- Port inventories decline over 54% since mid-June

- Cement buyers optimise multi-fuel procurement

Lower petcoke prices are restoring their calorific-value advantage, but ample domestic coal availability, weak monsoon demand and cautious cement-sector procurement are preventing an immediate recovery in buying.

India’s market for high-calorific-value US Northern Appalachian (NAPP) coal is entering a new phase as cement producers rebalance their fuel mix in response to changing economics. While retail NAPP prices have remained broadly stable across western India, demand has softened with the onset of the monsoon. At the same time, a sharp correction in international petcoke prices is beginning to restore its competitiveness, encouraging cement manufacturers to reassess the balance between petcoke, imported coal and domestic coal.

Rather than committing to one fuel, buyers are increasingly optimising their procurement strategy according to delivered cost, plant operating requirements and inventory positions.

Key Market Indicators

Coal and petcoke price assessments reflect market conditions during 8-9 July 2026. Indian retail prices and market feedback are based on trade surveys and port stock/lifting data.

NAPP Market Holds Firm Despite Seasonal Slowdown

US high-CV NAPP coal continues to trade at around INR 13,400-13,500/t in western India, while ILB coal remains available near INR 11,500/t. Prices have changed little over recent weeks despite noticeably weaker buying activity.

The monsoon has curtailed demand from brick kilns and several smaller industrial users, leaving purchases largely confined to immediate operational requirements. Cement producers are similarly avoiding large inventory build-ups as they monitor fuel prices and seasonal demand.

Retail lifting at Kandla and Tuna ports has fallen almost 46% over the past three weeks, while combined inventories have declined by more than 54% to 185,247 t. Although lower stocks could normally support higher prices, the simultaneous fall in weekly dispatches suggests that inventory reductions are being driven more by limited replenishment than by stronger end-user demand.

Fresh US cargoes also face a freight disadvantage. While FOB Baltimore 6,900 NAR coal has eased to US$86.65/t, Panamax freight to India remains around US$51/t, reducing the competitiveness of replacement imports. Existing inventories imported at earlier prices therefore continue to underpin the retail market.

Petcoke economics improve significantly

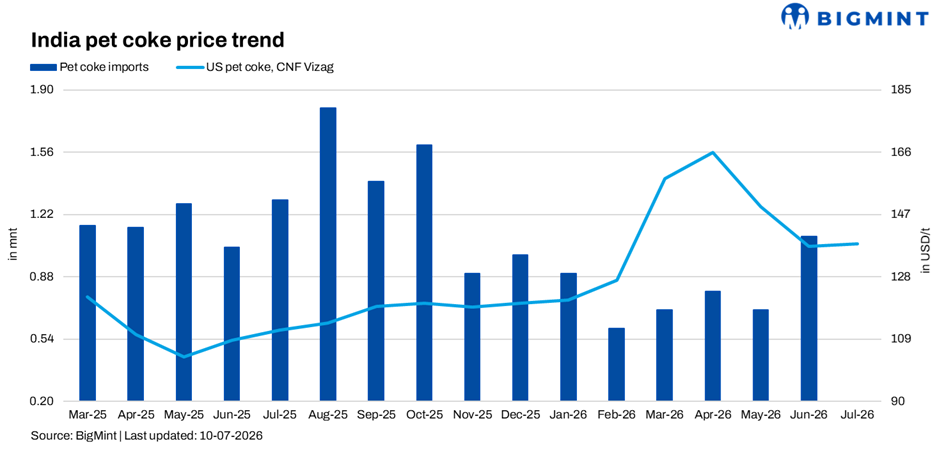

The biggest development has been the sharp correction in international petcoke prices.

High-sulphur petcoke delivered into India is now being indicated around US$135-140/t CFR, down from levels approaching US$160/t only a few weeks ago. FOB US Gulf Coast prices remain relatively soft at US$77.75-80/t, with freight accounting for a significant portion of delivered costs.

The decline has substantially improved petcoke’s competitiveness for cement manufacturers. Industry estimates indicate that the correction could reduce cement production costs by around INR 100/t, although the benefit is expected to become visible mainly during Q3FY27 as lower-cost inventories replace material purchased at earlier, higher prices.

Despite this improvement, buying has remained cautious. Several producers believe prices could soften further and therefore continue to procure only limited spot volumes.

Fuel procurement becomes flexible

The Indian cement industry is no longer making procurement decisions based solely on the headline price of coal or petcoke.

Instead, producers are optimising their fuel basket by balancing domestic coal, imported thermal coal, US NAPP coal and petcoke according to delivered energy cost, sulphur limits, kiln operating requirements, logistics and existing inventories.

US NAPP coal continues to retain an important role because of its high calorific value, low ash content and favourable combustion characteristics. Petcoke, meanwhile, offers superior heat value and lower energy cost but remains subject to operational limits associated with sulphur content.

As a result, the market is not witnessing a wholesale shift from coal to petcoke. Instead, buyers are selectively purchasing whichever fuel offers the best overall economics at a particular point in time.

Petcoke imports reflect disciplined buying strategy

India’s import data reinforces the shift towards more dynamic fuel procurement. Petcoke imports declined 37.3% year-on-year during H1 2026 to 4.7 Mnt, compared with 7.5 Mnt during the corresponding period last year. The reduction was significantly steeper than the decline in non-coking coal imports, indicating that cement manufacturers increasingly treated petcoke as a discretionary blending fuel rather than a fixed component of their fuel basket.

The United States retained its position as India’s largest supplier, accounting for more than 55% of total imported volumes despite the overall decline. June was also the only month during H1 2026 in which imports exceeded year-ago levels, suggesting that some buyers returned to the market following the recent correction.

The data suggests that buyers have not moved away from petcoke permanently. Instead, procurement has become more disciplined, with purchases closely aligned to prevailing economics and inventory requirements.

Cement producers focused on cost control

The correction in petcoke prices comes at an important time for India’s cement industry.

Industry volumes are estimated to have grown by around 8% year-on-year during Q1FY27, supported by healthy dispatches from leading producers. However, higher operating costs continue to weigh on profitability despite firmer cement prices.

Sector estimates indicate weighted average EBITDA of around INR 1,057/t, with the monsoon quarter expected to remain challenging as seasonal demand weakens. Although lower petcoke prices should eventually reduce fuel costs, analysts expect much of the benefit to emerge only during Q3FY27 as lower-cost inventories begin flowing through production.

This explains the cautious procurement strategy currently visible across the market. Rather than rebuilding inventories aggressively, cement companies are purchasing only against near-term requirements while monitoring both petcoke and coal prices.

Edge for petcoke but coal retains its place

The recent correction has restored much of petcoke’s advantage on a delivered energy basis. Its significantly higher calorific value means that, despite a higher price per tonne than imported thermal coal, it continues to offer a lower fuel cost per unit of heat for cement kilns.

However, procurement decisions are driven by more than fuel cost alone. Higher sulphur content, combustion characteristics and plant-specific operating constraints mean that cement producers cannot maximise petcoke consumption indefinitely. Conversely, US NAPP coal continues to provide high calorific value, relatively low ash and greater operational flexibility, making it an attractive blending fuel whenever relative economics favour coal.

Competition between the two fuels has therefore become increasingly tactical rather than structural, with buyers continuously adjusting fuel blends according to market conditions.

Outlook

The balance of fuel economics is gradually shifting back in favour of petcoke, and its share in cement fuel blends is expected to recover during the second half of 2026 if international prices remain around current levels. However, any recovery in imports is likely to be gradual rather than immediate.

Comfortable domestic coal availability, adequate inventories and seasonally weaker cement demand during the monsoon will continue to encourage disciplined procurement. At the same time, freight remains a significant component of delivered costs for both US petcoke and US East Coast coal, limiting aggressive import buying.

For US high-CV NAPP coal, retail prices are expected to remain broadly stable, supported by lower port inventories and its continuing role as a premium blending fuel. Fresh import demand, however, is likely to remain subdued until post-monsoon industrial activity improves or freight economics become more favourable.

The broader market trend is clear. Rather than choosing between coal and petcoke, Indian cement manufacturers are increasingly adopting a flexible fuel procurement strategy—continuously adjusting the balance between domestic coal, imported coal and petcoke to minimise production costs while maintaining kiln efficiency. That flexibility is likely to remain the defining characteristic of India’s industrial fuel market through the remainder of 2026.

Leave a Reply