- Each country now heavily influenced by its own demand dynamics

- Japan exploring better prices amid high domestic demand

- Spread may narrow as both Turkiye and Japan explore higher offers

Morning Brief: It seems Turkiye, the largest ferrous scrap importer in the world, and Japan, the second largest exporter of the same, are continuing to walk in opposing directions as far as prices are concerned.

Turkiye buys its bulk H2 mainly from the US and the UK whereas Japan sells high-grade material to Southeast Asian countries Korea, Vietnam, and Taiwan because of their geographical proximity. Korea, of course, is Japan’s largest buyer because the latter sells high-grade, mainly automotive scrap, much in demand in the former. But, Turkiye follows the middle path and can do with lower grades, for which the US is an ideal supply source.

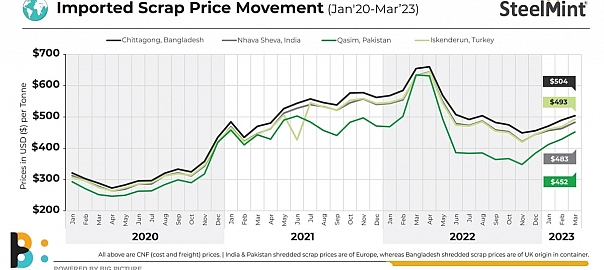

But the prices at which Turkiye buys from the US and Japan exports to Southeast Asia have become global benchmarks. Since South Asia (India, Bangladesh and Pakistan) also buys from the US-UK, they too are influenced by Turkiye.

Factors behind the “decoupling” of Turkey-Japan ferrous scrap prices

Swayed by differing market dynamics: This “spread” between the benchmark import and export prices are keenly watched by stakeholders in the global ferrous scrap trade. The same had widened with the onset of the Russia-Ukraine war, when Turkey was buying at $630/t levels CFR over March-April, 2022 whereas Japan was commanding an average $473/t FOB plus $20-22/t in freight over these two months.

Thereafter, both countries saw prices driving down but impelled by different reasons. Turkey’s crude steel production dropped because of plunging steel demand, high energy prices and inflation in Europe. Japan, on the other hand, was unable to command higher prices because of low steel demand in Vietnam and South Korea’s interest in its own discounted domestic scrap. During the middle of last year, Japan’s export offers remained dampened because of its higher domestic demand while buyers awaited further discounts.

These factors gave enough room last year to believe that Turkiye had indeed “decoupled” from Japan. Each geography was now swayed by its own demand dynamics and set prices accordingly.

For instance, as per information available, in 2017, the average gap between FOB prices of H2 bulk scrap exported from Japan to Korea were at a discount of $15/t to that of HMS 1&2 imported into Turkiye from the US. However, in 2022, the discount widened to about $35/t and currently is resting at an even higher $40-45/t despite Japanese prices having recouped to over $420/t CFR levels against Turkiye’s over $450/t CFR.

2) Japan looks for higher prices: On the other hand, Japan remained insulated from the high energy prices, which were predominantly a European phenomenon and is now naturally looking for a better price from its end-buyers. Lately, the decoupling is more pronounced as Japan’s domestic market is strong because of the leaning towards higher scrap usage amid the decarb drive. Naturally, under such circumstances, Japanese scrap sellers raised their offers in early March just ahead of the Kanto tender (to be concluded on 9 March), which is the price-setter in both the domestic and export markets.

SteelMint’s last assessment for Japan’s H2 scrap export offers stood at JPY 54,000/t FOB ($398/t), up JPY2,000/t ($15/t) w-o-w while the February Kanto benchmark was up JPY 53,362/t ($392/t) against JPY 50,932/t ($374/t) in January.

Japan cannot sell to a presently lucrative market like Turkiye because the latter’s geographical location makes it unviable, especially with escalating freights. Hence, Japan is looking to tap into South Asia, especially India, where prices have been upping since January, in a bid to garner meatier margins.

3) Earthquake triggers change in Turkiye market dynamics: The next major event after the Russia-Ukraine war that changed Turkiye’s scrap buying dynamics is the devastating February 2023 earthquake. With major portions of the country reduced to rubble, around 4 million tonnes of rebars are reportedly required to complete the reconstruction work. This means, the beleaguered country will require copious amounts of scrap, pig iron and billets for making those rebars and it is willing to pay a high price to secure these raw materials. No wonder prices are already climbing over $450/t CNF whereas Japan’s offers to Korea are still hovering at $420/t CFR.

4) Yen’s volatility keeps market participants uncertain: The Japanese yen was one of the most volatile currencies last year. It had weakened past 150 to the dollar around October 2022 – a psychological level not seen since August 1990. Currency fluctuations had kept market participants wary and had led to a demand drop over June-December, 2022, which got reflected in the prices. Japanese H2 FOB prices hovered in the range of $309-376/t during this period but it did not mind because of its high domestic demand.

Outlook

Turkiye and Japan are both heavyweight influencers in the ferrous scrap space and may have differing reasons for setting their prices. However, looking at the short-to-medium term, SteelMint expects the price parity to narrow down as Turkiye would raise its import prices to meet its pressing reconstruction needs. On the other hand, after a protracted period of depressed export offers, Japan may aggressively scout the export market with higher offers.

Leave a Reply