- Coal inventory drawdown reflects strong demand, not supply stress

- India’s coal market shifting from stock accumulation to inventory optimisation

India’s domestic coal supply chain is entering a new phase characterised by a broad-based drawdown in inventories across mines, ports and thermal power plants. The trend does not signal supply stress; rather, it reflects a market where strong electricity demand is absorbing the substantial stock buffers accumulated during FY2025-26.

An analysis of Ministry of Coal, Central Electricity Authority (CEA) and BigMint port inventory data shows that inventories are simultaneously declining at every stage of the supply chain, indicating that coal is moving more rapidly from mines to consumers instead of remaining parked as inventory.

The simultaneous decline also highlights a structural shift in market behaviour. After nearly two years of inventory accumulation, driven by domestic production consistently outpacing demand, FY2026-27 has begun with consumption overtaking supply growth. Instead of building inventories, the market is now drawing down the surplus stocks accumulated over the previous year.

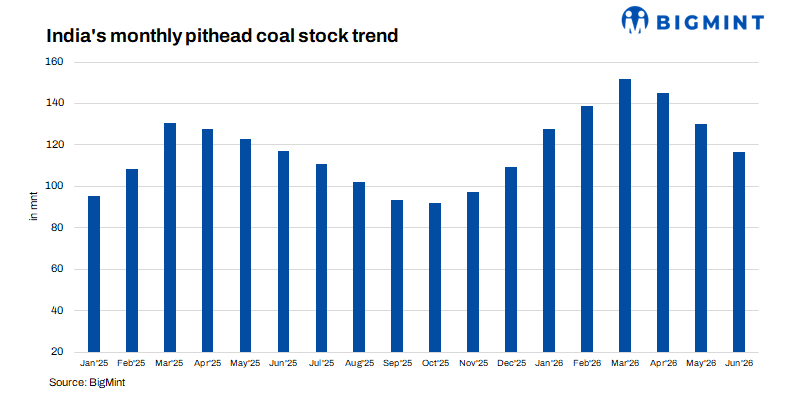

Inventory correction starts at mines

India entered FY2026-27 with an unprecedented 151.96 million tonnes (mnt) of pit-head coal inventory as on 31 March. However, while domestic production has remained close to record levels, dispatch has consistently outpaced output.

During April-June, pit-head coal inventories declined significantly as dispatches exceeded production. Opening pit-head stocks stood at 151.96 mnt, while coal production during the period reached 232.49 mnt. Against this, dispatches were higher at 268.04 mnt, reflecting robust coal offtake from consuming sectors, particularly the power sector. Consequently, the estimated closing pit-head stock fell to 116.41 mnt, indicating a drawdown of approximately 35.55 mnt over the quarter, driven by strong demand and higher evacuation levels.

The inventory balance suggests that approximately 35.5 mnt of coal was released from mine stockpiles during the first quarter.

Nearly 80% of the national inventory drawdown occurred at Coal India, whose stocks are estimated to have declined from 129.97 mnt to 101.74 mnt. This underlines Coal India’s continuing role as the principal balancing supplier to the domestic market.

Importantly, dispatch exceeded production not because mining activity weakened, but because domestic consumers required more coal than current production alone could supply. The industry therefore relied on inventories built during the previous financial year.

Ports no longer acting as storage hubs

The same trend is becoming increasingly visible at Indian ports.

BigMint’s Week 28 assessment shows total coal inventories at major ports declined to 19.37 mnt, down 7.14% week-on-week. Non-coking coal inventories fell to 14.16 mnt, down 6.06%, while coking coal inventories declined to 5.21 mnt, a sharper 9.98% week-on-week fall.

The decline is particularly significant because ports traditionally function as the intermediate buffer between imported supply and inland consumers. Instead of accumulating imported cargoes, inventories are now moving rapidly into the domestic market.

Some of the sharpest weekly inventory declines were recorded at:

- Mundra (-34%)

- Gangavaram (-28%)

- Karaikal (-22%)

- Pipavav (-22%)

- Haldia (-18%)

- Krishnapatnam (-16%)

- Dhamra (-11%)

Only a few ports, notably Paradip and Kandla, recorded inventory increases, largely reflecting fresh vessel arrivals rather than a broad-based build-up in stocks.

The simultaneous reduction across several major import terminals suggests that imported coal continues to find ready buyers despite comfortable domestic coal availability.

Power plants consuming coal as quickly as it arrives

The third component of the inventory story lies at India’s thermal power plants.

CEA data shows thermal power plant coal inventories have steadily declined from approximately 59.3 mnt at the end of March to 42.7 mnt by 11 July, a reduction of nearly 16.6 mnt.

Unlike previous episodes of declining power plant inventories, this drawdown has not been accompanied by supply disruptions. Instead, it reflects sustained coal consumption amid elevated electricity demand.

At the same time, the number of generating stations with critical coal inventories declined modestly from 32 plants on 30 June to 28 plants on 11 July, indicating that coal availability across the power sector remains broadly comfortable even though aggregate inventories have fallen.

Three inventories, one market signal

Viewed independently, declining pit-head stocks, lower port inventories and falling power plant coal stocks might suggest emerging supply tightness.

Viewed together, however, they tell a very different story. Coal is no longer accumulating at any point in the supply chain.

Instead:

- Mine inventories are being converted into dispatch.

- Imported coal is moving quickly through ports to end-users.

- Utilities are consuming coal almost as rapidly as it is being delivered.

This represents a coal supply chain operating at significantly higher throughput rather than one experiencing shortages.

The inventory accumulated during FY2025-26 is now flowing efficiently through the system instead of remaining locked in storage.

Demand overtakes supply growth

Several market developments have converged to produce this inventory correction.

Electricity demand has remained exceptionally strong despite the arrival of the southwest monsoon. India’s peak electricity demand exceeded 264 GW during June, while July demand has continued to remain substantially above corresponding levels last year.

Coal-fired generation therefore continues to shoulder the bulk of the country’s electricity requirements.

Meanwhile, domestic production growth has moderated after several years of rapid expansion. Coal India continues to produce around 56-57 mnt per month, close to record levels, but production has broadly plateaued while dispatch has consistently remained above 64 mnt per month.

The result is a market that is increasingly relying on inventories accumulated over the previous year rather than incremental production growth.

The inventory drawdown is a sign of market normalisation

The broad-based decline across pit-heads, ports and power plants should not be interpreted as evidence of tightening coal availability.

Instead, it reflects the normalisation of inventories from historically elevated levels. Even after the recent drawdown:

- Pit-head inventories remain above 116 mnt.

- Thermal power plants continue to hold more than 42 mnt of coal.

- Major ports still have close to 19 mnt of coal available.

Collectively, these inventories continue to provide a substantial operational buffer for India’s power and industrial sectors.

Outlook

The trajectory of domestic coal inventories over the remainder of the monsoon will depend on the balance between production, dispatch and electricity demand.

If mining operations improve following the initial monsoon disruption, production growth could stabilise inventories during the second quarter. However, should electricity demand continue to exceed seasonal expectations, dispatch is likely to remain ahead of production, resulting in a further gradual reduction in inventories

The market therefore appears to be transitioning from a phase of inventory accumulation to one of inventory optimisation, where stockpiles are being utilised more efficiently to meet strong domestic demand.

The most important takeaway is that India is not running out of coal — it is running down excess coal.

For the first time in several quarters, inventories are declining simultaneously at pit-heads, ports and thermal power plants, demonstrating that coal accumulated during FY2025-26 is now being converted into electricity generation and industrial production.

This is a hallmark of a mature and well-functioning supply chain. As long as dispatch remains robust, critical power plant inventories remain contained, and production continues near current levels, the ongoing inventory correction should be viewed as a sign of efficient market functioning rather than emerging supply stress.

In the coming months, the most important indicator will not be inventory levels alone, but whether production is able to replenish stocks at the same pace that India’s growing economy continues to consume them.

Leave a Reply