- Turkish scrap decline weighs on CIS billet prices

- Chinese domestic market outperforms weaker export markets

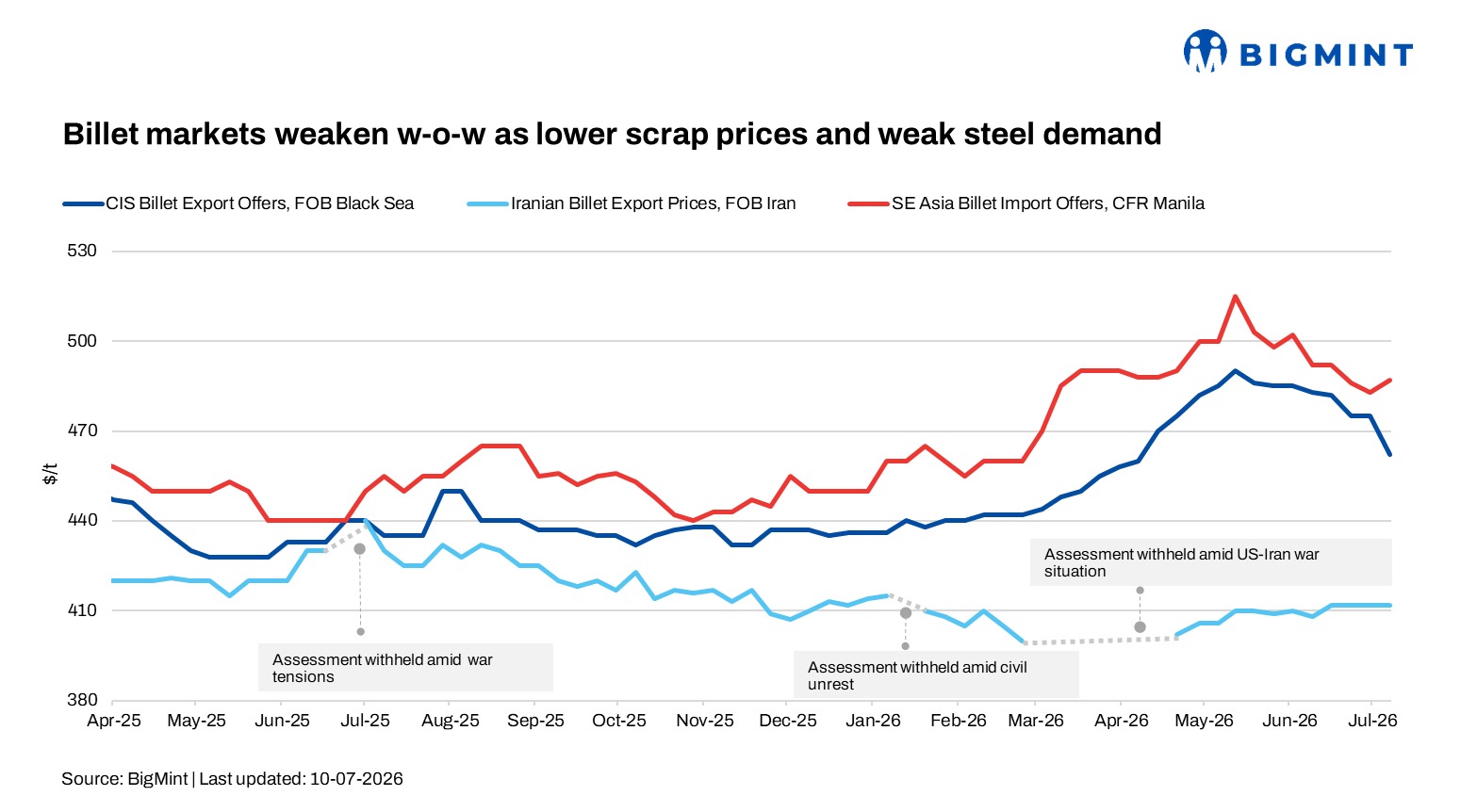

Global billet markets remained under pressure during the week ended 10 July as weak finished steel demand, softer scrap prices, and cautious mill procurement continued to weigh on trading activity across key regions. While firmer raw material costs and supply-side constraints supported China’s domestic billet market, export markets in the CIS, Asia, and the Middle East remained subdued amid sluggish buying interest, widening bid-offer gaps, and intense competition among suppliers. Most buyers restricted purchases to immediate requirements, with expectations of further price corrections continuing to dominate market sentiment.

The decline in Turkish imported scrap prices reinforced the bearish outlook for the billet market. Deep-sea HMS 80:20 scrap prices fell to around $362-370/t CFR, while rebar export offers softened to $570-575/t FOB, widening the scrap-to-rebar spread to approximately $200-205/t. Weak finished steel demand and hand-to-mouth procurement by Turkish mills continued to pressure both scrap and billet markets, with buyers remaining cautious despite improved steelmaking margins.

CIS billet market

The CIS billet market remained under pressure during the week as weak finished steel demand, lower scrap prices, and cautious buying from Turkiye continued to weigh on sentiment. Russian billet offers for late August-September shipment eased to $462-466/t FOB Black Sea, down from $472-475/t FOB a week earlier, while market participants indicated that offers could fall towards $460/t FOB if demand fails to improve.

However, a stronger Russian rouble may limit further price reductions, as mills seek to balance export sales targets with exchange rate developments before making deeper offer cuts.

In Turkiye, CIS billet offers declined to $485-495/t CFR, compared with $500-505/t CFR previously, but buyers continued targeting $470-480/t CFR, citing the recent correction in imported scrap prices. As a result, trading activity remained limited, with most buyers delaying purchases in anticipation of further price declines.

The domestic Turkish billet market also weakened, with Kardemir reducing billet prices by $10-15/t to $515-520/t exw and selling around 60,000 t within hours. Other domestic mills also lowered offers to $525-530/t exw, down from $545-550/t exw amid softer market conditions.

Notably, BigMint data shows that Turkiye’s billet imports rose over 5% y-o-y to 3.43 mnt during 5MCY’26, supported by competitively priced supplies from the CIS, China, Oman and the UAE. Billet exports also increased sharply by 95% y-o-y to 0.41 mnt. However, imports continued to far exceed exports, highlighting Turkiye’s growing reliance on imported semi-finished steel amid weak finished steel export demand and challenging conditions for domestic rerolling mills.

Asian billet market

Asian billet export markets remained subdued during the week ended 10 July as weak finished steel demand, intense regional competition, and expectations of further price declines kept buyers cautious.

China’s domestic billet market remained relatively firm, with BigMint assessing billet at RMB 2,970/t ($438/t), up RMB 30/t w-o-w, supported by stronger raw material costs and power-related supply concerns. Chinese 3SP billet export offers also increased to around $460/t FOB, while rebar export offers remained stable at $497/t FOB, although fresh export bookings were limited by weak overseas demand.

Indian billet exporters remained under pressure as monsoon-related weakness in domestic steel demand prompted mills to increasingly target overseas markets. Export offers for 3SP/4SP billets softened during the week to $445-450/t FOB, although Indian suppliers continued to face stiff competition from more competitively priced Chinese material in Southeast Asia. In Gujarat, domestic billet prices remained largely stable despite subdued local demand, supported by active export bookings. Market participants also reported fresh billet shipments to East Africa, with additional export cargoes under discussion.

Across Southeast Asia, buyers largely stayed on the sidelines awaiting lower prices. Chinese 5SP billet was offered at $484-487/t CFR Manila, while Indonesian producers maintained offers at $470-472/t FOB despite slow demand. In Saudi Arabia, Indonesian billet offers at $530-535/t CFR were considered unworkable, with buyers indicating acceptable levels below $500-510/t CFR.

Middle East billet market

Middle East billet markets remained subdued during the week as weak long steel demand, cautious buying, and geopolitical uncertainty continued to weigh on trading activity across the region. While limited billet availability supported Iranian export prices, buyers across the GCC largely stayed on the sidelines amid poor downstream demand and ample inventories.

In Iran, billet export offers remained broadly stable at $410-412/t FOB, supported by tight billet availability rather than stronger buying interest. During the week, a 30,000 t August-shipment cargo was concluded at around $415-417/t FOB by a mill in southwestern Iran. However, export activity remained constrained by renewed tensions around the Strait of Hormuz and broader geopolitical uncertainty, which continued to disrupt shipping, increase logistical risks and keep overseas buyers cautious.

In Saudi Arabia, billet imports remained slow despite softer international prices. Domestic billet prices declined sharply to around $575-585/t exw, but weak rebar demand and comfortable inventories discouraged fresh purchases. Market participants expect mills to postpone import bookings until downstream construction activity improves.

In Egypt, the government plans to issue eight new billet production licences with a combined capacity of 2.8-3 mnt to reduce import dependence and boost domestic steel production. While the move is expected to improve local billet availability, market participants warned it could create oversupply if long-steel demand remains weak. Meanwhile, rerollers continue to rely on imports despite safeguard duties due to limited domestic billet supply.

Leave a Reply