- Chinese iron ore prices fall 7% on shrinking mill profits, high port stocks

- Indian imported coking coal prices buck trend, inch up on tight supply

- Chinese HRC prices dip m-o-m but remain elevated near Oct’24 highs

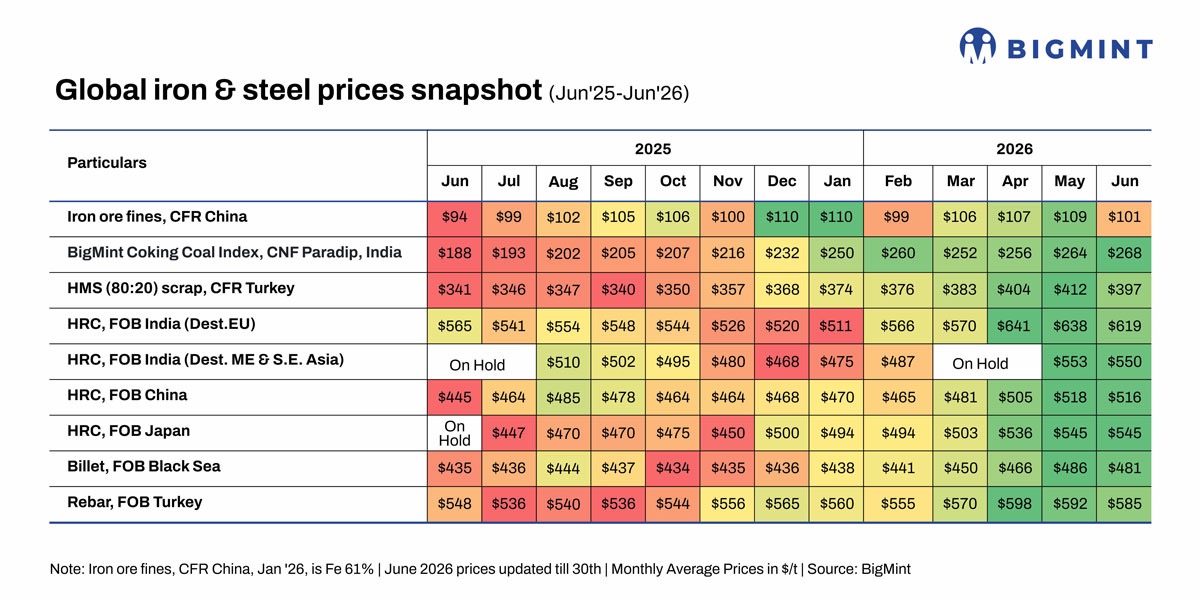

Morning Brief: Global steel and raw material prices declined m-o-m in June 2026 across major markets, halting the sustained uptrend since the outbreak of the US-Iran conflict and the resulting Middle East crisis.

Iron ore prices fell the sharpest, by 7% m-o-m, but other commodities recorded softer corrections, by up to 4%. Only Japanese HRC prices remained stable, while Indian imported coking coal prices inched up by 2%.

Easing Middle East tensions reduced freight costs and removed an important source of price support seen during March-May. Meanwhile, the rainy season in Asia and summer slowdowns in other regions weakened steel demand. Although elevated coking coal prices supported steelmaking costs, lower iron ore and scrap prices ultimately drove a broad-based correction in global steel prices.

Snapshot of global steel, raw material price movements in Jun’26

Chinese imported iron ore (Fe 61%): Chinese iron ore prices fell 7% m-o-m to $101/tonne (t) CFR, though blast furnace utilisation improved, with daily hot metal output assessed at 2.41-2.43 million tonnes (mnt) in June compared with 2.39-2.41 mnt/day in May.

The decline was driven by weaker seasonal steel demand as high temperatures and heavy rains in China slowed construction activity, while global trade barriers weighed on steel exports.

Steelmakers also faced mounting cost pressure after multiple met coke price hikes squeezed margins, prompting cautious raw material procurement. Several mills announced maintenance shutdowns or considered output cuts for July, raising expectations of weaker iron ore demand. Around 51% of mills were profitable by end-June 2026 against over 60% in end-May and nearly 60% in June 2025.

Additionally, supply remained elevated, with Chinese portside stocks assessed by Mysteel at 168 mnt on 26 June. The decline was reinforced by a sharp fall in seaborne freights following easing geopolitical tensions in the Middle East, which reduced delivered costs for imported ore. Capesize freights from Port Hedland, Australia, to Qingdao, China, eased to $12.3/dry metric tonne (dmt) in June from $15.1/dmt in May.

Indian imported coking coal: BigMint’s coking coal index increased by 1.5% m-o-m to $268/t CNF India, supported by stronger Chinese procurement. Mining disruptions and stricter safety inspections caused by the Shanxi mine accident tightened spot availability and prompted suppliers to raise offers.

Supply also remained tight last month, driven by reduced production and prolonged waiting times for berthing of vessels. Additionally, Chinese coke producers were able to successfully implement roughly four rounds of price hikes in June, further supporting global coking coal prices.

However, gains were partially capped by subdued buying interest from Indian consumers, as adequate inventories, cautious procurement strategies, and elevated import costs limited spot market activity.

Turkish imported scrap: Subdued rebar demand pulled down Turkiye’s imported HMS 80:20 prices by 4% m-o-m to $397/t. The market faced additional pressure from ample deep-sea scrap availability, with European recyclers becoming increasingly willing to reduce prices amid weak demand and rising inventory-carrying costs. The availability of competitively priced imported billets further reduced mills’ appetite.

Although firm US domestic scrap prices prevented a steeper correction, Turkish mills reduced bids as rebar export prices weakened and steelmaking margins remained under pressure.

Notably, more than 20 deep-sea cargoes were concluded during the month, including around 15 cargoes booked by two major flat steel producers.

CIS-origin billets: Black Sea billet export prices declined 1% m-o-m to $481/t FOB, as weak Turkish demand and softer imported scrap prices outweighed support from a stronger Russian rouble and firm domestic markets.

Turkish buyers remained cautious, limiting purchases amid sluggish rebar demand, compressed steelmaking margins, and expectations of further corrections in both scrap and billet prices.

Russia also faced mounting competition from Asia and the Middle East. Chinese mills reduced export offers amid weak domestic steel demand, while Iranian suppliers gradually returned to export markets following improvements in logistics, increasing billet availability across key destinations in the Gulf.

Turkish exported rebars: Turkish rebar export prices declined 1% m-o-m to $585/t in June as mills gradually shifted from attempting to recover higher production costs early in the month to subsequently reducing prices to stimulate demand.

At the beginning of June, producers raised export offers following the Eid holidays, citing elevated scrap, energy, and production costs. However, buying interest remained limited, with most overseas customers resisting prices.

As the month progressed, a seasonal summer slowdown in the domestic market, weak construction activity, and subdued export demand forced mills to reduce offers. At the same time, falling imported scrap prices reduced raw material costs.

The scrap-to-rebar spread expanded to $188/t in June from $180/t in May, but it remained slightly below mills’ preferred levels of around $190/t.

Chinese HRC export offers: Chinese hot-rolled coil (HRC) export offers fell marginally by less than 1% m-o-m to $516/t FOB, as seasonal demand weakness and cautious overseas buying offset cost support. However, prices remained on the higher side, near October 2024 levels.

The onset of the rainy season and high temperatures weighed on steel consumption in China and Southeast Asia. Although mills attempted to lift export offers due to higher coke costs, weak demand, softer iron ore, and lower freight expectations limited their pricing power. Large state-owned mills largely tried to keep FOB offers unchanged, while smaller mills reduced offers.

Indian HRC export offers: Indian HRC export offers softened across major destinations in June.

Export offers to the EU averaged around $619/t FOB, down about 3% m-o-m, as buyers largely stayed out of the market ahead of the revised safeguard regime that came into force on 1 July. Uncertainty over lower Indian allocations, higher out-of-quota duties, and additional compliance requirements under the Carbon Border Adjustment Mechanism (CBAM) delayed purchasing decisions. Moreover, India had exhausted Q2CY’26 quotas a few days into April, which limited demand.

Export offers to the Middle East and Southeast Asia remained relatively resilient, dipping 0.5% m-o-m to $550/t FOB. Trade in the Middle East was disrupted early in the month by the Israel-Iran conflict, elevated freights, and uncertainty over vessel movements through the Strait of Hormuz. Although shipping conditions gradually improved later in June, buyers largely continued hand-to-mouth procurement amid expectations of lower prices.

Around 30,000 t were reportedly booked into Vietnam at approximately $535/t FOB, weighing on offers.

However, despite softer export prices, Indian mills continued to push material into overseas markets as subdued domestic demand made exports increasingly attractive.

Outlook

BigMint expects global steel and raw material prices to decline m-o-m in July, with weak seasonal demand continuing to slow trade in most Asian steel markets. Chinese HRC prices remain near a 20-month high, which could keep buyers reluctant to procure material, leading to falling prices.

Falling freights and improving supply are also likely to bring down prices, especially of iron ore, scrap, and coking coal, although the latter may face a slower decline given the extent of suspended mining capacity and sluggish restarts. The price drop will effectively reduce the cost floor for steel prices.

At the macro level, weaker economic growth globally due to the Middle East conflict may also pressure demand. However, growth in Chinese government bond may boost domestic infrastructure demand, supporting steel prices there.

Leave a Reply