- Export interest revives in longs after extended silence

- Interim hike in flats on cards amid demand support

- Chinese Lunar holidays may keep prices range-bound

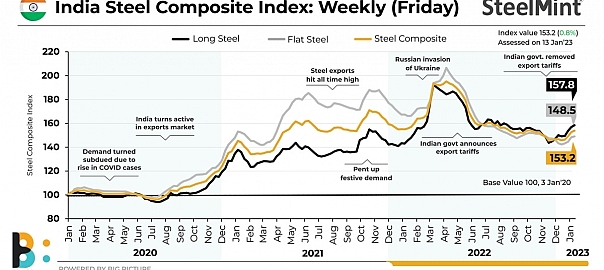

Morning Brief: The India Steel Composite Index sustained its upward trend for the last three weeks in a row to close on 13 January, 2023 at 153.20 points (152.10 points in the previous week), although this was a marginal 0.8% w-o-w rise. The flats index too rose a negligible 0.53% to 148.570 (147.70) points. Longs increased almost 1% to 157.80 (156.20) points w-o-w.

The index is also at a three-and-a-half month high since the current level was last observed on 30 September, 2022 at 153.10 points.

Factors boosting the index

Longs see heightened activity

1. Export interest revives: The longs, especially the semis (billets) segment, saw some activity of late after a protracted silence. A primary mill floated a tender for billets after a long gap and received active participation although no deal was closed. This was because the bids fell short of the mill’s expectations. But the tender indicated that overseas interest is reviving.

2. Uptick in global billets prices: Billets prices from Iran, the second-largest billets exporter after Russia, rose by $30/t in a recent deal. Thus, this global uptick in prices supported the increase in domestic prices.

3. Demand from project segment robust: Demand from the infrastructure project developers is good. Longs prices have already increased to INR 59,000-60,000/t ($726-738/t) and projects are accepting these levels, as they have deadlines to meet before the financial year closes on 31 March. Sensing that the market will likely absorb another hike, a leading tier-1 mill raised prices of rebar again by around INR 1,500/t ($18/t). This will set the tone for another round of hike in rebar rates from other primary mills too.

Flats see bullish trend

1. Flats export offers rise: The SteelMint export index rose $15/t this week, hitting a six-month high at $615/t FOB as mills increased offers to $650-660/t CFR UAE and $630-640/t CFR Vietnam. Mills also raised HRC export offers to Europe by about $50/t to $720-725/t CFR this week amid restocking activities. These offers were hovering around $660-680/t in the preceding three weeks.

Indian flat steel producers have turned aggressive in exports especially after the EU market opened up, and also buoyed by rising Chinese HRC export offers and futures.

2. Imports become unfavourable: Imported hot rolled coils (HRC) which had been a spot of bother for domestic mills, have become unfavourable with the uptick in global prices. Imported landed HRC prices are still cheaper but by a mere INR 1,000/t ($12/t) or so and the delivery time is 45-60 days which is further dissuading Indian buyers from taking position.

3. Raw material cost push: Prices of steel-making raw materials like iron ore and coking coal have risen lately, giving mills a cost push. NMDC hiked prices of lump ores by up to INR 500-600/t ($6-7/t) and fines by INR 500/t ($6/t), from 1 January.

SteelMint’s weekly Odisha iron ore fines Fe63% index rose by about INR 1,400/t ($17/t) to INR 5,100/t ($62/t) ex-mines as on 7 January, from INR 3,700/t ($45) around two months ago.

Similarly, weekly average prices of Australian-origin premium HCC coking coal rose by $52/t to $315/t CNF India on 7 January.

Outlook

Mills raised list prices of flats by up to INR 2,000/t ($24/t) in early January, which the market accepted. Encouraged, they are gearing up for an interim hike in flats, even as a hike in longs prices is already under way.

Meanwhile, China will go on its week-long Lunar New Year holidays from 22 January.

The market will fall silent and prices will remain range-bound in this period till the Chinese traders – who set price ideas — return.

The India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis: every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

SteelMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, SteelMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.

Leave a Reply