- Chinese HRC imports fall 59% m-o-m after halt in export scheme-led arrivals

- Exports rise 2% m-o-m in June amid EU policy uncertainty

- EU cuts steel import quotas sharply, but India will remain a key exporter

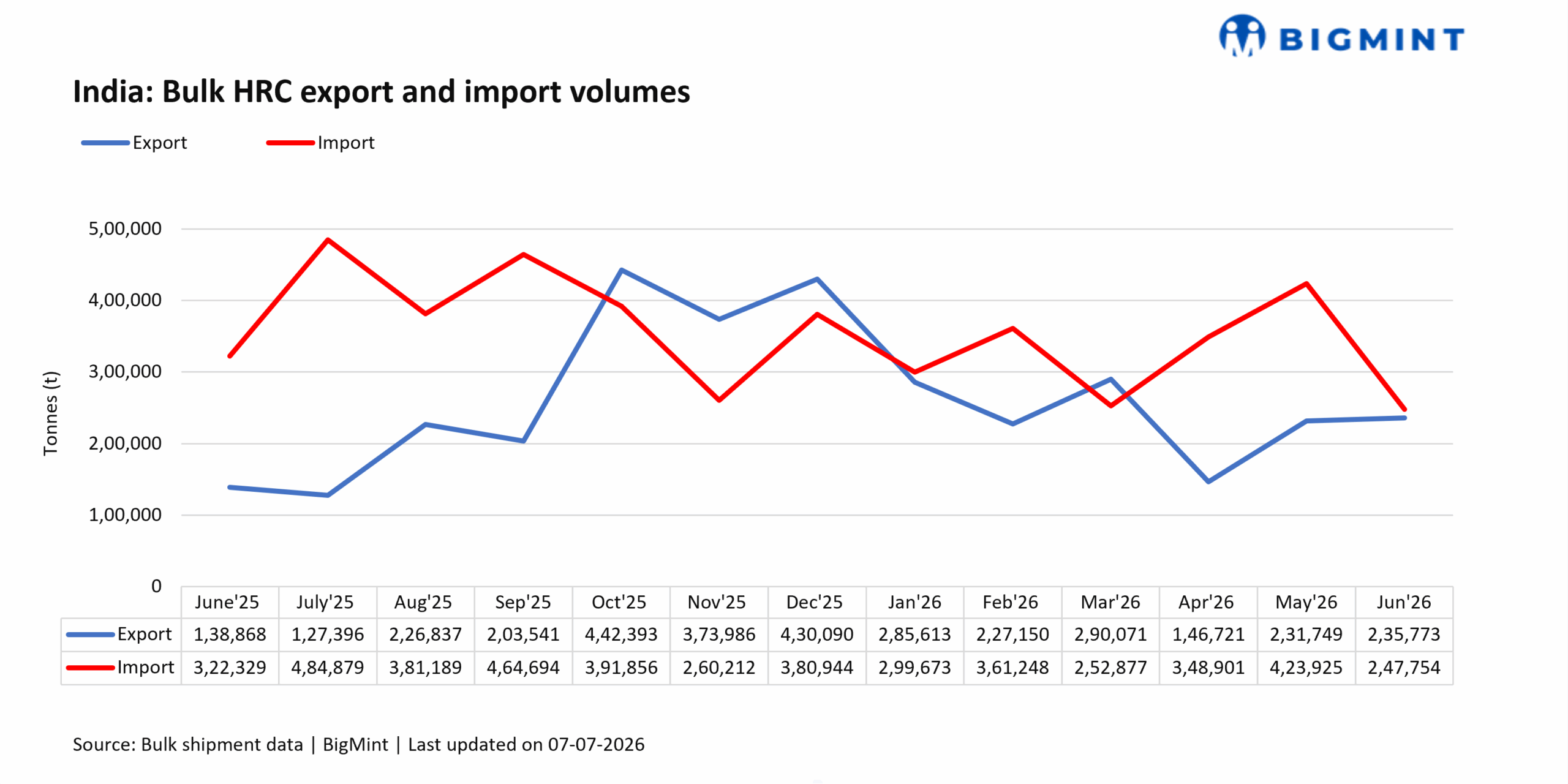

Morning Brief: India remained a net importer of hot-rolled coils (HRCs) during June 2026, though imports exceeded exports by a slim margin of around 12,000 tonnes (t). According to BigMint’s vessel line-up, India’s bulk HRC imports decreased sharply by 42% m-o-m and 23% y-o-y to around 247,800 t in June 2026. At the same time, bulk exports stood at 235,800 t, rising by a massive 71% y-o-y, though the m-o-m growth was limited to a minor 2%.

Besides March, India’s HRC imports have remained higher than exports throughout the first half of this year, though H1CY’26’s cumulative trade deficit of 0.51 million tonnes (mnt) remains a marked improvement over the 1.14 mnt recorded in the year-ago period. The narrower deficit is largely due to stronger exports this year, with shipments surging by 69% y-o-y to 1.42 mnt. However, bulk HRC imports fell merely 3% y-o-y in H1CY’26 to 1.93 mnt despite the safeguard duty.

Drop in Chinese imports drags down Jun’26 volumes

June’s import volumes reflect a sharp moderation from the steep spike recorded in May, when imports increased by 50% y-o-y. An increase in imports from China had driven up overall volumes in May, triggered by two factors.

First, the price spread between domestic (exy-Mumbai) and imported HRCs contracted to around INR 3,000/t in February-March, keeping overseas-origin material competitively priced. The gap between domestic prices and imports from free trade agreement (FTA) countries, Japan specifically, even turned negative, as landed costs of Japanese imports remained lower than domestic prices.

Secondly, export-oriented pipe and tube manufacturers had ramped up Chinese imports under the Advance Authorisation Scheme, which allowed them to avoid the safeguard duty and BIS quality norms that would ordinarily apply to steel entering the domestic market. As such, Chinese HRC imported under the scheme turned commercially viable in May, with an effective landed cost of around INR 52,000-53,000/t compared with domestic HRC prices of roughly INR 58,000-59,000/t.

In June, imports from China fell by 59% m-o-m and 45% y-o-y, indicating a halt in import arrivals under the Advanced Authorisation Scheme. Following April’s surge, there were reports of the government considering trade remedies to stem the inflow of low-priced foreign steel, leading to cautious sentiment.

Eventually, in late June, the government announced an anti-dumping investigation into hot-rolled flat steel products originating in or exported from China, Japan, and Russia. The applicants — JSW Steel, JSW Vijayanagar Metallics, and Jindal Steel Odisha — have also petitioned for retrospective application of duties, which is likely to curb import demand further.

Meanwhile, imports from South Korea increased by 18% m-o-m in June, mainly driven by the arrival of previously contracted cargoes from major mills such as POSCO and Hyundai Steel.

Imports remain uneconomical for buyers in Jul’26

Current pricing, as of 4 July 2026, continues to discourage imports. According to BigMint’s latest assessment, imported HRCs from free trade agreement (FTA) countries is estimated to land in India at around INR 64,307/t, including the 11.5% safeguard duty, port handling charges, and other fees. HRCs from non-FTA origins (China) are estimated to carry a landed cost of around INR 64,879/t.

In comparison, domestic HRC (IS2062, E250 BR, 2.5-8 mm, exy-Mumbai) was assessed at INR 58,200/t as of 4 July, leaving imported material at a premium of approximately INR 6,100/t for FTA countries (expanding from INR 5,700/t in early June) and INR 6,700/t for non-FTA countries (shrinking from INR 7,300/t) over domestic steel.

This substantial pricing gap substantially reduces the commercial incentive for domestic buyers to procure imported HRC for routine consumption. Consequently, import purchases in July are likely to be concentrated in applications where procurement decisions are driven by factors other than headline prices. Flat steel products account for the vast majority of India’s finished steel imports, with a share of about 90%.

Vietnam drives uptrend in exports

India’s HRC exports in June 2026 were primarily directed to Vietnam, with the country receiving 0.12 mnt compared to 0.03 mnt in the previous month. Manufacturing activity in Vietnam has accelerated, with global producers trying to diversify from China. Moreover, Indian exporters also seem to be benefiting from the restrictions on Chinese HRCs.

Exports to Vietnam also increased in June as Indian HRC remained one of the more competitively priced options in the region, while subdued domestic demand prompted steelmakers to push material overseas.

In fact, Vietnam has emerged as the most exported-to country for Indian HRC exporters during H1CY’26, while buyers in India’s traditional markets in the EU such as Spain, Belgium, and Portugal remained absent.

EU buyers remain absent amid lack of clarity on revised safeguard quotas

Notably, in June, import activity across the EU remained subdued after the exhaustion of its Q2CY’26 quarterly quota and ahead of the revised EU safeguard measures scheduled to come into effect from 1 July. Notably, India’s HRC quota under the previous safeguard regime (225,306 t) had already been fully utilised early, at the start of the second quarter.

Importers also remained cautious because of the additional costs associated with the Carbon Border Adjustment Mechanism (CBAM), prompting many to defer purchases until the new country-specific tariff-rate quotas (TRQs) became clear.

While the revised safeguard regime significantly reduces India’s quota allocation across flat steel products, the country remains the EU’s third-largest suppliers after Turkiye and the UK. BigMint’s calculations show that India’s combined allocation across five major flat steel categories has been cut by around 41%, from 2.40 mnt under the previous regime to 1.42 mnt. HRC quotas have been reduced by 34%, cold-rolled coil by 58.8%, metallic coated products by 66.8%, and organic coated products by 31.1%, while only Category 4A metallic coated products registered an increase.

Despite these reductions, India remains one of the EU’s largest country-specific suppliers alongside South Korea and Turkiye. The European Commission has largely based the revised allocations on historical trade patterns, enabling India to retain dedicated quotas across key flat steel categories because of its long-standing position as a major exporter to the bloc.

Outlook

India could turn into a net exporter in July. Imports remain higher priced than domestic material, and with subdued demand continuing in the domestic market, the gap between overseas-origin material and Indian HRCs may widen. Buying interest will also be tempered by the anti-dumping investigation. However, an increase in imports cannot be ruled out if shipments are procured under the Advanced Authorisation Scheme for re-export as pipes.

Meanwhile, exports are likely to increase m-o-m in July. Although export volumes to Europe are expected to decline under the tighter quota regime, the EU is likely to remain an important market for Indian mills.

The release of country-specific allocations from 1 July provides buyers with greater clarity over available volumes, which should support a gradual recovery in trading activity after the subdued conditions seen in June, albeit within a materially smaller quota framework.

Taken together, these factors suggest that exports are likely to outpace imports during July, potentially allowing India to become a net exporter of HRCs in July 2026.

Leave a Reply