- Imported thermal coal prices extended decline

- PHCC weakened on softer steel demand

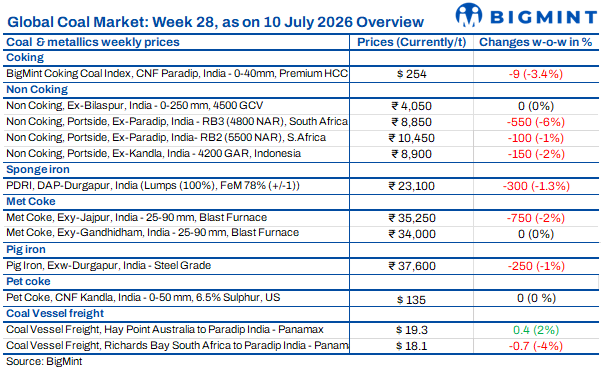

Coal buying remained restrained during the week ended 10 July’26 as weak downstream steel and sponge iron markets continued to weigh on demand. Imported thermal coal prices extended their decline, while domestic coal maintained its competitive position through ample availability and regular Coal India auctions. Policy uncertainty surrounding anti-dumping duties kept met coke trade cautious, and softer steel prices pressured coking coal values. Meanwhile, cement producers continued balancing domestic coal, imported coal and petcoke, focusing on cost optimisation rather than rebuilding inventories.

Indonesian coal prices weakened

Indian portside Indonesian thermal coal prices declined during the week ended 10 July’26 as weak buying and comfortable domestic coal availability continued to limit import demand. Prices of 5,000 GAR coal fell by INR 400/t w-o-w to INR 10,550/t at Kandla and INR 10,450/t at Vizag. Meanwhile, 4,200 GAR declined by INR 150/t to INR 8,900/t at Kandla and INR 8,800/t at Vizag, while 3,400 GAR eased by INR 100/t to INR 6,850/t at Navlakhi. Freight on the East Kalimantan-Navlakhi route dropped by $2.9/t w-o-w to $17.5/t. However, limited availability of high-GAR Indonesian cargoes continued to support premium-grade coal sentiment.

Portside coal prices fell further

South African thermal coal prices at Indian ports declined further during the week ended 10 July’26 as weak sponge iron demand, sluggish steel activity and comfortable domestic coal availability continued to weigh on imports. As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) fell by INR 100/t w-o-w to INR 10,450/t, while RB3 (4,800 NAR) dropped by INR 550/t to INR 8,850/t. At Vizag, RB2 declined by INR 150/t to INR 10,250/t and RB3 by INR 450/t to INR 8,850/t. Meanwhile, thermal coal inventories at major ports increased 1.6% w-o-w to 15.07 mnt, while PDRI DAP-Durgapur prices fell by INR 300/t to INR 23,100/t, reflecting continued weak demand.

Domestic coal prices stayed stable

Domestic coal prices remained stable during the week ended 10 July’26 as comfortable Coal India supplies and regular subsidiary auctions ensured adequate availability. BigMint assessed 5,000 GCV coal unchanged w-o-w at INR 5,500/t, while 4,500 GCV remained steady at INR 4,050/t. Competitive pricing and sufficient supply encouraged consumers to continue preferring domestic coal over imports. Coal India auctions witnessed healthy participation from cement producers, while buying from steel and sponge iron sectors remained largely requirement-based amid weak demand. The ongoing monsoon further weighed on consumption across key industries, with ample domestic availability continuing to limit imported thermal coal demand.

Met coke prices showed mixed trend

India’s domestic met coke market recorded mixed trends during the week ended 10 July’26 as uncertainty over the anti-dumping duty (ADD) on imports kept buying cautious. BF-grade coke prices in eastern India declined by INR 750/t w-o-w to INR 35,250/t ex-Jajpur, while western India remained stable at INR 34,000/t ex-Gandhidham. Foundry-grade coke also held steady at INR 36,400/t ex-Rajkot. Meanwhile, premium hard coking coal prices fell by $5/t w-o-w to $258/t CFR Paradip, while Indonesian BF-grade met coke (65/63 CSR) increased by $1/t to $319/t CFR India. Weak spot demand and policy uncertainty continued to weigh on market sentiment despite firm global coke fundamentals.

PHCC index extended decline

BigMint’s premium hard coking coal (PHCC) index declined by $9/t w-o-w to $254/t CNF Paradip on 10 July’26, pressured by lower steel prices and weaker buyer bids. Indian primary steel mills reduced July rebar list prices by INR 1,000-3,000/t m-o-m, while HRC and CRC list prices were cut by INR 1,000/t amid subdued demand, rising inventories and weak construction activity. Meanwhile, Panamax freight from Hay Point, Australia, to Paradip increased by $0.4/t w-o-w to $19.3/t, providing partial support to coking coal import costs despite the softer steel market.

Petcoke regained competitiveness

International petcoke prices declined sharply, improving fuel economics for Indian cement producers despite cautious buying during the monsoon. High-sulphur petcoke was assessed at around $135-140/t CFR India, down from nearly $160/t a few weeks earlier, while FOB US Gulf Coast prices remained at $77.75-80/t. The correction was expected to reduce cement production costs by around INR 100/t from Q3 FY’27. However, ample domestic coal availability and disciplined procurement limited immediate buying. India’s petcoke imports during H1’26 declined 37.3% y-o-y to 4.7 mnt from 7.5 mnt, reflecting a more selective purchasing strategy.

US NAPP prices stayed firm

US Northern Appalachian (NAPP) coal prices remained broadly stable despite weaker monsoon demand from cement and industrial consumers. Retail US NAPP prices in western India held at around INR 13,400-13,500/t, while ILB coal remained near INR 11,500/t. FOB Baltimore 6,900 NAR coal eased to $86.65/t, although Panamax freight to India remained elevated at around $51/t. Retail lifting at Kandla and Tuna ports declined nearly 46% over three weeks, while inventories fell over 54% to 185,247 t. Cement producers continued optimising fuel blends, supporting demand for premium US NAPP coal despite subdued procurement.

Coal freight market showed mixed trends

India’s dry bulk coal freight market recorded mixed trends during the week ended 10 July’26. Freight from Hay Point, Australia to Paradip increased by $0.4/t w-o-w to $19.3/t, supported by firm Australian coal fixtures and stronger Panamax sentiment. In contrast, the RBCT, South Africa-Paradip route declined by $0.7/t to $18.1/t due to weak cargo enquiries, while the East Kalimantan–Navlakhi Supramax route dropped by $2.9/t to $17.5/t amid subdued Indonesia-India coal activity. Meanwhile, the Baltic Dry Index (BDI) rose 9.8% w-o-w to 2,910, Brent crude increased to $76.65/bbl, while bunker prices eased by $9/t to $652/t.

Leave a Reply