- Muted industrial demand, cautious base metals sentiment weigh on prices

- SHFE lead edges higher; MCX futures gain on fresh buying interest

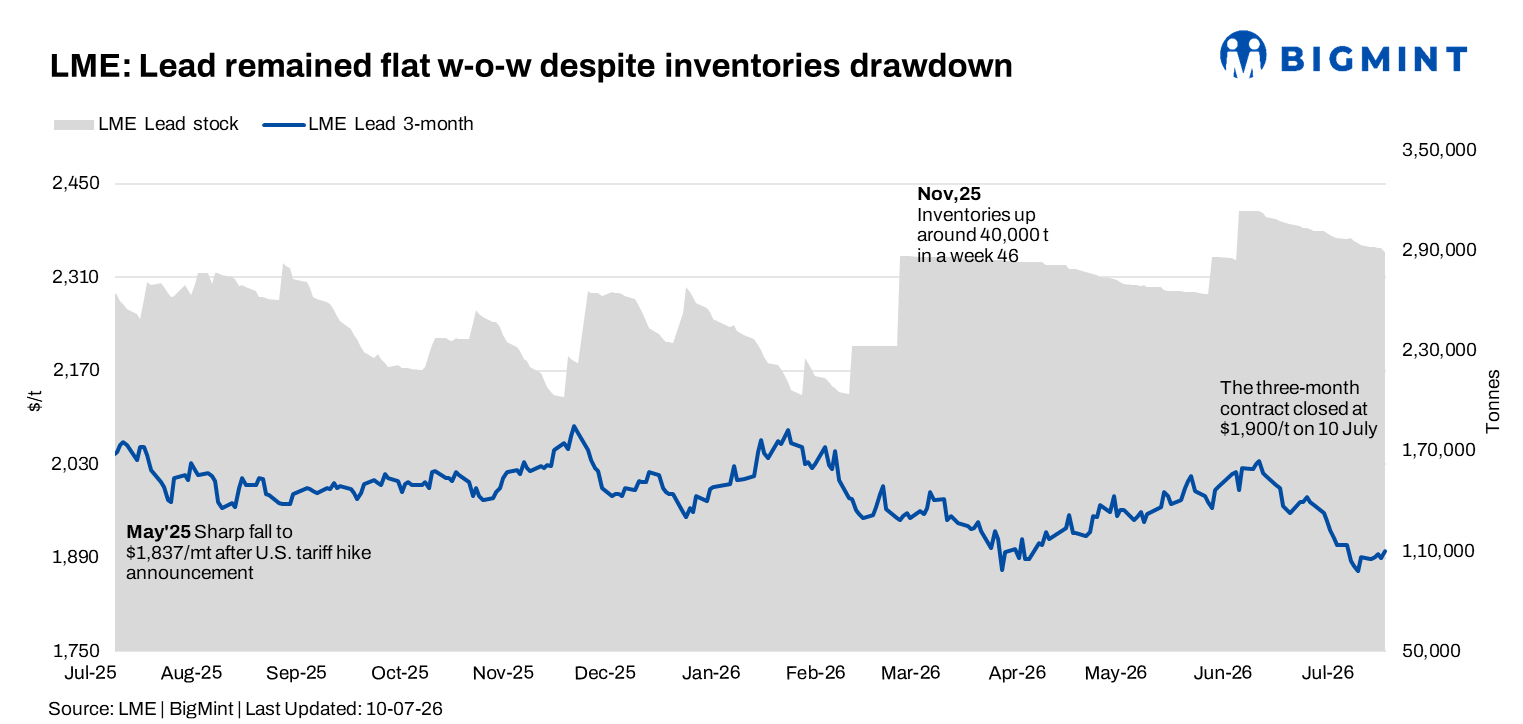

Lead prices on the London Metal Exchange (LME) remained largely range-bound during the week ended 10 July 2026, with prices continuing to trade below the psychological $1,900/t mark despite another week of declining exchange inventories. While warehouse stocks extended their downward trend, subdued industrial demand and cautious sentiment across the base metals complex limited any meaningful upside.

On a w-o-w basis, LME cash lead prices remained virtually unchanged at $1,851/t on 10 July, compared with $1,851/t on 3 July. Although prices showed resilience following the previous week’s weakness, persistent caution among market participants kept lead below the key resistance level of $1,900/t.

Price trends

LME cash lead prices opened the week at $1,852.5/t on 6 July before easing marginally to $1,849/t on 7 July. Prices recovered to $1,851/t on 8 July, slipped slightly to $1,850/t on 9 July, and closed the week at $1,851/t on 10 July, reflecting a narrow trading range throughout the reporting period.

The three-month contract displayed relatively stronger performance. Prices started the week at $1,888/t on 6 July, improved to $1,891.5/t on 7 July, climbed further to $1,895.5/t on 8 July, softened marginally to $1,890/t on 9 July, and ended the week at $1,899.5/t on 10 July, approaching the important $1,900/t level.

Despite the improvement in forward prices, the cash contract continued to trade comfortably below $1,900/t, highlighting cautious spot market sentiment and restrained buying activity.

Inventory analysis

LME lead inventories continued to decline during the reporting week, providing underlying support to market fundamentals.

Exchange stocks fell from 293,150 t on 3 July to 292,275 t on 6 July, before easing further to 292,075 t on 7 July. Inventories declined to 291,425 t on both 8 and 9 July, before falling further to 289,375 t on 10 July.

Overall, LME lead inventories declined by 3,775 t w-o-w, extending the warehouse drawdown seen in recent weeks. The continued reduction suggests steady physical outflows from exchange warehouses, although tighter inventories remained insufficient to trigger a sustained price recovery amid subdued demand conditions.

SHFE lead trends

Lead prices on the Shanghai Futures Exchange (SHFE) strengthened modestly during the week, indicating a slight improvement in domestic Chinese sentiment.

SHFE lead increased from $2,210/t on 6 July to $2,216/t on 7 July, before rising further to $2,221/t on 8 July. Prices edged down marginally to $2,217/t on 9 July, before rebounding to close the week at $2,239/t on 10 July.

The gradual recovery suggests improved downstream participation and relatively firmer sentiment in China’s domestic lead market, although gains remained moderate amid broader macroeconomic uncertainties.

MCX lead trends (6-10 July)

On the Multi Commodity Exchange (MCX), lead futures outperformed overseas benchmarks, registering steady gains throughout most of the week.

The July futures contract settled at INR 198,600/t on 6 July before easing marginally to INR 198,200/t on 7 July. Prices recovered to INR 199,050/t on 8 July, climbed further to INR 200,850/t on 9 July, and closed at INR 200,650/t on 10 July.

Open interest declined from 537 lots on 6 July to 531 lots on 7 July, before recovering to 540 lots on 9 July and ending the week at 538 lots. The rise in prices alongside relatively stable open interest suggests fresh buying interest during the week, while the marginal decline in prices and open interest on the final trading day points to limited profit booking after recent gains.

Trading volumes remained moderate as domestic consumers largely continued need-based procurement amid comfortable availability of refined lead.

Market updates

Market sentiment remained cautious during the week as LME lead prices continued to trade below the key $1,900/t threshold despite another week of declining exchange inventories. The continued inventory drawdown offered support to underlying market fundamentals, but subdued industrial demand and cautious buying interest prevented prices from establishing a stronger upward trend.

In China, SHFE lead prices posted modest gains, indicating relatively firmer domestic sentiment compared with overseas markets. Meanwhile, MCX lead futures remained resilient, supported by gradual buying interest and stable domestic demand conditions, even as global lead markets continued to consolidate.

Outlook

BigMint expects LME lead prices to remain range-bound in the near term as declining exchange inventories continue to provide underlying support, while cautious industrial demand and subdued spot market activity limit upside potential.

Immediate support is likely around $1,840-1,850/t, while resistance is expected near $1,900-1,920/t. Inventory trends, macroeconomic developments and downstream demand in China and other key consuming regions will remain the primary indicators for price direction, while Indian buyers are expected to continue following a need-based procurement strategy.

Leave a Reply