- Containerised scrap gains preference in Vietnam amid limited import quotas

- Weaker Japanese yen supports exporters’ competitive pricing

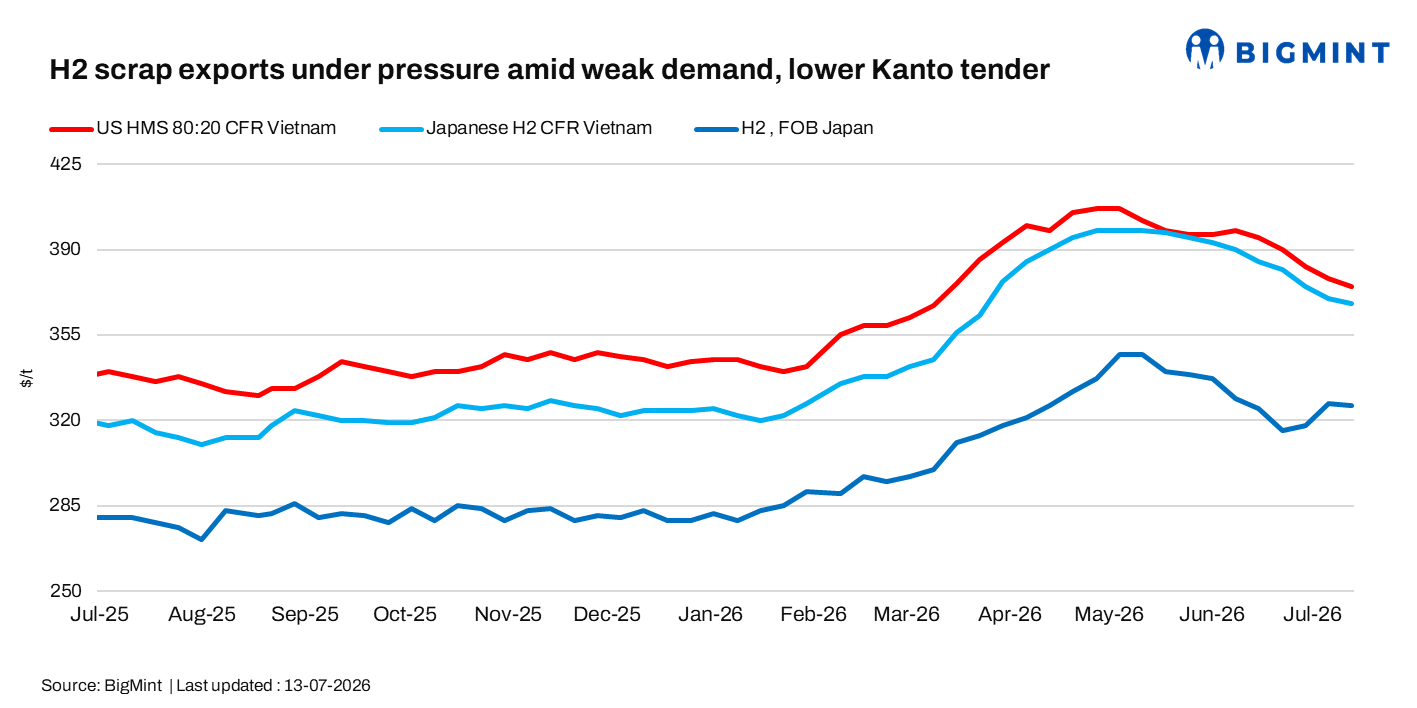

Japan’s H2 ferrous scrap export market remained subdued during the week ended 13 July as weaker downstream steel demand across Southeast Asia and cautious buying sentiment continued to weigh on trading activity. Despite the weaker yen improving export competitiveness, buyers remained cautious, delaying fresh bookings amid expectations of further price declines and ahead of the July Kanto Tetsugen tender, where the monthly price eventually fell.

Weekly assessments

- Japanese H2 scrap was at $368/t CFR Vietnam, down by $2/t w-o-w.

- Japanese H2 scrap was at JPY 52,900/t ($326/t) FOB Tokyo Bay, down by JPY 100/t ($1/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $375/t CFR Vietnam, down by 2/t w-o-w.

Japan market

H2 scrap export market remained under pressure during the week as weak overseas demand and competitive offers weighed on trading activity. Export offers to Vietnam eased to $370-375/t CFR, while buyers maintained bids below $365/t CFR, keeping a wide bid-offer gap.

Although the weaker JPY improved exporters’ competitiveness, sluggish finished steel demand across key Asian markets continued to limit buying interest. The July Kanto Tetsugen tender reinforced the bearish sentiment, with 15,000 t of H2 sold at JPY 52,508/t ($324/t) FAS, down JPY 1,998/t ($12/t) m-o-m.

Tokyo Steel cut H2 scrap purchase prices by JPY 1,000/t ($6/t) at most plants, with H2 buying levels at JPY 52,000-53,500/t. FOB Tokyo Bay eased to JPY 52,900/t, while firm domestic demand for higher-grade scrap continued to limit export availability.

Vietnam market

Imported ferrous scrap buying remained subdued as weak long steel demand and sluggish construction activity continued to limit procurement. Mills largely maintained need-based purchases and delayed fresh bookings in anticipation of further price corrections, while some buyers shifted towards containerised scrap amid limited remaining import quotas following heavy bulk purchases earlier this year.

Deep-sea scrap trading also remained subdued. US-origin HMS 80:20 bulk offers were heard around $385/t CFR, with buyers indicating workable levels near $370-372/t CFR, resulting in no reported transactions.

A Vietnamese market participant said, “Construction demand remains weak due to adverse weather, and mills are buying only for immediate requirements. Demand could improve later as producers begin securing scrap for September production.”

Leave a Reply