- Supply crunch, higher domestic prices drive EU demand

- ME, SE Asia markets prefer cheaper Chinese material

- Indian steel exports may see hurdles in current calendar

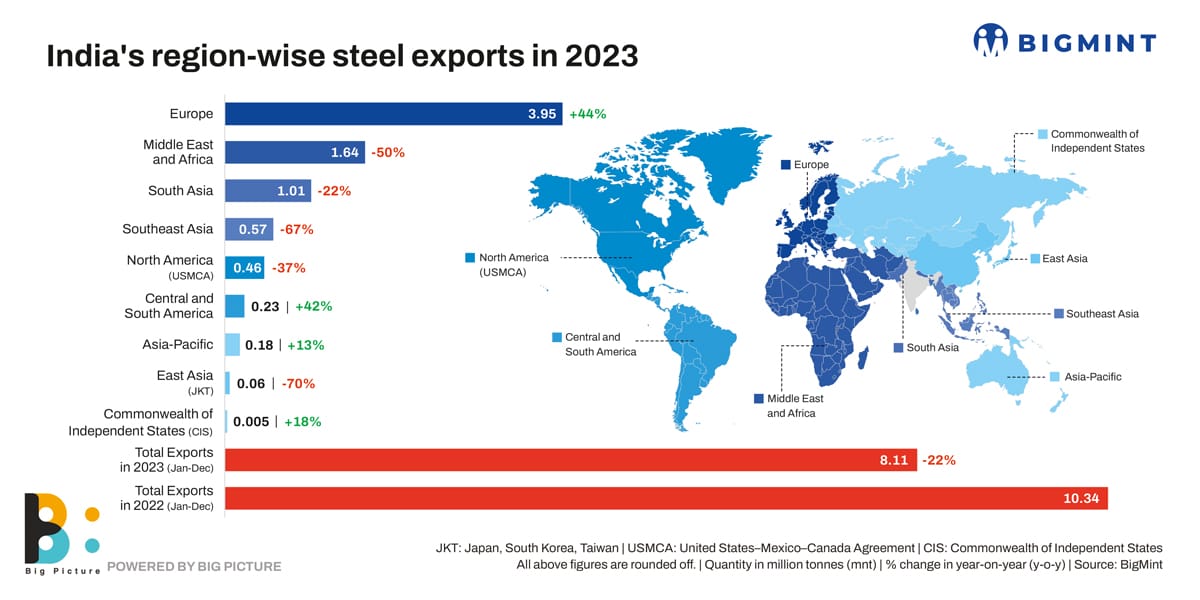

Morning Brief: India’s steel exports in calendar 2023 (CY’23) were driven by the European Union (EU) which showed a substantial y-o-y growth. However, India’s overall volumes fell 22% in CY’23 to around 8 million tonnes (mnt) against 10 mnt in CY’22 because most of the other key importing geographies showed sharp y-o-y declines.

Multiple factors boost exports to EU: This geography showed a considerable 44% increase y-o-y to almost 4 mnt in CY’23 against 2.75 mnt in CY’22.

Several factors helped to push up the volumes here.

One was the increase in quotas for India post-the sanctions imposed on Russian steel exports to the EU. Secondly, mills received higher realisations in the well-paying EU market and thus concentrated more here. Indian HRC export offers to the EU were at a yearly average of around $726/t, CNF EU in 2023 – much higher than those realized in the Middle East or Southeast Asian markets.

Thirdly, the EU’s domestic steel prices rose amid an increase in the cost of production. Plus, many of the key mills shut down some of their blast furnaces due to carbon emission issues, which decreased supply. In fact, worldsteel data reveals that the EU-27’s crude steel production fell 7.4% in CY’23, creating a case for the price hikes. In general, tradeable prices for HRCs in northern Europe in September 2023 were hovering at $676-697/t ex-works whereas in November last year these rose to around $727-748/t and in February 2024, further to $797-818/t in dollar parity.

Lastly, the US, a major market for the EU, offered good prices which also encouraged end-buyers in the latter to import from India, Vietnam etc, and value add for further sales to the US.

China lures away Middle East buyers with cheaper offers: This region, which recorded the highest volumes of steel exports from India in CY’22, at over 3.30 mnt, saw the same plunging 50% to a little over 1.60 mnt in CY’23. This was mainly because China had captured this market and how! Chinese steel exports to Middle East (ME) and Africa rose 44% y-o-y to 26 mnt in CY’23. ME buyers favoured Chinese materials because of the price factor. These averaged $625/t CNF Abu Dhabi last year compared to the Indian average of $663/t CNF Jebel Ali (Dubai), cheaper by $38/t.

Of course, China had been a prolific exporter last year, goaded by inadequate demand and falling prices at home.

Drop in Vietnam’s imports pulls down SEA volumes: Exports from India to Southeast Asia fell a staggering 67% to a mere 0.57 mnt last year compared to 1.74 mnt in CY’22. Here too China played a key role in taking away a traditional market like Vietnam from India with aggressively low offers.

India steel exports to Vietnam – 0.32 mnt in CY’23, down over 70% y-o-y. In this period, exports from China to Vietnam rose 70% to 9.25 mnt (5.50 mnt in CY’22). Interestingly, Vietnam had seen imports from India even crossing 0.20 mnt in certain months alone in 2021.

Although Vietnam’s own domestic market was dull, it was exporting decent volumes of HRCs as well as value-added products to the EU, US, Mexico and other countries without resorting to dumping, a source informed BigMint.

Outlook

CY’24 is likely to emerge as a challenging year for Indian mills in terms of exports and for multiple reasons. One, China may continue to remain an aggressive exporter in the current calendar, if its home demand and prices fail to pick up. Two, even though the EU offered solace in terms of decent imports last year, the quotas do act as a barrier for Indian mills. Plus, the full implications of the carbon border adjustment mechanism (CBAM) are still being studied and the same may also have limiting aspects for Indian mills, going forward. CBAM is a EU carbon tariff and will see full-fledged implementation from 2026 but the process kicked in from October 2023. Three, Indian mills will be expanding capacity in the near future which will increase supply and may force mills to eye exports in what may still be a highly competitive environment. Lastly, Southeast Asia, which was predominantly an importing geography, is seeing capacity additions, a scenario that may alter market dynamics and impel it to become an exporting entity and compete with India.