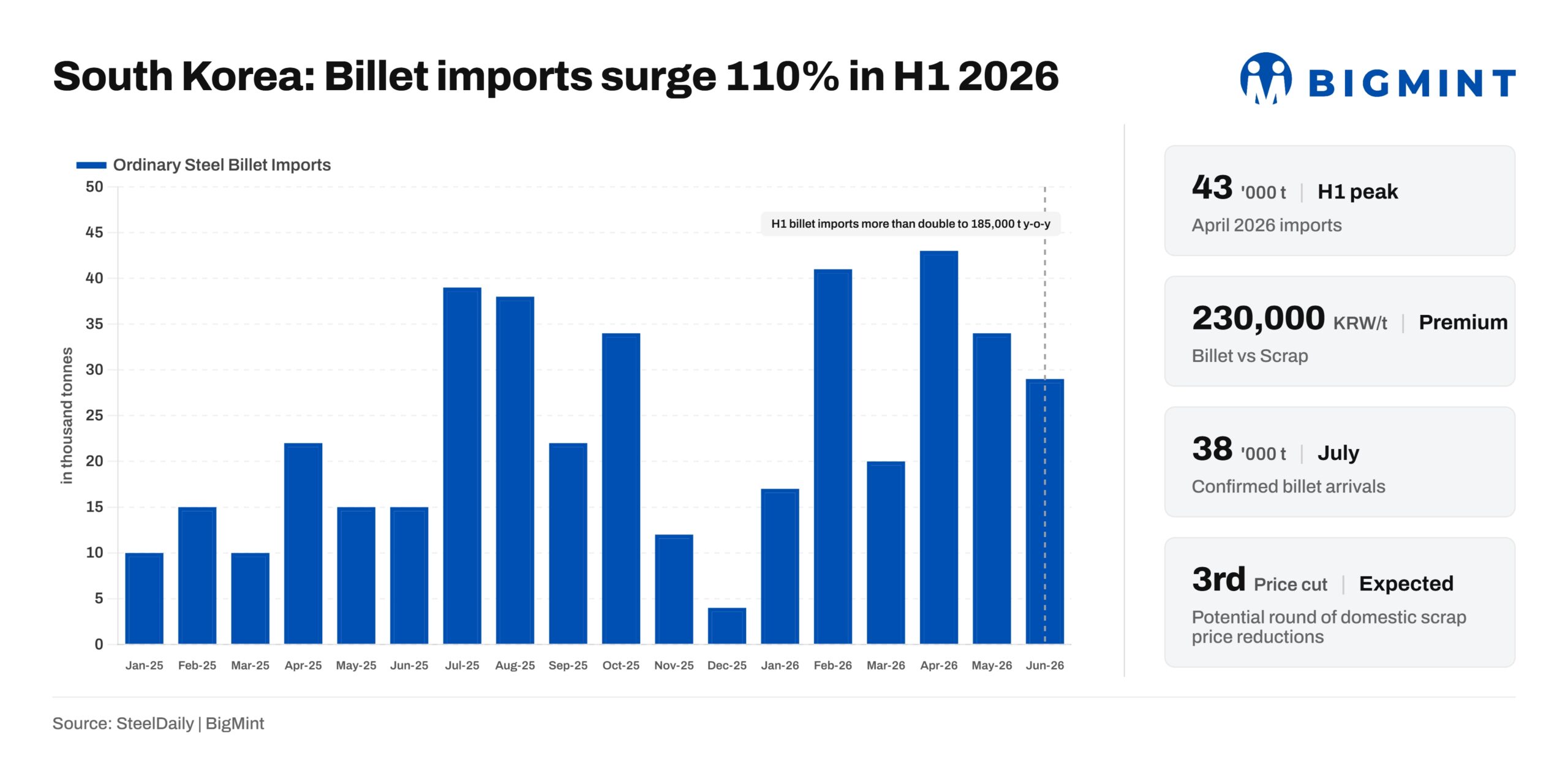

- H1 billet imports more than double to 184,750 t y-o-y

- Three confirmed July cargoes signal sustained import momentum

South Korea’s ordinary steel billet imports have accelerated sharply in 2026, highlighting a notable shift in metallics procurement by domestic electric-arc furnace (EAF) steelmakers. Cumulative billet imports reached 184,750 t during January-June 2026, up 110% from the corresponding period last year, while confirmed cargo arrivals in July indicate that import momentum remains intact. The trend could reshape domestic scrap consumption patterns, particularly as mills continue to hold comfortable scrap inventories.

Country-wise import trend

Japan remained South Korea’s dominant supplier of ordinary steel billets during the review period, continuing to account for the largest share of imports. However, import sourcing has gradually become more diversified, with Chinese-origin billets gaining a larger presence in recent half-years alongside intermittent supplies from other origins.

Import momentum extends into H2

Import momentum extends into H2

Billet imports strengthened throughout the first half of 2026, peaking at 43,000 t in April, before easing to 34,000 t in May and 29,000 t in June. Despite the moderation, imports remained well above historical monthly averages, taking first-half arrivals to nearly 185,000 t.

The strong momentum has continued into July. Following the arrival of a 15,000-t cargo at Pyeongtaek Port earlier this month, another 3,000-t billet shipment reached Masan Port on 14 July, while a further 20,000-t cargo is scheduled to arrive on 20 July. The three confirmed cargoes alone account for 38,000 t of billet imports in July, suggesting mills continue to favour imported billets as part of their raw material mix.

Scrap demand faces substitution pressure

The sustained increase of billet imports is expected to reduce dependence on domestic steel scrap, particularly as major Korean steelmakers already maintain relatively comfortable scrap inventories.

Unlike scrap, billets can be directly charged into rolling operations or EAF production, providing mills with greater operational flexibility and supply diversification. As billet arrivals increase, mills may reduce spot scrap purchases, particularly in southern Korea, where recent cargoes have been concentrated.

Industry participants believe the Yeongnam region could experience the most immediate impact, with changes in billet and scrap inflows likely to influence regional supply-demand balances. Market participants also warned that continued billet imports could trigger a third round of domestic scrap purchase price reductions, should current import volumes persist.

Economics remain closely balanced

Imported billets are not currently cheaper than domestic scrap. The average June billet import price stood at $499/t, equivalent to around KRW 765,000/t, compared with domestic Weight A scrap purchase prices of approximately KRW 530,000/t, leaving a premium of roughly KRW 230,000/t for imported billets.

Despite the cost premium, mills continue importing billets, indicating that procurement decisions are increasingly being driven by production flexibility, inventory management and raw material diversification rather than direct price competitiveness alone.

Market implications

The sharp increase in billet imports marks a structural shift in Korea’s metallics procurement strategy. If elevated import volumes continue through the third quarter, domestic scrap demand is likely to soften further, limiting procurement activity and increasing downward pressure on scrap purchase prices. Market participants will closely monitor additional billet bookings, mill inventory levels and domestic scrap price revisions to assess the pace of substitution between billets and scrap.

Note: This article has been published in accordance with a content exchange agreement between SteelDaily and BigMint.

Leave a Reply