- SECL dominates volumes; ECL focuses on premium coal

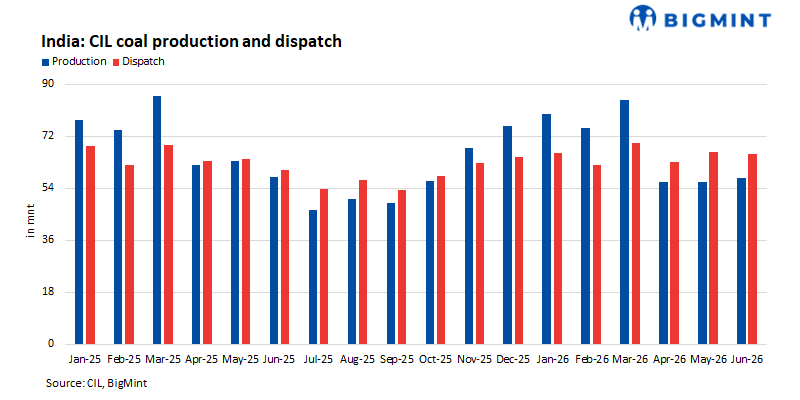

- Need-based buying likely amid comfortable domestic coal availability

Coal India subsidiaries South Eastern Coalfields Ltd (SECL) and Eastern Coalfields Ltd (ECL) have together notified 1.105 million tonnes (11.05 lakh tonnes) of coal for their upcoming e-auctions. While SECL has offered 10.30 lakh t across four major clusters, ECL has notified 74,900 t comprising premium steam coal grades from multiple underground and opencast mines.

The combined offering covers G3 to G15 grades through both road and rail modes, catering to power producers, sponge iron units and other non-regulated sector consumers.

SECL notifies 10.30 lakh t, led by Baroud G14 cluster

South Eastern Coalfields Ltd (SECL) has notified 1.03 million tonnes (mnt) of non-coking coal for its e-auction scheduled on 17 July 2026. The offering spans multiple grades across road and rail modes, with the Baroud OC G14 cluster emerging as the largest contributor.

The Baroud OC G14 cluster has notified 500,000 t, accounting for nearly half of the total auction quantity. The offering comprises 100,000 t from Baroud OC through road mode and 400,000 t via Baroud Silo in rail mode. The rail quantity will be sourced from Baroud OC, Bijari OC and Jampali OC, while the representative G14 grade has been notified at INR 930/t.

The Chhal cluster has notified 400,050 t, including 50 t through road mode from Chhal OC and 400,000 t through Chhal Rail Siding. While the road lot comprises G11 coal, the rail quantity will be supplied as G15 coal from Chhal OC. The representative grade for the cluster remains G11, with a notified price of INR 1,184/t.

The Jagannathpur OC G11 cluster has notified 60,050 t, comprising 50 t through road mode and 60,000 t through Bhatgaon AWT Rail Siding. The rail supply will be sourced from Jagannathpur OC, Ketki UG and Gayatri UG, with the representative G11 grade notified at INR 1,184/t.

The Shivani UG cluster has offered 70,000 t of G7 coal, including 10,000 t through road mode and 60,000 t via CHP Bhatgaon Rail Siding. The representative grade has been notified at INR 2,540/t.

Rail mode dominates SECL dispatch

Rail transportation accounts for 9,20,000 t, or nearly 89% of SECL’s total offering, while the remaining 1,10,100 t has been notified through road mode. The extensive rail availability is expected to facilitate procurement by power utilities and other bulk consumers across key demand centres.

ECL offering led by premium G4 coal

ECL has notified 74,900 t of steam coal for its 18 July 2026 e-auction across G3, G4, G5, G6 and W04 grades. The offering spans multiple underground and opencast mines, with G4 coal accounting for 45,000 t, or around 60% of the total notified quantity.

The 45,000 t G4 offering includes 4,000 t each from Chora 7&9 Pit UG and Bansra UG; 3,000 t each from Pandaveswar UG, Central Kajora UG, Porascole East UG and Chora 10 Pit UG; and 1,000 t each from Amritnagar UG, Ningha UG, Dhemomain Incline UG, Parbelia UG and Patmohona UG. Smaller quantities of 500 t each have been notified from Khandra UG, Bhanora West Block UG and Nimcha UG.

In addition, 4,000 t will be offered through UKA IV Bankola Line II rail siding, sourced from Shyamsundarpur UG. The grade has been notified at INR 3,557/t.

The Belbaid cluster has offered 25,000 t of G5 steam coal, including 5,000 t through road mode and 20,000 t through TOP-I (Belbaid) rail siding. The grade has been notified at INR 3,275/t.

The auction also includes 6,000 t of G3 steam coal from Central Kajora UG and Porascole (E) UG, notified at INR 3,719/t. In addition, 7,000 t of G6 coal has been offered under the Salanpur B cluster at INR 3,031/t, while the Mugma D cluster has notified 5,000 t of W04 coal at INR 2,890/t.

ECL dispatch balanced across road and rail

Unlike SECL, ECL has adopted a more balanced dispatch strategy. Road mode accounts for a significant share of the offering across the G3, G4 and G6 grades, while rail dispatch has been provided for selected G4, G5, G6 and W04 lots through UKA IV (Bankola Line II), TOP-I (Belbaid), Dalmiya Siding and MMU IIIA/PMCS, offering logistical flexibility to industrial consumers.

Market implication

The combined auction reflects two distinct procurement opportunities. SECL’s catalogue is dominated by large-volume G14 and G11 coal, primarily targeting power producers and other bulk consumers through extensive rail connectivity.

In contrast, ECL’s offering is concentrated in premium G3, G4 and G5 grades, which together account for over 75% of its notified quantity and are expected to attract demand from sponge iron, captive power and other industrial users.

With domestic coal availability remaining comfortable and monsoon conditions continuing to moderate industrial activity, bidding across both auctions is likely to remain consumption-driven. Buyers are expected to focus on delivered costs, freight advantages and immediate fuel requirements rather than aggressive inventory building.

Leave a Reply