- Copper concentrate imports rise 62% y-o-y in 4M CY’26

- Expanding smelting capacity widens India’s dependence on imports

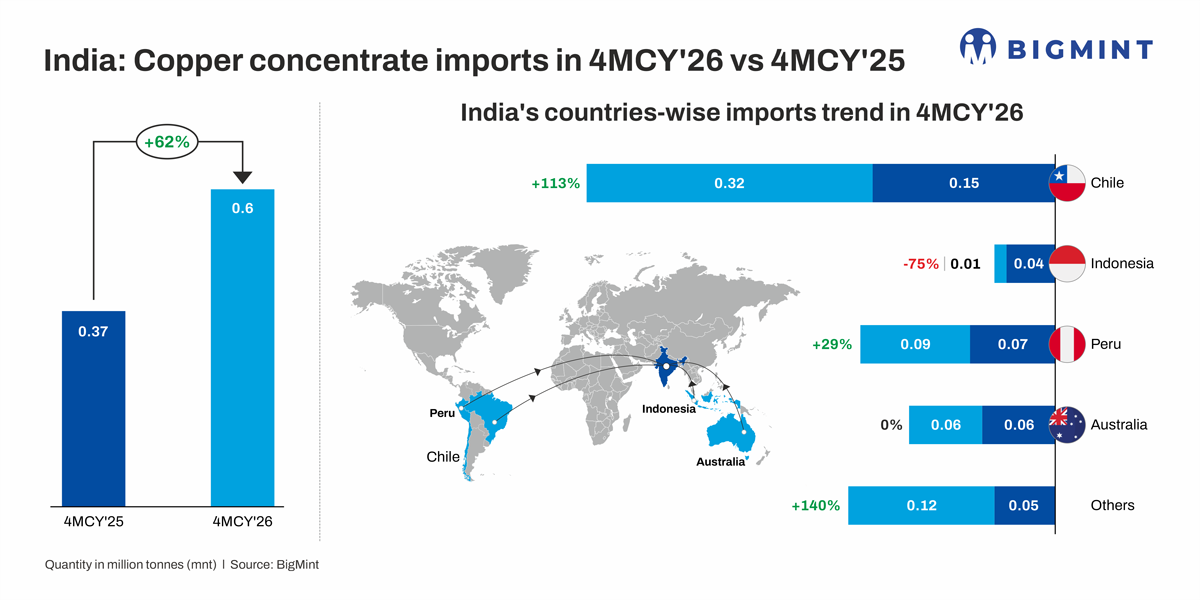

India’s dependence on imported copper ore and concentrates is continuing to intensify as growth in downstream refining capacity significantly outpaces expansion in domestic mining. Copper concentrate imports reached 0.60 million tonnes (mnt) during the first four months of CY’26 (4MCY’26), up 62% year on year from 0.37 mnt in the corresponding period of 2025. Notably, imports during just four months have already reached nearly 70% of the country’s total concentrate imports recorded in 2021, highlighting the structural shift in India’s copper supply chain.

Over the past five years, India’s copper ore and concentrate imports have steadily increased from 0.87 mnt in 2021 to 1.44 mnt in 2025, registering a compound annual growth rate (CAGR) of around 13%. While domestic copper mining has improved during the period, the pace of expansion has remained insufficient to support the country’s rapidly growing smelting and refining industry.

Copper concentrate imports rising despite higher domestic mining

India’s domestic copper mining sector has continued to record gradual improvements. Hindustan Copper Limited (HCL), the country’s only primary copper mining company, produced 3.67 mnt of ore during FY’26, registering 6% year-on-year growth, supported by higher mining activity, operational optimisation and the resumption of key mining assets.

Consequently, metal-in-concentrate (MIC) production increased by 9% y-o-y to 27,421 tonnes, marking the company’s highest annual MIC production in the past seven years.

Despite this encouraging performance, HCL currently meets only around 4% of India’s overall MIC requirement, while nearly 96% of the country’s concentrate demand continues to be met through imports. This underscores the widening structural imbalance between India’s limited upstream resource base and its rapidly expanding downstream copper industry.

How is refining capacity reshaping India’s copper demand?

The principal driver behind rising concentrate imports is the rapid expansion of India’s copper refining capacity. Strong demand from power transmission, renewable energy, electric vehicles, electronics and infrastructure has encouraged significant investments in smelting and refining over the past few years. However, India’s relatively limited copper ore reserves have prevented domestic mining from expanding at a similar pace, making imported concentrates the primary source of feedstock for new capacity.

The trend became increasingly evident during 4M CY’26, when India’s refined copper production rose 8% year on year to approximately 0.22 mnt. The increase was largely driven by the commissioning and progressive ramp-up of Adani Group’s Kutch Copper Ltd. (KCL), whose refined copper production surged to 31,000 tonnes during the period from just 2,300 tonnes in the corresponding period of 2025, representing an increase of more than 1,200% as the newly commissioned smelter steadily increased operating rates.

Although production at established producers such as Hindalco and Sesa Sterlite moderated during the period, KCL’s additional output more than offset the decline, resulting in higher overall refined copper production and a corresponding increase in demand for imported concentrates.

How is India securing concentrate amid tighter global supply?

India’s growing appetite for copper concentrates has coincided with tighter conditions in the global concentrate market. According to the International Copper Study Group (ICSG), global copper mine production increased from 21.91 mnt in 2022 to 23.22 mnt in 2025. However, mine production declined marginally by 1.3% year on year to 7.45 mnt during 4MCY’26 owing to supply disruptions across several major producing countries.

Chile experienced production losses due to water constraints at Collahuasi, an underground incident at El Teniente and widespread power outages across northern mining regions. Indonesia’s concentrate exports were affected by the introduction of a 7.5% export tariff alongside operational disruptions at the Grasberg mine. Meanwhile, flooding disrupted production at the Kamoa mine in the Democratic Republic of Congo (DRC), while Panama’s Cobre Panama mine remained largely idle, removing approximately 0.35 mnt of annual concentrate capacity from the global market.

Despite tighter global availability, India successfully diversified its sourcing strategy. Chile strengthened its position as India’s largest concentrate supplier during 4M CY’26, with shipments increasing 113% year on year to 0.32 mnt, accounting for more than half of India’s total concentrate imports. The increase was further supported by Codelco’s long-term concentrate supply agreement with KCL, reinforcing Chile’s strategic importance in supplying India’s expanding refining industry.

Peru remained the second-largest supplier, with exports to India increasing 29% year on year to 0.09 mnt, supported by higher production from the expanded Toromocho mine. Meanwhile, imports from Indonesia declined sharply by 75% to 0.01 mnt, while shipments from Australia remained broadly stable at around 0.06 mnt. Imports from Canada, Brazil and other countries increased 140% year on year to 0.12 mnt, highlighting India’s efforts to diversify procurement amid intensifying competition for copper concentrates.

Alongside domestic expansion, India is also securing long-term overseas concentrate supplies. In July 2025, Adani Group’s Kutch Copper Ltd. (KCL) signed an MoU with Australia’s Caravel Minerals Ltd. to explore investment and long-term offtake from the Caravel Copper Project. The agreement could provide KCL with up to 100% of the project’s copper concentrate output, strengthening feedstock security for its Mundra smelter and diversifying India’s concentrate supply sources.

Can HCL bridge India’s copper supply gap?

Recognising the widening gap between domestic concentrate production and downstream demand, HCL has accelerated its Vision 2030 strategy to strengthen India’s upstream copper sector. The company has announced a capital expenditure programme of INR 7,188 crore to expand ore production capacity from the current 4 mnt/year to 12.2 mnt by FY’30.

The strategy combines brownfield expansion, mine revival, processing infrastructure upgrades and greenfield exploration. A key project is the establishment of a new 3 mnt concentrator plant at the Malanjkhand Copper Project in Madhya Pradesh through an investment of ₹469.55 crore.

HCL has also resumed operations at the Kendadih, Kolihan and Surda mines while expanding concentrator capacity at the Indian Copper Complex from 0.4 mnt to 0.9 mnt. In parallel, the company has secured the Sidhi Copper Block through auction, advanced exploration activities at Sikkim, Dhobani and Pathargora, and continues to evaluate overseas mineral opportunities, including prospective investments in Chile, to strengthen long-term resource security.

Will import dependence continue?

HCL’s expansion programme is expected to substantially strengthen India’s domestic copper mining industry over the coming years. However, it is unlikely to eliminate the country’s reliance on imported concentrates in the foreseeable future. Mining projects typically require long development timelines before reaching commercial production, whereas refining capacity has already expanded and continues to ramp up.

As India positions itself as a global manufacturing hub for renewable energy equipment, electric vehicles, electrical infrastructure and electronics, demand for refined copper is expected to remain robust. Consequently, imported concentrates will continue to play a critical role in supporting domestic smelters, making long-term supply agreements, diversified sourcing strategies and overseas resource investments increasingly important for ensuring feedstock security.

India’s copper industry is therefore entering a new phase in which the challenge is no longer expanding refining capacity but securing sufficient concentrate to utilise it efficiently. Until domestic mining catches up with downstream growth, imports are expected to remain the backbone of the country’s copper value chain.

Leave a Reply