- India, Canada and Chile raise shipments on improved cargo flows

- Cautious market sentiment keeps Capesize freight rates under pressure

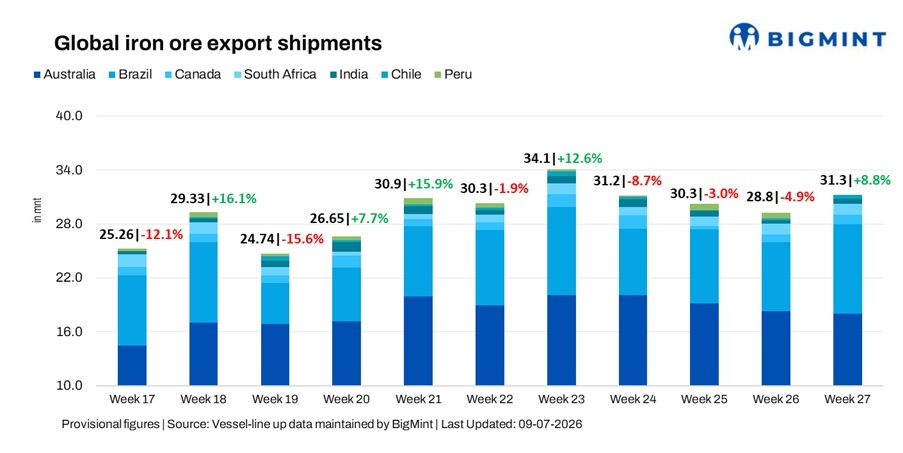

Global iron ore export shipments rebounded 8.8% w-o-w to a three-week high of 31.3 million tonnes (mnt) in the week ended 3 July, recovering after a three-week decline. The increase was driven by stronger cargo flows from Brazil, India, Canada and Chile, according to BigMint data.

Improved Vale dispatches and steady Brazilian port operations supported overall momentum, while Australian shipments remained largely stable amid moderated Pilbara loadings.

Country-wise trends

Port & shipper-wise trends

- Australia: Port Hedland handled 11.55 mnt, followed by Port Walcott (3.33 mnt) and Dampier (3.02 mnt). BHP shipped 6.79 mnt, followed by Rio Tinto (6.35 mnt) and FMG (3.53 mnt). China remained the leading destination at 15.04 mnt, followed by Japan (1.33 mnt) and South Korea (1.05 mnt).

- Brazil: Ponta da Madeira handled 4.21 mnt, followed by Tubarao (2.46 mnt) and Itaguai (1.56 mnt). Vale shipped 4.99 mnt, while CSN & Vale accounted for 4.02 mnt. China remained the largest importer at 5.02 mnt.

- Canada: Sept-Iles handled 0.61 mnt, followed by Port Cartier (0.49 mnt). AMNS shipped 0.49 mnt, while IOC accounted for 0.43 mnt. The Netherlands emerged as the key destination at 0.26 mnt, followed by Spain (0.17 mnt).

- South Africa: Saldanha handled 1.08 mnt, followed by Richards Bay (0.16 mnt). China remained the leading importer at 0.38 mnt.

- India: Dhamra handled 0.27 mnt, followed by Paradip (0.18 mnt). Rungta Sons shipped 0.18 mnt, while China remained the major destination at 0.45 mnt.

- Chile: Totoralillo and Huasco handled 0.20 mnt each. China accounted for the entire shipment volume at 0.44 mnt.

- Peru: No shipments were recorded during the week.

Freight market remains under pressure amid cautious sentiment

The dry bulk iron ore freight market remained subdued as weak Capesize demand, limited fresh cargo enquiries and sufficient vessel availability continued to pressure rates. Although Brazilian shipment activity improved, market sentiment remained cautious amid uncertainty over sustained cargo volumes.

The Pacific market remained soft due to slower activity, while Atlantic sentiment saw limited support from improved Brazil cargo flows. Panamax and Supramax segments remained relatively steady, supported by selective cargo demand and balanced tonnage availability.

Outlook

Global iron ore shipments are expected to remain range-bound, with Brazilian loading programmes, Pilbara supply trends and Chinese steel demand likely to guide seaborne flows. Freight sentiment may stay cautious in the near term, with Capesize recovery dependent on stronger cargo enquiries, while smaller vessel segments are expected to remain comparatively stable.

Leave a Reply