in the export market for the next few days.

Recently, mills, which are experiencing shrinking profits, have become more interested in medium and low-grade fines.

Price indicators

- No confirmed deal was reported from the East Coast this week and taken into price calculation under T1 trade and given 0% weightage in the index calculation. For detailed methodology Click here.

- BigMint received fifteen (15) indicative prices in the current publishing window and thirteen (13) were considered for price calculation as T2 inputs and given 100% weightage.

Factors impacting the seaborne market-

- Iron ore spot prices dropped w-o-w: The benchmark iron ore fines dropped by $4/t w-o-w to $98/t CFR China on 13 August. Prices remained under pressure amid weak market fundamentals with limited buying activity and reduced demand due to maintenance shutdown by mills leading to further production cuts.

- Portside offers in China down w-o-w: Portside offers of Indian iron ore fines (Fe57%) in China dropped by RMB 15/t ($2/t) w-o-w on 14 August. Offers were recorded at around RMB 560/t ($78/t) at Qingdao Port, including all import taxes and port charges. D-o-d, portside prices decreased by RMB 10/t ($1-1.5/t) today.

- DCE futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2025 contract dropped by RMB 36/t ($5/t) w-o-w to RMB 713/t ($100/t) on 14 August. On a d-o-d basis, futures prices fell by RMB 21.5/t ($2/t) against RMB 734.5/t ($103/t) yesterday.

Outlook

Seaborne iron ore export prices are expected to remain under pressure in the near term amid the ongoing production cut by the Chinese steel mills and lack of inquiry in the seaborne market.

Leave a Reply