- Iron ore rides post-Labour Day restocking spree

- Longs still on backfoot, scrap feels Turkiye heat

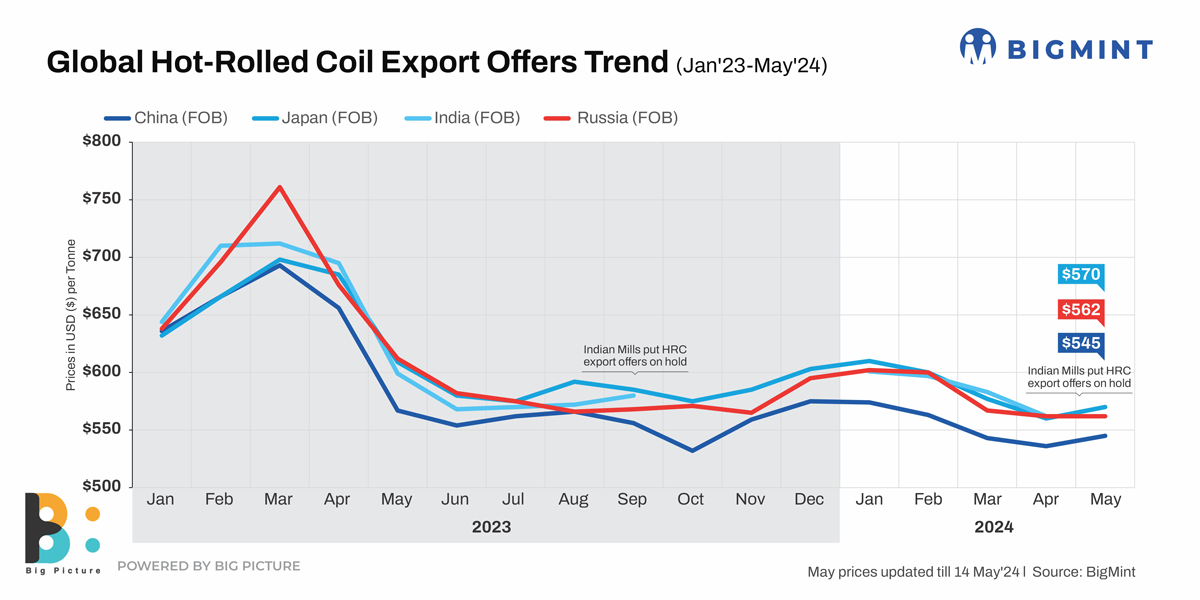

- Indians prioritise domestic market, withdraw offers

Morning Brief: Most global steel and raw material prices, after falling further last month, moved up slightly in May 2024, reveals data maintained with BigMint. Scrap and rebar showed a dip while the rest upped, but all moved in a highly narrow range. Iron ore rose a mere 5% but which was the highest gain m-o-m amongst all commodities.

In May, Chinese hot rolled coil (HRC) offers, after showing a steady decline since December 2023, rebounded, albeit by a marginal 1.49% or $8/tonne (t) to a two-month high of $545/t against $537/t in April. Japanese offers took cue from China to rise $9/t or 1.6% to $570/t ($561/t) while Indian mills withdrew from the market amid better home realisations and unviability in export offers.

In longs, Turkiye’s rebar remained stable, dropping a mere $3/t to $589/t ($592/t). Black Sea billet export offers also remained flat, upping $2/t to $504/t ($502/t).

All prices are on FOB basis.

In raw materials, Fe62% iron ore fines, CFR China, rose 5.4% to $117/t ($111/t), while the premium HCC coking coal from Australia, CFR India, headed north by a slight 1% or $3/t to $259/t ($256/t). Coking coal had breached the psychological $300/t barrier in September last year. From April, it has again fallen below this threshold.

HMS 80:20 scrap, CFR Turkiye, fell almost 1% to $383/t ($386/t) in the month under review.

Factors that impacted prices in May’24

China keeps global flats prices supported: Chinese HRC prices rose on two reasons. First, steel futures on the Shanghai Futures Exchange (SHFE) rose post-Labour day holidays, as Chinese market participants tried to push up prices in the absence of offers from other competing origins. Secondly, steel inventories also saw a slight decline. As per a source, in end-April, social (outside of mills) inventory in 29 key cities was at 13 mnt, a m-o-m decrease of 16%.

On cue, several steel majors upped their domestic offers. For instance, Chinese steel behemoth Baosteel increased HRC prices by RMB 50/t ($7/t) m-o-m for June sales. Taiwan’s China Steel Corporation (CSC) also upped June sale prices–HRCs, HR plates, and CRCs were higher by TWD 300/t ($9/t).

Vietnamese steel majors, keenly watching Chinese prices, also moved in fast. Formosa Ha Tinh increased HRC prices by $15/t m-o-m for July shipments amid the rise in global imported and domestic HRC offers. Its domestic competitor, Hoa Phat, increased its benchmark HRC (SAE1006, non-skinpassed) prices by $27/t for July sales.

However, Chinese futures, after the slight uptrend in early-May, have been volatile.

Indian mills focused on higher domestic realisations: Indian mills, on the other hand, kept their export offers on hold for four consecutive weeks till mid-May. Weighed down by inventory since early this year, especially in flats, mills strategically cut production or opted for maintenance and effected interim price hikes over the last couple of months. The production cuts led to lesser supply and supported the price hikes, which helped to increase domestic realisations. For instance, ex-Mumbai trade-level HRC prices in April remained flat m-o-m at INR 52,630/t ($630/t) whereas export offers hovered at $562/t FOB. This allowed mills to avoid export allocations.

Turkish rebars slip on low finished demand: The Turkish rebar slipped slightly amid a couple of reasons. One, the Turkish economy has somewhat struggled since the elections were held in end-March. The government is trying to keep the lira supported which can be a drag on exporters. Thus, from 32.36 levels to the dollar in April the TRY has regained a bit of ground at 32.32 till date in May. A stronger TRY means lesser forex earnings for exporters. Two, the Turkish Ministry of Commerce has restricted exports of 54 categories of products, including rebars, to Israel. This is a huge disadvantage for rebar exporters as Israel is amongst the largest markets for such products for Turkiye.

Black Sea billets sluggish as competition eases: Black Sea billet prices have remained sluggish mainly because of the lack of competition with the onset of the Red Sea crisis which has made business more localised. Secondly, Turkiye, which is the largest market for Russian billets, has seen demand for finished steel dropping in a sluggish economy. Thirdly, the global billets trade has failed to pick up post-the Labour Day holidays because supply in longs continues to overshoot demand.

Chinese restocking keeps iron ore supported: Steel prices rose as Chinese market participants returned from the Labour Day holidays, which had a cascading effect on iron ore. Secondly, Chinese buyers started focusing on post-holiday purchasing, mostly for June-arrival cargoes, expecting a strong uptrend as the holidays ended. Thirdly, higher crude steel output also supported Chinese iron ore import prices. The average daily crude steel output of CISA-affiliated mills stood at 2.199 mnt in late-April, up 3.8% from 2.119 mnt in mid-April and up 3.7% m-o-m against 2.121 mnt in late-March.

Scrap dips amid lack of Turkish demand: A rush of supplies from the US and Baltic region gave Turkish importers opportunities to lower prices especially since EU suppliers were also in the fray. EU sellers eventually either held back or found it challenging to reduce beyond $380/t CFR. But Turkish procurements were low because buyers were hamstrung by lack of demand for finished steel. Turkish automobile sales fell in April while white goods are facing stiff competition from Chinese products.

Coking coal ups marginally on Chinese interest: Australian premium hard coking coal prices edged up on increased appetite from Chinese buyers as domestic coal prices shot up. Secondly, Indian buying is also on an uptrend amid pre-monsoon restocking demand.

Outlook

Flat steel prices may remain supported in the near term as mills have already hiked prices for June-July deliveries. Firmer finished prices may also support iron ore and coal.

However, longs may continue to battle the twin challenges of low demand and supply glut.