The possible change that China may reopen to Australia’s coal exports following thawing relations between the two nations may bring some notable changes in prices and supply, but there could be difference in magnitudes for different grades.

Background

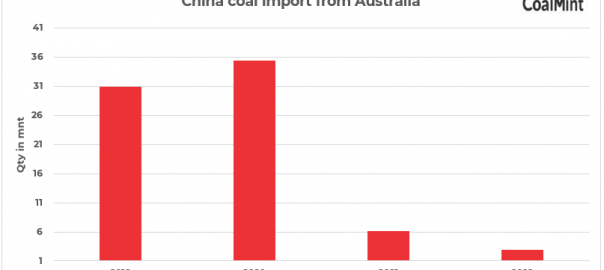

China introduced an unofficial ban on Australian coal as well as some other commodities in October 2020 in response to a series of unfriendly moves by the Morris administration. As Anthony Albanese stepped in as the new prime minister, especially after Australian foreign minister Penny Wong’s visit to Beijing in December 2022, the tension began to alleviate and finally prompted the possible lift.

According to market sources, China’s National Development and Reform Commission (NDRC) held a meeting on 3 January to discuss the lifting. Three state power groups and a major steelmaker were heard to be able to import Australian coal ahead of others.

Thermal coal

The news that China is considering a lift on Australian coal import ban brought little change in Australian thermal coal prices. On 4 January, the February contract for Newcastle thermal coal on the ICE closed at $363.7/t, up 0.85% from a day earlier.

Market sources noted the possible lift would not reshape the market in the near-term. While it is unknown when the lift will be implemented, some expected that it is not until 1 April at earliest.

Now, the bigger impact on the Newcastle futures is the weakening natural gas prices as adequate supply and warmer weather will reduce demand in Europe.

China strengthened thermal coal imports from Indonesia and Russia since it weaned off Australian coal. Meanwhile, Australia also ramped up exports to other markets to make up for the loss in the Chinese market. This is to say, the mutual dependence is low, at least for the near-term.

It was heard that orders of Australian coal have been filled well into the first quarter. And for Chinese utilities, they have launched a steady supply mechanism with domestic miners through medium- and long-term contracts. The country has added 300 million tonnes into the contracts for this year.

But no doubt that the reopening to Australian coal will bring more price discoveries, even at present, Australian coal is not competitive enough compared with Chinese domestic coal.

A source from a state utility calculated that the price of Australian 5,500 Kcal/kg NAR coal, for mid-February delivery, is around 1,150-1,170 yuan/t CFR North China, almost the same with the price cap by NDRC on the domestic thermal coal.

Australian coal’s re-entry also has a limited impact on Indonesian coal imports, as China is focusing on low-CV coal from Indonesia and high-CVs from Australia, but it is likely to have some linkage effects in terms of price.

Coking coal

There will be a major supply swing in coking coal if Australian coal is allowed to reenter China. Australian prime low-vol (PLV) hard coking coal used to be highly sought after in China, especially to blend with local high-ash, high-sulfur coals, as well as other blending coals imported from Russia and Mongolia.

The higher supply of Australian coal may greatly ease Chinese domestic coking coal prices, which have been flying high for years and placed great cost pressures on downstream users. Steelmakers and coking plants will be beneficial from inflows of Australian coal.

Good demand for Australian PLV, however, may not have much impact on the ample supply of Mongolian and Russian coals, which should continue to flow into China at stable or higher quantities.

Due to China’s rising demand for PLV, the price spread between MLV and PLV is likely to widen.

PCI

But prices for pulverized coal injection (PCI) material may not be impacted significantly. This is mainly because there is sufficient domestic supply and Chinese steelmakers tend to stick to domestic products.

Note: This article has been exchanged under the article exchange agreement between CoalMint and Sxcoal.

Leave a Reply