- SHFE inventories decline on stronger grid demand, lower imports

- US inventories surge as tariff arbitrage drives copper inflows

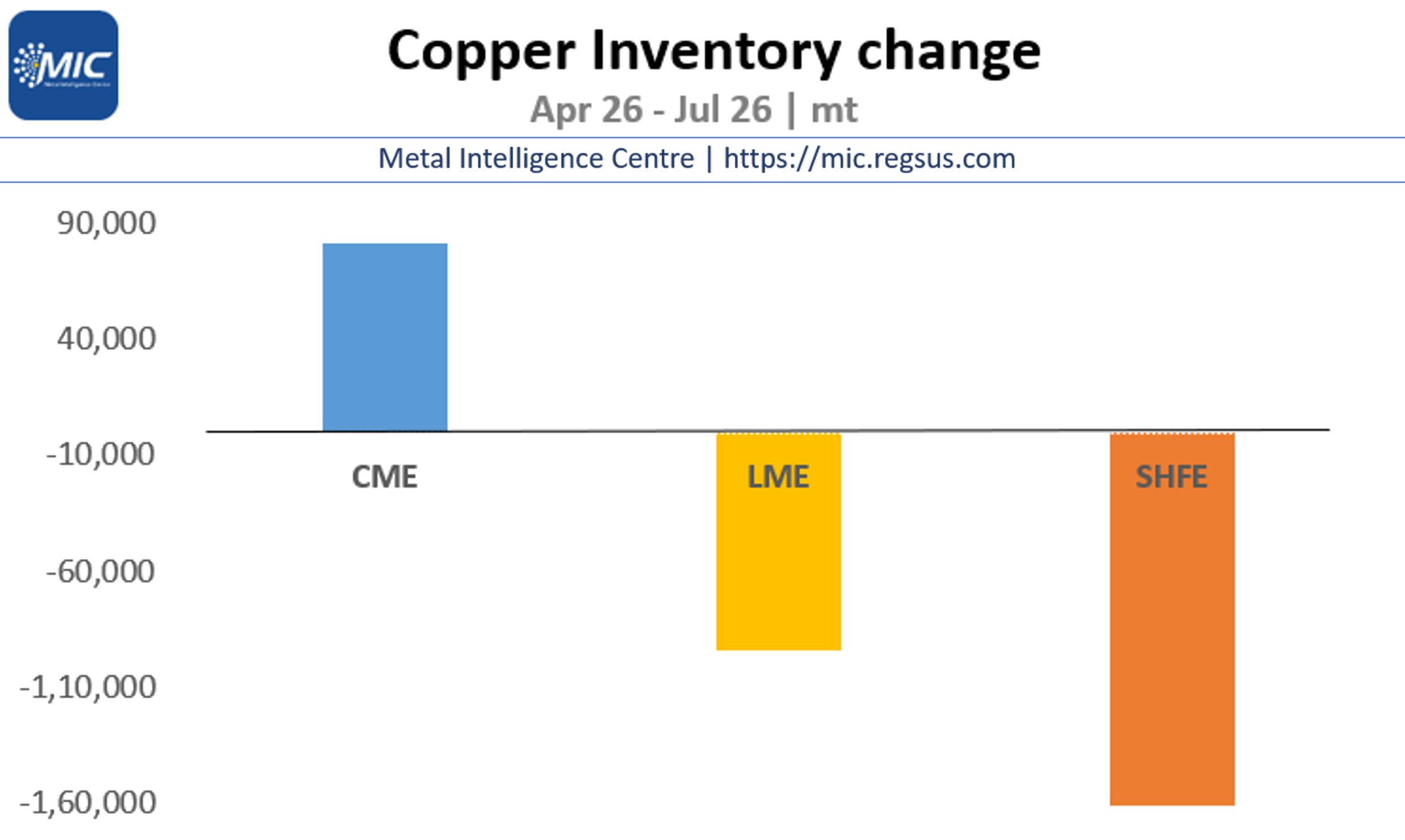

Metal Intelligence Centre: Over the last three months, copper inventories have shown a lopsided development. While financial gains raised stocks in the Chicago Mercantile Exchange (CME) by 81,709 tonnes (t) (15%), stocks in the London Metal Exchange (LME) declined by 93,950 t (24%). More importantly, growing consumption led to a 166,213 t (62%) decline in SHFE inventories.

The latest CME warehouse data shows that copper inventories have climbed to 613,741 t, making them 1.5 times larger than the combined inventories of the LME and SHFE. To put it differently, the US, which accounts for around 8% of global copper consumption, holds around 60% of global reported inventories.

SHFE inventory declines

Seasonally, SHFE stocks fall after the Lunar holidays. However, this year’s decline was exacerbated by a late surge in China’s power grid investment. Chinese reports suggest that the country boosted grid investment by 49% this year, while other sectors, such as electric vehicles, durable goods, and construction, contracted. Strong Chinese demand is reflected in the Yangshan copper premium, which rose to $80-90/t last week, the highest since June 2025.

At the same time, supplies slowed in China. The country’s copper imports declined by 7%, while output growth slowed to 5%. As grid investments picked up, consumers were forced to draw more metal from domestic warehouses.

US arbitrage drives LME inventory withdrawals

The decline in LME inventories has a different explanation.

CME prices, set by US consumers and investors, have been trading at a premium to LME prices for financial reasons, such as the possibility of US tariffs and hopes of an AI-linked demand boom. The gap hovered at $300-600/t above LME prices in recent months and provided enough incentive for traders to move copper from LME to CME warehouses.

The combination of the two — Chinese demand and US arbitrage — has helped increase requests for the withdrawal of metal inventories from LME warehouses in recent weeks. With 43% of total stocks on the withdrawal list, LME’s available inventories declined below 200,000 t this week.

The piling up of a record volume of inventories in US warehouses, far above consumption needs, points to a lopsided distribution of inventories, driven by speculation rather than real demand. Despite the recent dip, the current level of inventories in the LME and SHFE is above that of the same period in the last two years. However, any further drawdown may lead to shortages outside the US, thereby tightening premiums and lifting prices.

Note: This article has been published as part of a content partnership between Metallic Intelligence Centre and BigMint.

Leave a Reply