- Ebitda of top four mills to rise by 5-10% y-o-y in Q1

- Improvement in realisation offset by higher coking coal costs

Data Deep Dive: Indian steel mills are projected to further improve profitability in the June quarter (Q1FY27), building on a strong performance in the March quarter (Q4FY26), as higher steel realisations more than offset the impact of elevated coking coal costs.

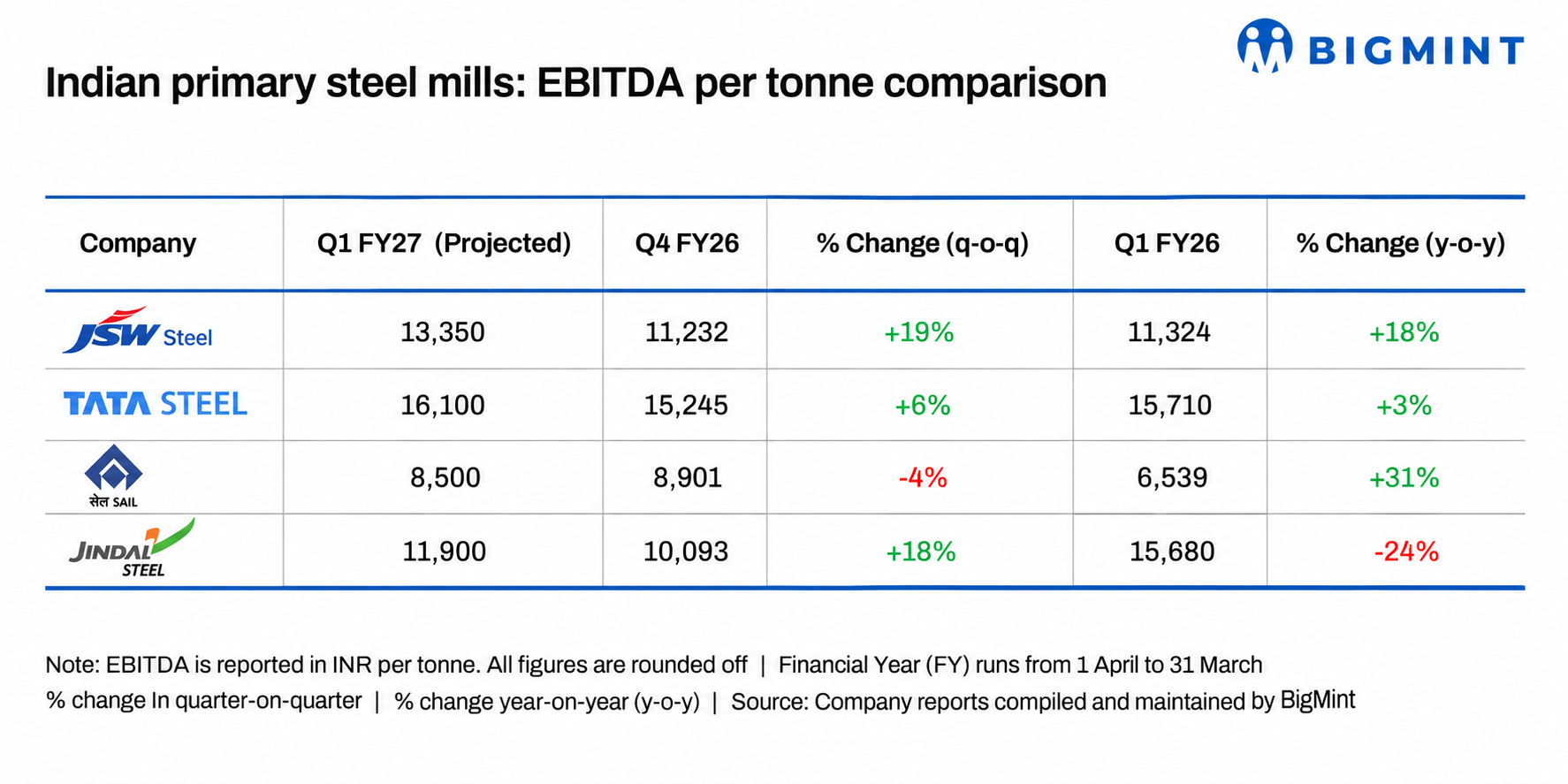

Aggregate Earnings Before Interest, Taxes, Depreciation, and Amortization (Ebitda) per tonne for the four major mills is estimated at between INR 12,313-12,979/t, up 5-11% sequentially and by a similar 5-10% on a y-o-y basis, although the extent of improvement varies across companies.

This follows a robust Q4FY26, when aggregate Ebitda per tonne had increased 20% q-o-q and 34% y-o-y.

The improvement has been driven primarily by stronger flat steel prices amid healthy domestic demand. Finished steel consumption grew 8.7% y-o-y during April-May 2026, according to provisional Joint Plant Committee (JPC) data, supported by infrastructure and construction activity. Average hot rolled coil (HRC) prices (2.5-8 mm, IS2062, Gr-E250) rose 8% sequentially and 13% y-o-y to INR 58,577/t ex-Mumbai during the quarter.

Rebar prices (BF route) eased 2% sequentially to INR 56,731/t ex-Mumbai as construction activity moderated ahead of the monsoon, although they remained 2% higher than a year earlier.

Part of the increase in domestic demand was met through higher imports, which rose 45% y-o-y during April-May, while exports increased at a slower 27%, increasing import penetration in the domestic market and emerging as a growing concern for steel producers.

The improvement in steel realisations was partly offset by higher raw material costs. Premium hard coking coal prices (0-40 mm) increased 3% sequentially to INR 24,921/t CNF Paradip, taking the y-o-y increase to 40%. Coking coal prices have been strengthening since Q3FY26, supported by lower production in China and further amplified by rupee depreciation.

Iron ore provided some relief, with Odisha Fe 62% fines (0-10 mm) prices declining 9% q-o-q to INR 5,354/t, although they remained 5% above year-earlier levels. Iron ore prices, however, are expected to firm going forward.

Company-wise performance

JSW Steel is expected to deliver the strongest earnings improvement among the major mills, with Ebitda per tonne projected to rise about 19% q-o-q and 18% y-o-y to around INR 13,350/t, the highest level in 12 quarters. The improvement follows a strong Q4FY26, when Ebitda per tonne increased 47% sequentially and 32% y-o-y.

Together with Tata Steel, JSW Steel has been among the biggest beneficiaries of the safeguard duty, which has provided significant support to HRC prices.

Tata Steel’s Ebitda per tonne is projected to increase 6% sequentially and 3% y-o-y to around INR 16,100/t, the company’s highest level in 10 quarters, supported by firmer flat steel prices.

Jindal Steel is expected to report an 18% sequential improvement in Ebitda per tonne to around INR 11,900/t, although this would still represent a 24% decline from the high base recorded a year earlier. The company’s earnings remained volatile during FY26, with Ebitda per tonne reaching a 10-quarter high of INR 15,680 in Q1 before falling to INR 8,516 in Q3 (excluding one-offs). Maintenance shutdowns during the June quarter constrained production and limited further earnings improvement.

Steel Authority of India Ltd (SAIL) is expected to remain the weakest performer among the four major producers. Ebitda per tonne is projected to decline 4% sequentially to around INR 8,500/t, although it would still represent a 31% increase y-o-y. SAIL’s Ebitda per tonne remained within the INR 5,000-7,000/t range for seven consecutive quarters before recovering to nearly INR 9,000/t in Q4FY26, with some moderation expected during Q1FY27.

The company continues to report the lowest Ebitda margin among its peers, at around 11%, largely because of higher operating expenditure.

Outlook

While Indian steel mills are expected to report another strong quarter, sustaining the current pace of earnings growth may become more challenging. Domestic steel prices have started coming under pressure, while significant capacity additions over the medium term could cap profitability despite healthy underlying demand. If domestic capacity additions outpace demand growth, greater reliance on exports will become essential to absorb the surplus and sustain profitability.

Leave a Reply