- Easing demand weighs on SCFI

- Carrier capacity discipline limits downside

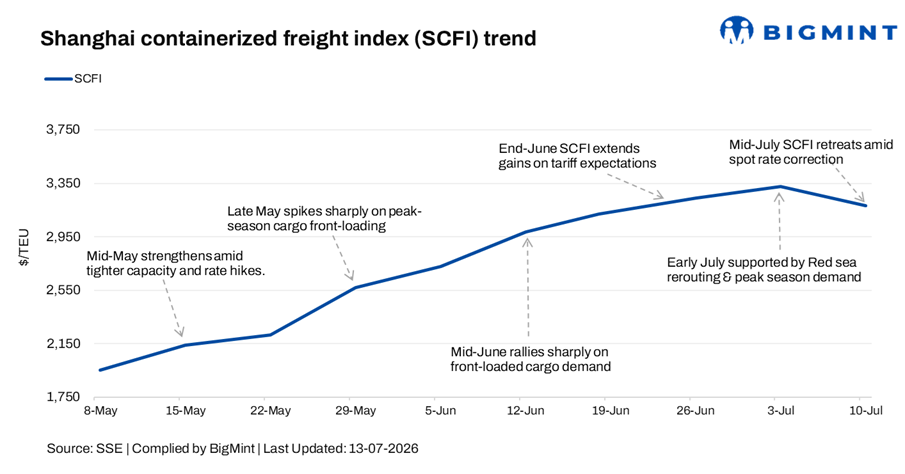

The Shanghai Containerized Freight Index (SCFI) declined 4.3% w-o-w to 3,184.82 points on 10 July 2026, from 3,326.87 points on 03 July 2026, reflecting a modest correction after the sharp rally witnessed in recent weeks.

The decline was primarily driven by lower assessed spot freight rates as earlier front-loading demand began to ease and additional vessel capacity entered the market. Nevertheless, carriers continued to implement General Rate Increases (GRIs) and peak-season surcharges (PSS), while selectively managing capacity through blank sailings and service rationalization to support freight levels and prevent a sharper correction.

Despite the decline in the benchmark index, freight market sentiment across the major east-west trade lanes remained relatively firm. Seasonal cargo demand continued to support the Asia-Europe and Asia-Mediterranean routes, while trans-Pacific trade benefited from front-loaded shipments ahead of potential U.S. tariff changes.

However, improving vessel availability and a gradual rebalancing of supply-demand conditions limited the full realization of carrier-led rate increases, resulting in a moderation of the SCFI.

Outlook

The SCFI is expected to exhibit volatility in the near term. While the recent correction indicates that the sharp gains recorded in the previous week may be losing momentum, seasonal export demand, continued front-loading of shipments ahead of potential trade policy changes, and carriers’ capacity management through selective blank sailings are likely to provide support to spot freight rates. However, improving vessel availability and softer booking activity on some routes could limit further upside.

Leave a Reply