- Sponge iron prices fall across markets

- Buyers cautious amid bearish sentiment

Sponge iron prices declined by INR 50-200/t across markets on 10 July 2026, with the exception of Raigarh, where prices increased by INR 50/t. The uptick in Raigarh was mainly supported by the availability of adequately priced material that had previously been sold at lower rates to neighbouring markets, helping stabilise local prices.

Market scenario

Overall, the market sentiment remained bearish throughout the week. Week-on-week (w-o-w), PDRI prices declined by approximately INR 100-600/t, reflecting the soft market trend driven by limited downstream demand and weak buying interest.

Buyers continued to adopt a wait-and-watch approach, anticipating further price corrections. As prices have been declining almost every day, most buyers preferred purchasing only against immediate requirements rather than building inventories. Consequently, the market witnessed predominantly need-based buying, while bulk procurement remained largely absent during the week.

Overview of regional markets

Southern region

The southern region remained relatively stable compared to other regions. Producers were reluctant to reduce prices significantly due to persistent margin pressure arising from firm raw material costs. Buyers also avoided bulk purchases and increasingly sourced material from more competitively priced markets, particularly the central region

Central and eastern regions

In the central and eastern regions, sponge iron prices declined by INR 100-600/t w-o-w, reflecting subdued buying interest and weaker demand from the finished steel sector. Lower finished steel demand has indirectly reduced sponge iron consumption. Additionally, liquidity constraints and limited fund availability discouraged buyers from making large-volume purchases. Some buyers from the western region were also observed procuring sponge iron from Durgapur and Ramgarh, attracted by their comparatively competitive prices.

Raw material scenario

Raw material prices remained largely stable during the week. Coal prices witnessed a marginal decline, while iron ore pellet prices remained steady. As a result, production costs did not ease significantly, and sponge iron manufacturers continued to face margin pressure. Consequently, producers were reluctant to implement sharp price cuts. Although some mills offered discounts to stimulate demand and attract buyers, the response remained weak amid the prevailing bearish market sentiment and cautious buying activity.

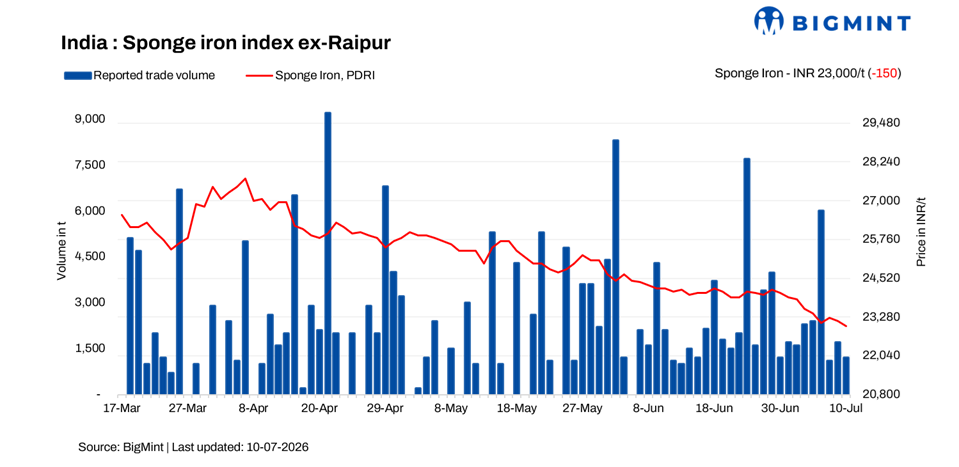

Trading remained sluggish throughout the week. According to BigMint, total recorded sponge iron trades on 10 July stood at approximately 11,000 t, around 4,600 t lower than yesterday. The lower trade volume reflects subdued buying interest and confirms the prevailing weak market sentiment.

NMDC price revision

Adding further pressure to market sentiment, NMDC, India’s largest merchant iron ore mining company, reduced its iron ore list prices effective 10 July 2026. As learnt by BigMint from market sources, the miner has fixed the price of DR CLO (10-40 mm, Fe 67%) at INR 5,850/t (USD 61/t) and iron ore fines (-10 mm, Fe 64%) at INR 4,700/t (USD 49/t), on an FOR basis from its Bacheli complex, excluding royalty, DMF, and NMET charges. Prices across all grades have been reduced by INR 150-500/t, which may further weigh on sponge iron market sentiment in the near term.

Rationale

Prices have been derived based on transactions, offers, bids, and indicative price data sets. Transactions are considered as T1 and given a weightage of 50%, whereas other data sets are considered as T2 and given a weightage of the balance 50%.

Click here for detailed methodology

Leave a Reply