- Ample scrap availability keeps buyers on the sidelines

- Weak construction demand weighs on steel market sentiment

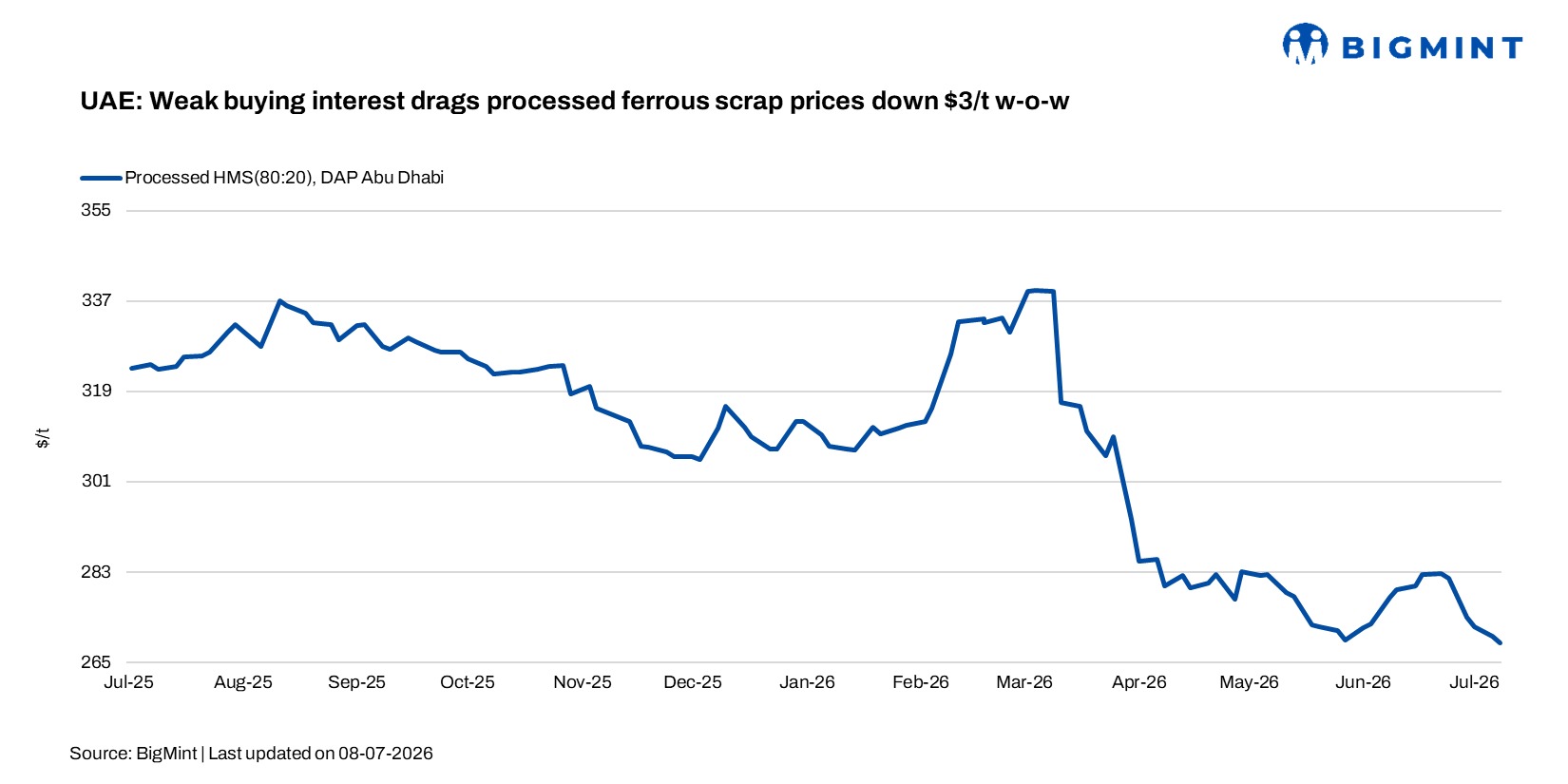

The UAE’s processed ferrous scrap market remained under pressure during the week ended 9 July, as comfortable scrap availability and subdued buying interest continued to weigh on prices. Weak downstream steel demand and expectations of further price corrections following the UAE’s export ban kept procurement activity largely need-based, with buyers showing little urgency to secure material. According to BigMint’s assessment, processed HMS (80:20) scrap was assessed at AED 988/t ($269/t) DAP Abu Dhabi, down AED 12/t ($3/t) week on week from AED 1,000/t ($272/t).

Market participants reported comfortable availability across all major scrap grades, with no immediate supply constraints. Buyers continued to procure material only against short-term production requirements, as abundant domestic availability reduced the need for forward purchases.

According to market sources, transactions during the week were largely concluded on a delivered basis within one week, with LMS trading at AED 840-860/t ($227-232/t), HMS 80:20 at AED 925-940/t ($250-254/t), processed HMS at AED 980-1,000/t ($265-270/t), and processed PNS at AED 1,040-1,060/t ($281-286/t).

Overall market sentiment remained soft, with buyers expecting additional price corrections following the recently implemented export restrictions. As material remained readily available, most consumers continued to delay purchases, anticipating more favourable buying opportunities.

A Dubai based-scrap trader said, “Supply is comfortable across all grades, and buyers are in no hurry to book material. Most expect prices to soften further over the coming weeks.”

Another yard-side participant added: “Transactions are continuing, but almost entirely on a need basis. There are no supply concerns at present, which has reduced buyers’ urgency.”

Steel market developments

The UAE’s long steel market remained relatively resilient despite seasonal weakness. Mills were largely able to achieve their targeted July sales volumes, although discounts were widely offered to stimulate demand. Traders, however, continued to face margin pressure as construction activity remained slow and downstream buying subdued.

Market participants expect construction demand to remain weak until September, raising concerns over the sustainability of current domestic rebar prices if market activity does not improve.

In contrast, the wire rod market strengthened further during the week. Tight regional supply enabled domestic producers to implement another round of price increases, while Chinese offers remained less competitive due to elevated inland logistics costs, higher port charges, and longer delivery times. Consequently, buyers continued to favour locally available material for prompt deliveries despite lower Chinese CFR offers.

Meanwhile, uncertainty surrounding regional shipping disruptions continued to influence market sentiment. Participants noted that prolonged logistics challenges across the GCC could delay shipments of scrap, billet, hot-rolled coil and finished steel, while higher freight costs and extended transit times may further slow fresh trading activity.

Outlook

BigMint expects the UAE processed scrap market to remain under pressure in the coming weeks as ample domestic availability and weak steel demand continue to limit buying activity. Unless construction activity improves or export opportunities strengthen, buyers are likely to maintain a cautious procurement strategy, keeping prices under downward pressure. At the same time, market participants will closely monitor the impact of export restrictions and regional logistics developments on scrap availability, trade flows, and pricing across the GCC.

Leave a Reply