- Tier-1 mills cut both HRC, rebar list prices

- NHAI quality show-cause impacts IF mills

- Prices likely to remain flat in short term

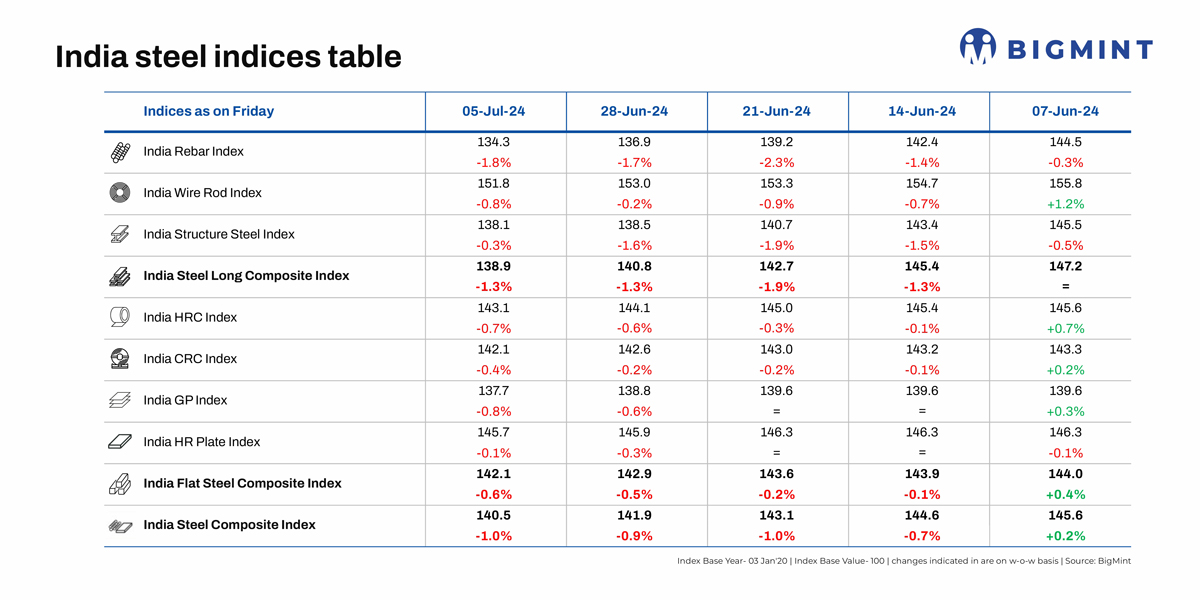

Morning Brief: The falling streak in India’s steel prices continued. The BigMint India Steel Composite Index dropped further for the fourth week in a row to close on 5 July, 2024 at 140.5 points, a w-o-w dip of 1%. This is a 12-week low since 12 April, 2024’s 139.7.

The bearish streak is sustaining amid gloomy global sentiments, escalated freights and lacklustre domestic demand. Tracking the sentiments, both the longs and flats sub-indices also fell w-o-w.

Factors that impacted index last week

Mills, trade segment drop prices: It was a down syndrome across rebars. Tier-1 mills announced a reduction in their list prices for early July 2024 sales. Prices dropped by as much as INR 1,000-1,500/tonne ($12-18/t) to INR 55,000-55,500/t ($659-665/t). On cue, trade-level blast furnace (BF)-grade prices dropped by around INR 1,100/t ($13/t) to settle at INR 55,200/t ($661/t) levels, ex-Mumbai, minus 18% GST.

Project segment prices hovered at INR 53,500-54,000/t ($641-647/t) against the previous week’s INR 55,500-56,500/t ($665-677/t).

Demand remained dull, especially with the monsoons having set in. Outdoor construction activity has waned sharply, impacting demand. That apart, the post-election expected turnaround eluded markets. Plus, induction furnace (IF) prices also dropped, further dragging down the BF material as well.

IF prices impacted by NHAI notice: The induction furnace segment experienced continued sluggish sales amid dull demand for semis and finished steels. The monsoon is dampening demand but the recent NHAI show-cause notice to IF mills on quality issues has dealt a body blow to demand. Prices, in any case, had dropped to four-month lows last week. The market expected these to have bottomed out and had moved to the side-lines, adopting a wait-and-watch mode. This resulted in dull sales last week. But, it seems, IF rebars are yet to see the bottom of the barrel. Prices slid a further INR 800/t ($10/t) w-o-w to INR 48,100/t ($576/t) ex-Mumbai on the weekend.

With further declines, the gap with BF rebars has widened to INR 6,500-7,000/t ($78-84/t) while inventories for the former are idling for 12-15 days against 6-8 in April.

Tier-1 mills cut list prices in flats: In flats, the story was similar, with some tier-1 mills cutting down their list prices of hot rolled coils by INR 1,000-1,750/t ($78-84/t) for July sales. Cold rolled coils (CRCs) fell by INR 1,000-1,500/t ($12-18/t). Post-reduction, HRCs hovered at INR 53,000-53,500/t ($635-641/t) and CRCs, at INR 60,000-60,500/t ($719-725/t).

The price drop can be attributed to a few factors. One, an increase in domestic HRC production over November 2023 till March 2024, pumped up the volumes and depressed prices. The trade segment was also sitting on large volumes but with few takers. This forced mills to deviate from their usual rainy season maintenance shutdowns and bring these forward to April-May. Thus, HRC output levels dropped from 4.86 million tonnes (mnt) in March to around 4.23 mnt in April. Resultantly, supplies were also rationalised.

Two, cheaper imports have been exerting tremendous pressure on mills with India set to become a net steel importer in Q1. Domestic prices averaged INR 53,533/t ($641/t) in Q1FY’24 (April-June) against the landed INR 51,133/t ($613/t) from FTA countries and INR 48,933/t ($586/t) from China. Obviously buyers veered towards the cheaper alternatives, keeping Indian prices under pressure.

Exports continue to remain dull: India mills continued to hold their export offers and for three reasons. One, demand dullness sustained post-Eid, especially in the Middle East. Two, Chinese offers continued to drop (those to Vietnam fell $10/t w-o-w), making these further inviable for Indians. Three, demand from the EU is persistently down. The market there is over-supplied and domestic mills are pressuring down prices. Plus, buyers and sellers have moved to the side-lines, trying to gauge the effects of the safeguard regime that came into force from July.

Outlook

In longs, IF mills are on the backfoot in the face of the NHAI show-cause. This may have a further spin-off on rebar prices. On the other hand, a substantial IF market share may shift to the BF mills and this may keep prices here supported even if these do not recover from the current levels.

In flats, with mills having just announced their price direction, not much movement is expected in the near term. In exports, factors are not likely to change soon, which may also have a downward bearing on domestic prices.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply