- Iranian billet absence supports regional supply balance

- Freight costs lift billet export offer levels from CIS

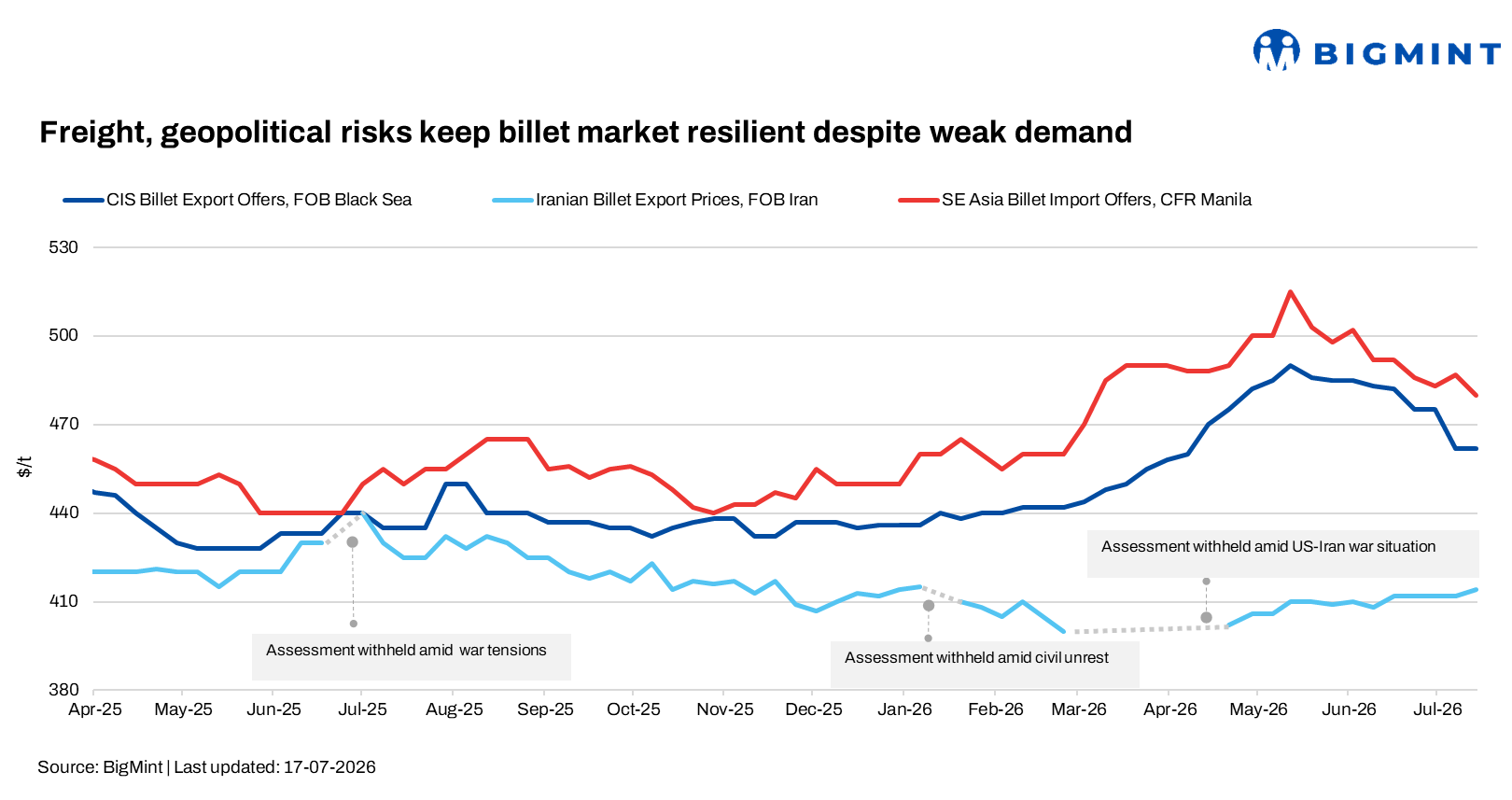

The global billet market remained mixed in the week ended 18 July as higher freight rates, rising energy costs, and geopolitical tensions supported export offers, while weak seasonal demand and cautious buying limited trading activity across Asia, the CIS, and the Middle East. Cost pressures kept suppliers firm, but subdued downstream steel demand and wide bid-offer gaps continued to restrict fresh deals.

Meanwhile, Turkiye’s imported deep-sea ferrous scrap market remained stable, with US-origin HMS 80:20 assessed at $369/t CFR. Weak rebar demand kept mills focused on need-based purchases, while imported billet was assessed at $530/t CFR Turkiye. Domestic rebar offers were heard at $565-570/t exw and export offers at $568-570/t FOB, with the scrap-to-rebar spread holding at $200-202/t, supporting steelmakers’ margins despite limited trading activity.

Asian billet market

Asian billet markets remained mixed during the week ended 18 July as higher crude oil prices and freight costs supported export offers, while weak seasonal demand across Southeast Asia continued to limit buying activity. Chinese 5SP billet offers to the Philippines increased to $480-490/t CFR Manila from $477-480/t CFR earlier, reflecting higher shipping costs following renewed Middle East tensions.

However, buyers maintained workable levels around $475/t CFR, resulting in limited transactions. Chinese billet was offered at $458-460/t FOB, while base-grade billet was heard at $440-445/t FOB or $465-475/t CFR Southeast Asia.

In China, BigMint assessed domestic billet at RMB 2,990/t ($441/t), up RMB 20/t ($3/t) w-o-w from RMB 2,970/t ($438/t). SHFE rebar futures strengthened to RMB 3,112/t ($459/t) from RMB 3,087/t ($456/t) a week earlier, supported by improving domestic sentiment, a 2% decline in mill output, maintenance shutdowns, and falling social inventories despite the summer off-season. Iron ore remained around $100/t, while softer coke prices partially offset cost support.

Although Chinese mills continued to seek export orders, overseas demand remained subdued due to the rainy season, elevated inventories, and cautious buyer sentiment across key importing markets. Over March-May, China’s billet exports increased 40-45% y-o-y to approximately 3.8-3.9 million metric tons (mnt), driven by robust shipments to Southeast Asia. Exports to Thailand and Indonesia surged above 80% to around 0.9 mnt, according to data from China Customs.

Tight regional supply, following the absence of Iranian billet exports during Q2, coupled with higher energy costs and geopolitical tensions, supported Chinese billet prices, with 3SP billet reaching a peak of $490/t FOB in mid-May. However, export prices are expected to face renewed pressure in Q3 as seasonal demand weakens, Iranian suppliers gradually return to the market, inventories remain elevated, and competition from regional exporters intensifies.

CIS billet market

The CIS billet export market remained subdued during the week as seasonal weakness, sluggish downstream steel demand, and lower scrap prices continued to weigh on trading activity. Market participants reported very limited buying interest, with no fresh export deals concluded during the week.

Russian billet offers to Turkiye were heard at $490-510/t CFR, equivalent to $460-480/t FOB Black Sea, while the prevailing FOB Black Sea offer level was around $465/t. Turkish buyers maintained bids at $480-490/t CFR (around $450-470/t FOB), keeping negotiations largely stalled. Offers to Egypt were reported at $510-515/t CFR, translating to $470-472/t FOB. Reflecting the softer market, the FOB Black Sea billet index declined to $460-462/t, down from $466-468/t earlier in the week.

In Saudi Arabia, imported billet continued to outperform domestic material on price. Indonesian billet was offered at around $530-535/t CFR, while buyer bids were $505-510/t CFR. Domestic billet prices remained stable at $580-590/t exw, maintaining a $50-70/t premium over imports. A North African producer reportedly sold around 90,000-100,000 t of billet to Saudi buyers, highlighting continued import demand despite payment-related challenges.

Meanwhile, high domestic scrap procurement prices, with HMS at SAR 2,000-2,100/t ($533-560/t), shredded at SAR 2,060-2,065/t ($549-551/t), and high grade scrap at SAR 2,070-2,075/t ($552-553/t), continued to support production costs and limited the ability of local mills to reduce billet prices. Market participants expect CIS billet exports to remain under pressure until finished steel demand improves.

Middle East billet market

The Middle East billet market remained firm during the week as higher freight rates, vessel shortages, and rising marine insurance costs supported import offers despite sluggish downstream demand. In the UAE, imported billet offers widened to $560-610/t CPT Jebel Ali from $550-600/t a week earlier. Chinese and East Asian billet was offered at $560-565/t CPT, with workable levels around $570-580/t CPT, while GCC-origin billet was heard at $615-620/t CPT, reflecting elevated logistics costs and shipping disruptions.

In Egypt, billet buying remained limited despite softer Russian offers. Standard Russian billet was offered at $510-515/t CFR, while 5SP billet was heard at $520-530/t CFR, easing billet import prices to $510-520/t CFR. Domestic rebar prices remained stable at EGP 35,000-40,000/t ($693-792/t) ex-works.

Regional sentiment remained cautious as escalating security risks in the Strait of Hormuz, including attacks on commercial vessels and the reported loss of a 43,000-t billet cargo, heightened concerns over supply chain reliability. While the immediate impact on billet availability was limited, the disruptions supported freight rates, insurance premiums, and import offers. The continued absence of competitively priced Iranian billet further tightened regional supply, while uncertainty over its return kept buyers cautious.

Leave a Reply