- Seasonal disruptions continue to slow recycling operations across yards

- Weak steel demand keeps mill procurement cautious and trade volumes subdued

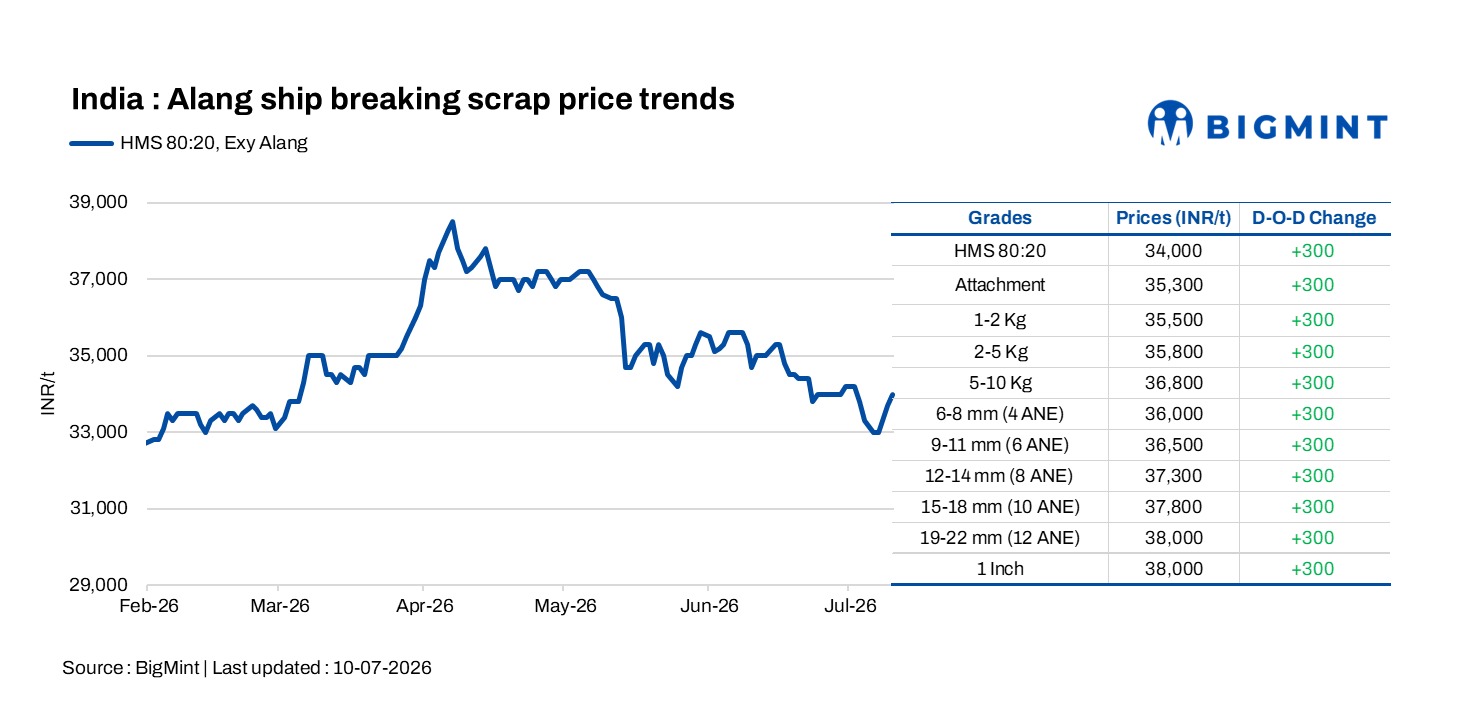

Ship-breaking melting scrap prices in Alang, Gujarat, increased on 10 July, with HMS (80:20) assessed at INR 34,000/t ($357/t) ex-yard. The rise was primarily driven by persistent monsoon rainfall, which disrupted ship-cutting operations and reduced the supply of processed melting scrap entering the market.

Market participants said price variations continued across individual recycling yards, reflecting differences in inventory levels and operational efficiency rather than a broad shortage of quality scrap. Seasonal weather conditions slowed processing activity, limiting the availability of finished scrap and supporting offers despite subdued buying interest.

Gujarat market update

The strength in Alang scrap prices contrasted with weakness across Gujarat’s secondary steel market. In Bhavnagar, billet prices declined by INR 100/t day on day to INR 39,900/t DAP, while Ahmedabad rebar prices fell by INR 300/t to INR 45,000/t ex-works.

Steelmakers continued to procure raw materials only against immediate production requirements as weak finished steel demand discouraged inventory building. The cautious procurement pattern limited trading activity despite tighter scrap availability.

Mandi market update

In Mandi Gobindgarh, billet prices fell by INR 150/t to INR 42,150/t DAP, while HMS (80:20) melting scrap prices eased by INR 100/t to INR 34,000/t DAP. Rebar prices remained stable at INR 46,800/t ex-works.

Market activity remained subdued, with low transaction volumes as competitively priced semi-finished and finished steel from neighbouring markets continued to pressure local demand and mill pricing.

Outlook

Alang scrap prices are expected to remain supported as long as monsoon-related disruptions continue to constrain processing activity. However, any sustained upside is likely to be capped by weak downstream steel consumption, with mills expected to maintain need-based procurement until demand for finished steel improves.

Leave a Reply