- Coal competition reshapes cement fuel procurement

- US retains dominance despite lower shipments

India’s petcoke imports declined sharply during the first half of 2026 as cement manufacturers reduced purchases amid improving domestic coal availability and changing fuel economics. While the United States retained its position as India’s dominant supplier, overall import volumes fell by more than one-third, indicating a more cautious procurement approach by industrial consumers.

The contraction was significantly steeper than the decline in non-coking coal imports, suggesting that cement producers increasingly treated petcoke as a discretionary blending fuel rather than an essential component of their fuel basket. With domestic coal supplies improving and imported thermal coal remaining competitively priced, the incentive to maximise petcoke consumption weakened considerably.

Petcoke imports register a sharp contraction

India imported 4.7 mnt of petcoke during January-June 2026, compared with 7.5 mnt during the corresponding period of 2025, representing a decline of 37.3%.

Unlike non-coking coal imports, which declined gradually through the first half, petcoke purchases remained below year-ago levels in almost every month.

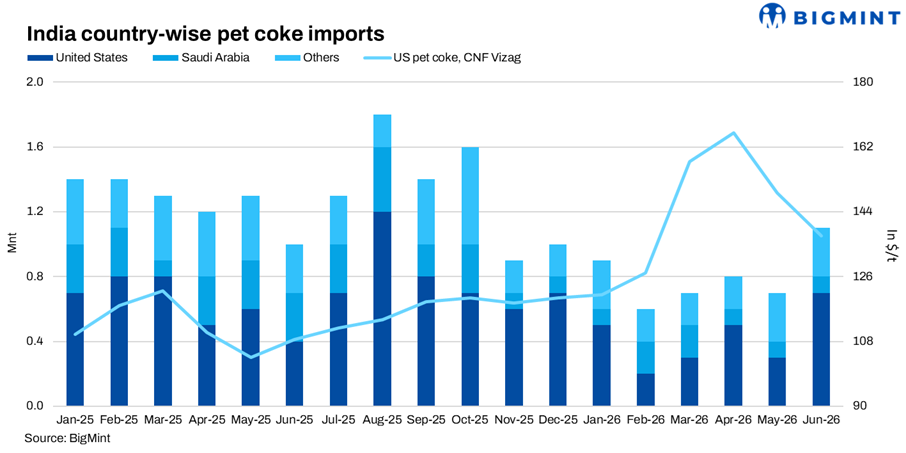

Monthly petcoke imports

June was the only month during H1 2026 in which imports exceeded the previous year’s level, suggesting that some buyers returned to the market to take advantage of favourable pricing after the earlier correction in international petcoke markets.

Nevertheless, the broader trend remained firmly downward, reflecting weaker underlying demand rather than temporary procurement delays.

Imported petcoke prices remain volatile

Imported petcoke prices remained volatile during H1 2026. Prices surged sharply during April and May as geopolitical tensions in the Middle East, higher freight costs and supply disruptions pushed CFR India offers to around $150-155/t. However, easing tensions and improving freight availability led to a correction of around $20-25/t by the end of June. Despite the decline, cement producers remained cautious, increasingly comparing petcoke with US NAPP, Russian and domestic coal on delivered fuel economics rather than headline prices.

United States dominant supplier

The United States continued to dominate India’s imported petcoke market despite lower overall volumes.

Petcoke imports by origin

Although US shipments declined in absolute terms, the country increased its market share slightly to more than 55% of India’s total petcoke imports.

Saudi Arabian and Venezuelan exports registered the sharpest declines, while China emerged as a modest supplier during H1 2026, albeit from a very low base.

The data highlights that buyers largely reduced purchases across all origins rather than switching aggressively between suppliers.

Saudi supply disrupted during geopolitical tensions

Geopolitical tensions also affected trade flows from the Middle East. Saudi-origin petcoke offers were largely absent from the Indian market during the conflict, limiting procurement options for buyers. Although supply gradually started returning towards the end of June, market activity remained limited as many cement producers had shifted to alternative fuels, including US NAPP, Russian thermal coal and domestic coal, while others delayed purchases in anticipation of lower petcoke prices.

Fuel economics reshape procurement

The sharp decline in imports reflects changing economics within India’s cement industry rather than a structural loss of relevance for petcoke. Historically, cement manufacturers have used petcoke as a supplementary kiln fuel because of its high calorific value and favourable pricing relative to imported coal. However, fuel selection is largely determined by relative economics rather than fixed consumption patterns.

During H1 2026, greater availability of domestic coal, comfortable inventories and improved domestic logistics reduced the need for imported alternative fuels. As imported thermal coal prices softened and domestic coal remained readily available, the economic advantage of petcoke narrowed. Consequently, cement producers increasingly optimised fuel blends instead of maximising petcoke consumption.

Rather than replacing coal, petcoke continued to function as a complementary fuel whose consumption was adjusted according to prevailing market conditions.

Domestic production remains lower

The decline in imports was not driven by higher domestic petcoke production. India’s domestic petcoke output remained below last year’s level, indicating that lower imports primarily reflected weaker consumption rather than increased local supply. During April-May FY26, domestic petcoke production declined 6.8% y-o-y to 2.32 mnt, while May production fell 5.3% y-o-y to 1.20 mnt, despite improving 6.7% m-o-m over April. The data suggests that changing fuel economics, rather than higher domestic production, remained the key factor behind lower import demand.

Regional import pattern remains broadly balanced

The geographical distribution of imports changed only marginally.

Coast-wise distribution

The West Coast marginally increased its share of imports, reflecting the continued dominance of US and Middle Eastern cargoes discharged through western Indian ports. The sharper decline in East Coast imports is also consistent with improving availability of domestic coal in eastern India, reducing dependence on imported fuels.

Cement sector adopts flexible fuel strategy

The H1 2026 import data suggests that cement manufacturers are adopting increasingly dynamic fuel procurement strategies.

Instead of maintaining fixed consumption ratios between coal and petcoke, buyers appear to be adjusting fuel blends more actively in response to changes in domestic coal availability, imported fuel prices and operational requirements.

The sharp contraction in petcoke imports despite generally softer international prices illustrates that procurement decisions are now being driven by overall fuel optimisation rather than simply purchasing the lowest-cost imported fuel.

This also reflects greater confidence in domestic coal supply, allowing cement producers to rely less heavily on imported petcoke for kiln operations.

Outlook

Petcoke imports are expected to remain sensitive to relative fuel economics during the remainder of 2026.

Should international petcoke prices weaken significantly relative to high-calorific-value coal, buying interest could recover, particularly among cement manufacturers seeking to lower fuel costs. However, any rebound is likely to be measured as long as domestic coal availability remains comfortable and industrial consumers continue to enjoy reliable domestic supplies.

Overall, H1 2026 marks a shift towards more disciplined and flexible fuel procurement. Rather than signalling a structural decline in petcoke consumption, the import data indicates that Indian cement producers are increasingly using petcoke selectively–balancing cost, calorific value and operational efficiency within a broader, more diversified fuel portfolio.

With imported petcoke prices correcting sharply from May highs and domestic refinery prices also easing, cement producers are expected to continue optimising fuel blends between petcoke, imported coal and domestic coal depending on relative economics.

Leave a Reply