- China supply tightens as SHFE inventories fall 18% w-o-w

- Ivanhoe Mines plans to increase copper output in H2CY’26

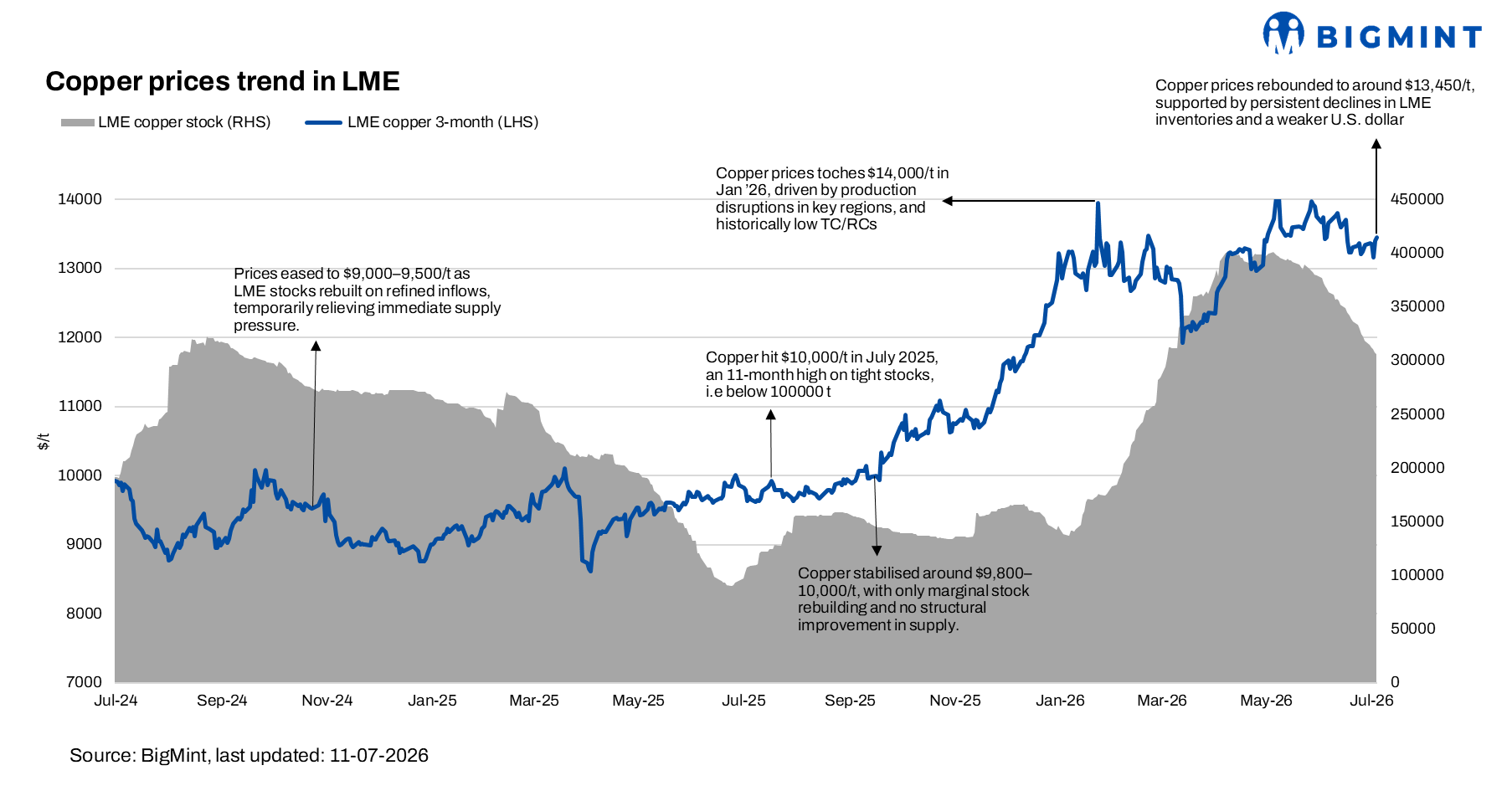

LME copper prices witnessed a volatile week, declining from around $13,370/t to nearly $13,170/t mid-week before recovering to close at approximately $13,450/t on 10 July 2026, up 0.8% w-o-w. The recovery comes amid a month-long correction, with copper returning to early-June levels after rallying to record highs and subsequently consolidating over recent weeks. The rebound was supported by continued weakness in the US dollar and persistent tightening in physical supply.

Meanwhile, LME copper inventories extended their downward trend, declining by 2.7% w-o-w, highlighting continued tightening physical availability. The sustained drawdown in exchange stocks provided underlying support to prices and helped drive the late-week recovery despite lingering macroeconomic uncertainty.

Market sentiment improved as a softer US dollar boosted buying interest, while easing geopolitical tensions reduced immediate inflation concerns. At the same time, Shanghai copper inventories fell 18.3% w-o-w, reinforcing tightening physical supply in China and supporting copper prices.

However, markets remained focused on longer-term structural shifts, with regional trade fragmentation and ongoing US tariff policies continuing to widen the pricing gap between CME and LME contracts. The growing influence of the SHFE alongside the LME also reflected an increasingly regionalised global metals market, although tight physical supply enabled copper to outperform several other industrial metals.

Global updates

Kamoa-Kakula remains on track for record copper output

The Kamoa-Kakula copper complex in the Democratic Republic of Congo produced 64,328 t of copper in Q2CY’26, taking H1 output to 124,759 t. Operator Ivanhoe Mines attributed the strong performance to improving operational efficiency and continued mine ramp-up. The miner also plans to boost copper production in H2CY’26 by lifting mining rates across the Kamoa mines (Kamoa 1 and Kansoko), as well as through destocking of copper concentrates held in inventory. As such, the company remains on track to achieve its 2026 production guidance of 520,000-580,000 t, while the Phase 3 concentrator is expected to further expand capacity.

India updates

ICA India calls for faster copper capacity expansion

India will need to add 0.5 mnt of refined copper capacity every five years to keep pace with rapidly growing demand, according to the International Copper Association (ICA) India.

The association expects copper demand to grow by around 9% in 2026, driven by infrastructure, construction, clean energy, and emerging technologies. While capacity additions by Hindalco and Kutch Copper will improve domestic supply, they are unlikely to fully bridge the gap, highlighting the need for sustained investment in smelting and refining infrastructure.

India’s copper concentrate imports surge in 4MCY’26

India’s copper concentrate imports rose 62% y-o-y to 0.60 mnt during January-April 2026, driven by the rapid expansion of domestic refining capacity, particularly the ramp-up of Adani’s Kutch Copper smelter. Despite Hindustan Copper Ltd. (HCL) increasing ore production by 6% and achieving a record 27,421 t of MIC output, domestic mining currently meets only 4% of India’s concentrate requirement.

To secure raw materials amid tightening global supply, India increased imports from Chile, its largest supplier, while HCL continues expanding mining operations under its Vision 2030 strategy to reduce long-term import dependence.

Outlook

Copper’s outlook remains constructive despite expectations of softer seasonal trading during the summer months. BigMint expects prices to regain momentum later in the year if the US Federal Reserve adopts a more dovish monetary policy, which could weaken the US dollar and support demand for industrial metals.

Continued declines in exchange inventories and persistent tightness in the global copper concentrate market are expected to provide underlying support. Meanwhile, constrained mine supply, slow project development, and limited concentrate availability are likely to keep the market structurally tight, reinforcing a positive medium- to long-term outlook for copper prices.

Leave a Reply