- Supply constraints limit downside in scrap prices

- Key casting scrap availability remains constrained

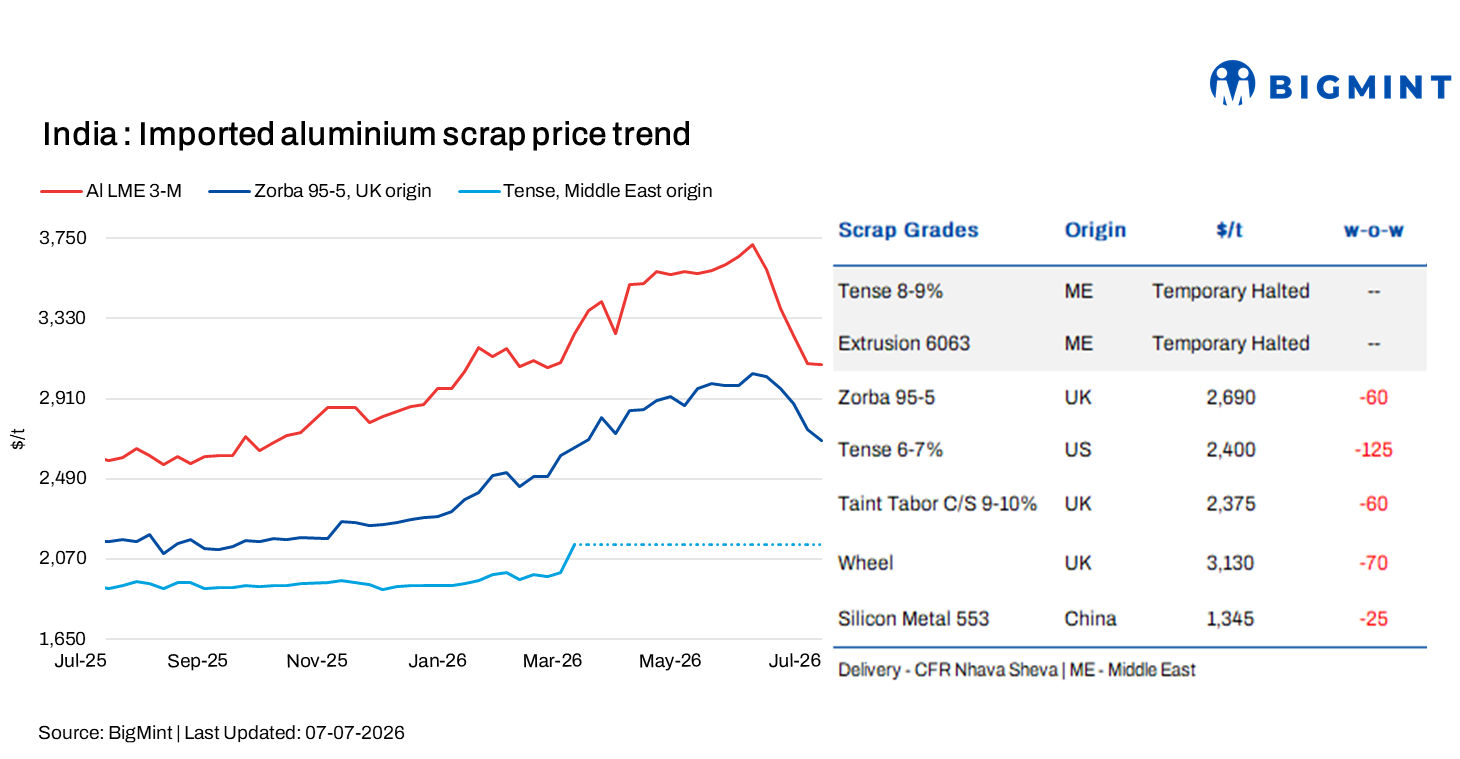

India’s imported aluminium scrap prices declined further w-o-w, tracking continued weakness in LME aluminium prices and subdued buying activity in the domestic market.

According to BigMint’s latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap prices fell by $60/t w-o-w to $2,690/t, while US-origin tense 6-7% scrap prices declined by $125/t w-o-w to $2,400/t.

LME aluminium slips marginally w-o-w

Three-month aluminium prices on the London Metal Exchange (LME) traded lower w-o-w, closing at $3,112/t on 30 June against $3,120/t on 27 June, down by $8/t, or 0.3% w-o-w.

Meanwhile, LME aluminium inventories increased by 8,125 t, or 2.8% w-o-w, to 303,675 t on 30 June from 295,550 t on 27 June.

LME aluminium prices declined w-o-w as supply concerns eased following the reopening of the Strait of Hormuz and the faster-than-expected restart of production at Emirates Global Aluminium’s Al Taweelah smelter. Additional pressure came from plans to restart primary aluminium capacity at Slovalco in Slovakia, along with higher aluminium production in China and expanding smelting capacity in Indonesia, improving expectations for global metal supply.

Market scenario

Imported aluminium scrap prices continued to trend lower this week, mirroring the decline in domestic scrap values as weaker LME aluminium prices weighed on the market. However, the availability of key casting grades, particularly imported wheels and tense scrap, remained constrained.

In the near term, imported scrap prices are expected to witness only a modest correction, tracking movements in the primary aluminium market. Over the medium to long term, the outlook remains supportive due to emerging supply-side risks from key exporting regions.

The UAE has imposed a four-month ban on exports of selected aluminium, ferrous and copper scrap to retain recyclable raw materials for domestic processing. Although the UAE accounts for only around 6% of India’s aluminium scrap imports, it remains a strategically important supplier due to its proximity and shorter transit times. Meanwhile, the European Union is expected to present a proposal on 9 September to introduce a 15% levy on aluminium scrap exports. Europe accounts for nearly 20% of India’s aluminium scrap imports, making the proposed measure significant for global scrap trade flows if approved.

While these measures are yet to be finalised, they have already influenced market expectations. The prospect of tighter scrap availability from key sourcing regions is expected to limit the downside in imported scrap prices. Consequently, although prices may remain under pressure in the short term due to weaker LME aluminium, any correction is likely to be moderate. Market participants will closely monitor developments in the EU ahead of the September decision, as any export restrictions could tighten global scrap availability and support aluminium scrap and secondary alloy prices.

On the domestic front, trading activity also weakened. Following softer global aluminium prices, the domestic market witnessed a notable decline, particularly in casting-grade aluminium scrap prices, which fell sharply w-o-w across both southern and northern regions amid weak demand and cautious buying.

Chinese silicon prices

According to BigMint’s latest assessment, China-origin Silicon Metal 553 prices declined by $25/t w-o-w to $1,345/t CFR Mundra from $1,370/t, as softer Chinese export offers amid weak downstream demand from the polysilicon and aluminium alloy sectors, coupled with comfortable supply availability, weighed on the market.

Outlook

Imported aluminium scrap prices are expected to remain supported over the medium term, as tightening scrap availability from key exporting regions is likely to limit further downside, although near-term price movements will continue to track trends in LME aluminium and the primary aluminium market.

Leave a Reply