- EU buying sentiment improves gradually as quota clarity emerges

- Hormuz uncertainty continue to weigh on Middle East trade flows

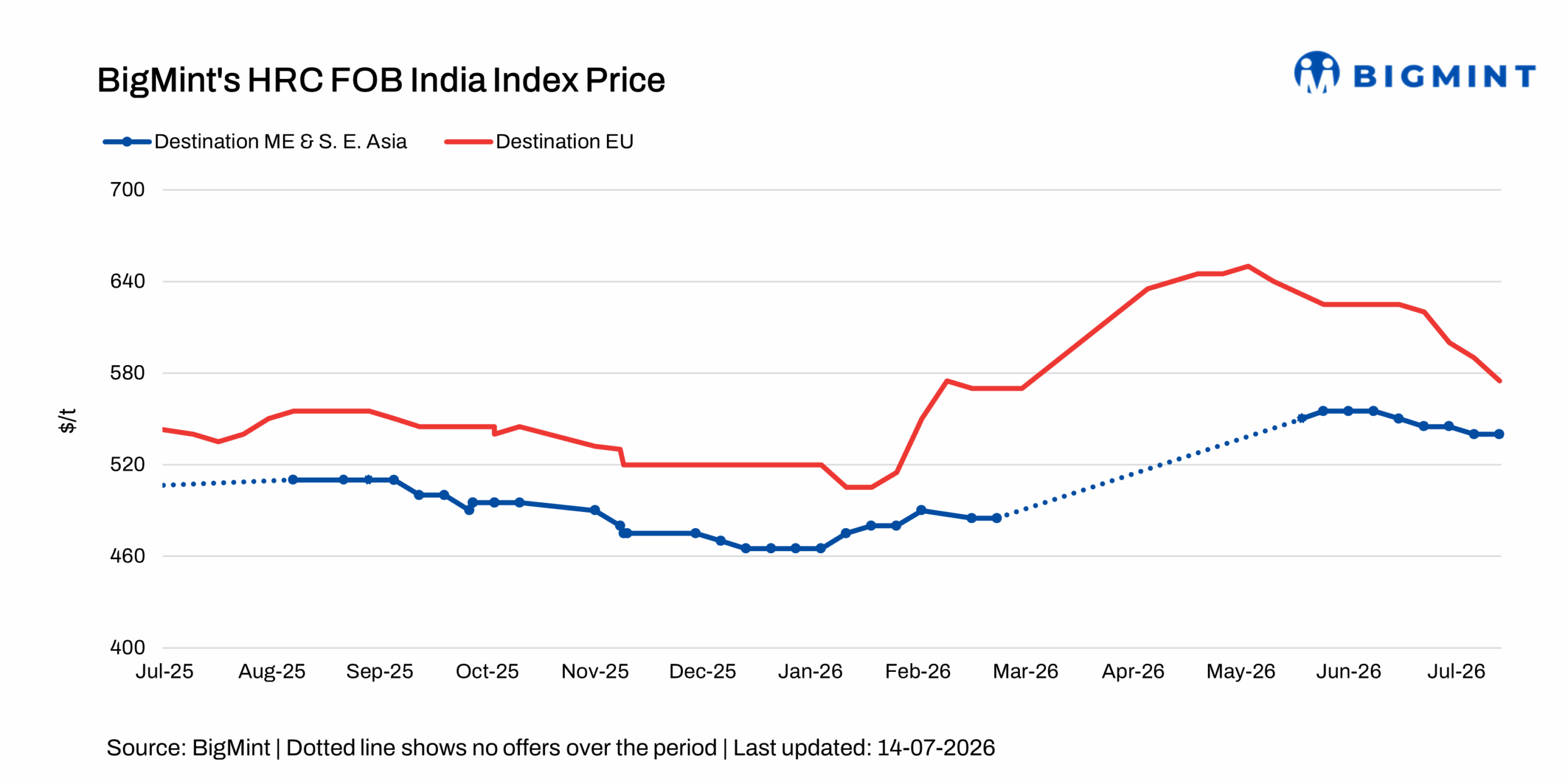

Indian HRC export activity showed mixed regional trends during the assessment week ended 14 July. Buying sentiment in the EU improved gradually as greater clarity emerged over the revised country-wise quota framework. In contrast, renewed uncertainty surrounding the Strait of Hormuz continued to weigh on trade flows in the Middle East, while weak downstream demand and elevated inventory levels kept buying activity subdued in Vietnam.

HRC export offers to the EU decline w-o-w: Indian HRC export offers to the EU declined by $15/t w-o-w to around $575/t FOB, compared with $590/t a week earlier. Moreover, a booking of around 20,000 t was reportedly concluded at similar levels for August 2026 shipments.

An EU-based source said, “Although trading activity has started to improve gradually, market sentiment remains mixed as some buyers are still assessing the available quota allocations under the revised quota system, while others have begun resuming purchases. Overall market activity is expected to strengthen from August onward as participants become more familiar with the new framework.”

Meanwhile, ArcelorMittal reportedly increased its HRC prices by around EUR 50/t ($57/t) to EUR 770/t ($880/t) on a delivered basis, likely reflecting tighter import availability under the revised quota framework and reduced import competitiveness amid CBAM-related cost pressures.

HRC export offers to the Middle East and Southeast Asia show mixed trends w-o-w: Indian HRC export index for the Middle East and Southeast Asia remained stable w-o-w at around $540/t FOB, as steady offers to the Middle East offset lower export offers to Vietnam.

Indian HRC export offers to the Middle East remained unchanged w-o-w at around $545/t FOB, with freight to Jeddah estimated at approximately $60/t. Chinese HRC export offers to the region also remained stable w-o-w at around $560/t CFR Jeddah.

A UAE-based source said, “Tensions around the Strait of Hormuz have escalated again over the past few days, making the market increasingly complicated and uncertain. Participants continue to closely monitor the situation, as sentiment remains closely tied to developments in the Strait of Hormuz. Until the situation is resolved, uncertainty is likely to continue weighing on trade flows, shipping activity, and overall market sentiment.”

In contrast, Indian HRC export offers to Vietnam declined by $10/t w-o-w to around $525/t CFR Ho Chi Minh City, from $535/t a week earlier, as weak downstream demand and ample inventories continued to weigh on buying sentiment across the region.

Outlook

Indian HRC export activity is expected to show mixed regional trends in the coming weeks, with gradual improvement likely in the EU as buyers gain clarity on country-wise quota allocations under the revised framework and resume purchasing activity.

However, Middle East trade flows may remain constrained as Hormuz-related uncertainties continue to disrupt shipping operations and weigh on buyer sentiment. Meanwhile, Indian HRC exports to Vietnam are expected to remain under pressure, as weak downstream demand and elevated inventory levels continue to limit immediate restocking activity.

Leave a Reply