- India’s BF slag generation rises 6% y-o-y in FY’26 amid higher hot metal output

- Granulated BF slag used for reducing carbon emissions, lowering clinker consumption

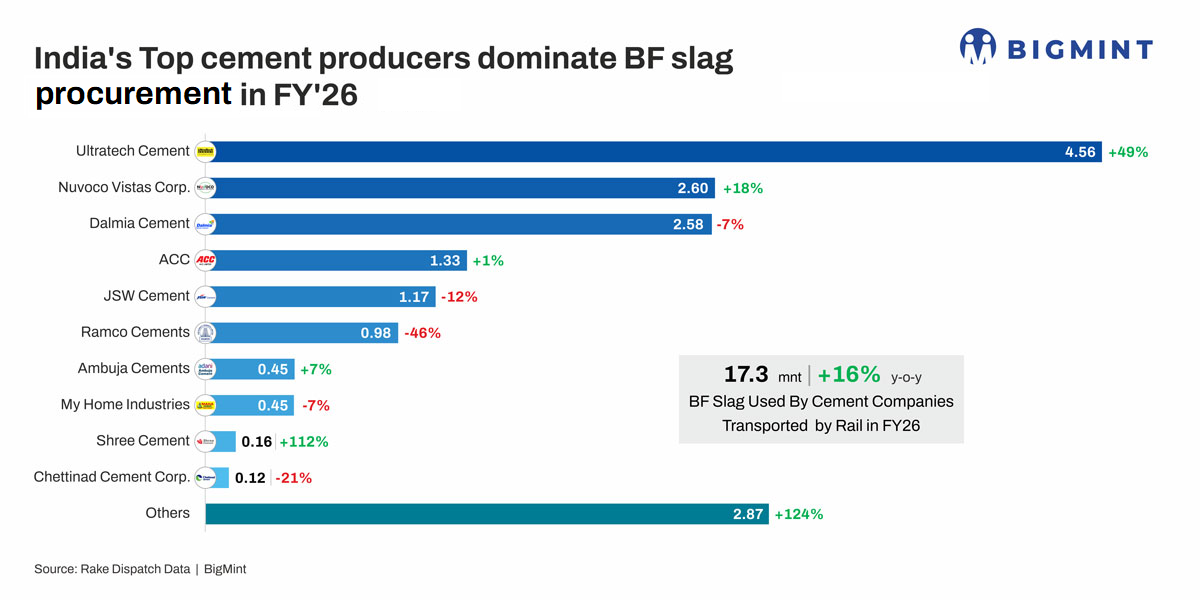

Blast furnace (BF) slag has evolved from a steelmaking by-product into one of the cement industry’s most important raw materials. According to BigMint’s rake dispatch data, capturing around 50% of total domestic rail shipments, BF-slag dispatches to cement companies by rail increased 16% y-o-y to 17.28 mnt in FY’26, compared with 14.94 mnt in FY’25.

UltraTech Cement remained the largest BF slag consignee, with rake receipts increasing 49% y-o-y to 4.56 mnt, accounting for more than one-fourth of the tracked rail movement. Nuvoco Vistas increased procurement by 18% to 2.60 mnt, while ACC maintained stable volumes at 1.33 mnt. Ambuja Cements also recorded a 7% increase to 0.45 mnt.

Among other major consumers, Dalmia Cement reduced procurement by 7% to 2.58 mnt, while Ramco Cements and JSW Cement reported declines of 46% and 12%, respectively. Shree Cement more than doubled its BF slag receipts to 0.16 mnt.

Use of BF slag in cement production

BF slag is produced during hot metal production through the blast furnace-basic oxygen furnace (BF-BOF) route, when impurities in iron ore combine with limestone flux inside the blast furnace. The molten slag is rapidly quenched with water to produce granulated blast furnace slag (GBFS), which possesses cementitious properties and is widely used in manufacturing Portland slag cement (PSC) and ground granulated blast furnace slag (GGBS).

Unlike ordinary clinker, GBFS helps reduce carbon emissions, lowers clinker consumption, and improves concrete durability, making it an important raw material as cement producers increasingly focus on low-carbon and blended cement.

India generated 35.6 mnt of BF slag in FY’26

India’s BF slag generation increased 6% y-o-y to 35.6 million tonnes (mnt) in FY’26 from 33.7 mnt, supported by higher steel production. The country’s hot metal output rose to 96.2 mnt during the year as integrated steel producers increased blast furnace utilisation and commissioned additional capacity. It should be noted that one tonne of hot metal generates around 0.37-0.38 t of BF-slag. Major BF slag suppliers include SAIL, Tata Steel, JSW Steel, AM/NS India, Jindal Steel and Power (JSP), and NMDC Steel, with slag availability directly linked to hot metal production.

Cement industry consumes most granulated BF slag

The cement industry is the largest consumer of GBFS in India, utilising almost the entire quantity of granulated slag generated by integrated steel plants. The material is primarily blended with clinker and gypsum to manufacture PSC, where slag typically accounts for 25-70% of the finished product depending on the grade. GBFS is also processed into GGBS for use in blended cement and concrete applications.

Rail dominates BF slag logistics

Efficient logistics remain critical as most integrated steel plants and cement grinding units are located in different regions. Industry estimates suggest that around 70% of BF slag is transported by rail, mainly through full-rake movements from steel plants to cement clusters, while the remaining 30% moves by road for shorter distances and last-mile connectivity. Rail continues to be the preferred mode due to its lower freight cost for bulk long-distance movement.

Outlook

India’s hot metal production is projected to reach 140 mnt by FY’30, according to BigMint data. Correspondingly, BigMint expects BF slag generation to increase to around 52 mnt, ensuring ample availability for low-carbon cement production.

India’s transition towards blended and low-carbon cement is expected to keep BF slag demand firm over the medium term. Rising steel production will improve slag availability, while ongoing capacity additions by cement manufacturers are likely to support higher consumption of PSC and GGBS. With rail continuing to dominate long-distance logistics, BF slag movement data will remain an important indicator of procurement trends and regional cement production activity.

Leave a Reply