- Chinese utilities delay bulk purchases amid cautious sentiment

- Indonesian prices dip as weak demand offsets tight supply

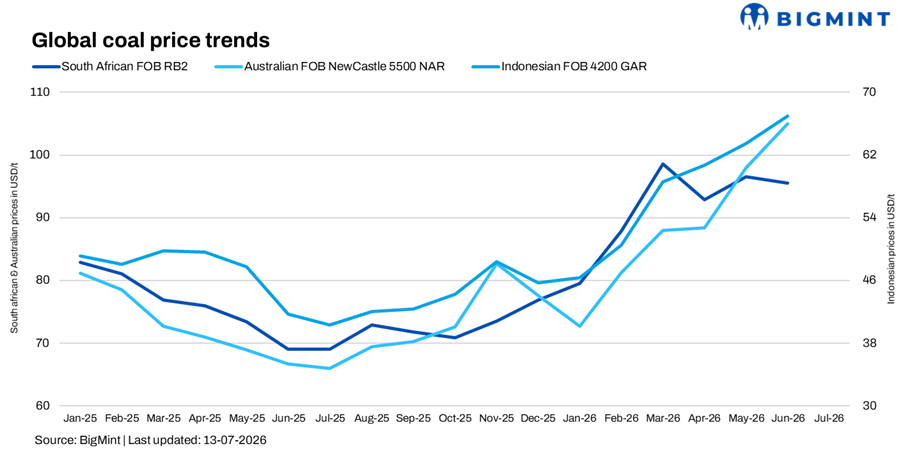

Asian seaborne thermal coal prices remained under pressure during the week ended 10 July 2026 as comfortable inventories, declining Chinese domestic coal prices, and limited Indian demand reduced buyers’ urgency. Indonesian low- and mid-calorific value coal recorded the sharpest decline, while Australian high-CV prices showed tentative signs of stabilisation after recent weakness.

Although summer power demand was beginning to improve in parts of China, utilities remained cautious and floated numerous tenders without committing to substantial volumes. In India, the monsoon, ample domestic coal availability, and rising port inventories continued to restrict fresh import bookings.

China’s domestic decline weighs on imports

Chinese domestic coal prices extended their decline during the week as utilities continued procuring cautiously despite improving seasonal power demand.

Qinhuangdao (QHD) FOB 5,000 kcal/kg NAR declined by $3.53/t w-o-w to $103.75/t, while 5,500 kcal/kg NAR fell by $3.25/t to $117.37/t and 6,000 kcal/kg NAR eased by $3.23/t to $131/t. Chinese utilities continued issuing tenders across multiple calorific grades, but confirmed awards remained limited, indicating buyers were still testing lower prices rather than rebuilding inventories. A reported Russian 5,500 kcal/kg NAR cargo traded at $99/t CFR South China, although the broader market assessment remained around $108.50/t CFR, suggesting the transaction was cargo-specific rather than representative of the wider market.

Australian Newcastle market seeks stability

Australian Newcastle thermal coal prices showed signs of stabilising after the sharp correction witnessed over recent weeks, although buying interest remained subdued.

For 6,000 kcal/kg NAR, bids improved to $125.00-130.25/t from $115.00-129.00/t a week earlier, while offers ranged between $127.00-132.75/t compared with $127.50-131.25/t previously. No confirmed trades were reported during the week.

Meanwhile, 5,500 kcal/kg NAR bids were heard at $92.00/t against offers of $94.00-95.50/t, with no confirmed trades after unconfirmed deals at $90.75-91.00/t in the previous week.

Firmer September offers reflected expectations of improved market conditions later in Q3, although demand remained subdued as South Korean utilities were adequately covered and Chinese buyers continued opportunistic procurement.

Indonesian coal records steeper correction

Indonesian thermal coal remained under pressure as subdued buying from both China and India outweighed emerging supply-side concerns. According to BigMint’s weekly FOB assessments, 5,000 GAR declined by $1.49/t w-o-w to $82.61/t, 4,200 GAR fell by $1.32/t to $63.16/t, while 3,800 GAR eased by $1.06/t to $52.24/t.

Availability of premium Indonesian cargoes remained relatively tight due to Indonesia’s Domestic Market Obligation (DMO), particularly for 3,400 GAR and 5,000 GAR coal. However, weak seaborne demand continued to outweigh supply constraints, keeping prices under pressure. Market participants also awaited clarity on Indonesia’s revised 2026 production quotas, which could influence export availability later this year.

Indian portside prices decline as domestic coal remains competitive

Indian portside Indonesian coal prices softened as buyers restricted purchases to immediate requirements. According to BigMint’s assessments, 5,000 GAR coal declined by INR 400/t w-o-w to INR 10,550/t ex-Kandla and INR 10,450/t ex-Vizag. 4,200 GAR coal fell by INR 150/t to INR 8,900/t at Kandla and INR 8,800/t at Vizag, while 3,400 GAR eased by INR 100/t to INR 6,850/t ex-Navlakhi.

South African coal prices also weakened amid negligible enquiries from sponge iron producers. BigMint assessed RB2 (5,500 NAR) at INR 10,450/t ex-Paradip and INR 10,250/t ex-Vizag, while RB3 (4,800 NAR) declined to INR 8,850/t at both ports.

Domestic coal remained significantly more competitive, with BigMint’s 5,000 GCV assessment unchanged at INR 5,500/t and 4,500 GCV stable at INR 4,050/t. Regular Coal India supplies, comfortable inventories and subdued monsoon demand continued to discourage imported coal purchases.

India’s thermal coal inventories at major ports increased by 1.6% w-o-w to 15.07 mnt, while power plant stocks remained comfortable at around 42.7 mnt, equivalent to nearly two weeks of consumption.

Outlook

Asian thermal coal prices are expected to remain under pressure in the near term, with China’s domestic market continuing to dictate seaborne sentiment. Although improving summer power demand and modest declines in Chinese port inventories could slow the pace of the correction, utilities are expected to continue buying only on a requirement basis.

In India, comfortable domestic coal availability, healthy inventories and monsoon-related demand weakness are likely to keep import demand subdued over the coming weeks. However, constrained availability of premium Indonesian cargoes and uncertainty surrounding Indonesia’s revised production quotas could provide support to higher-calorific grades later in the third quarter if regional demand improves.

Leave a Reply