- BF-origin rebar prices decline by INR 1,600/t w-o-w

- HRC market stable on firm fundamentals, policy support

- Mills likely to slash prices in early July on rising inventory pressure

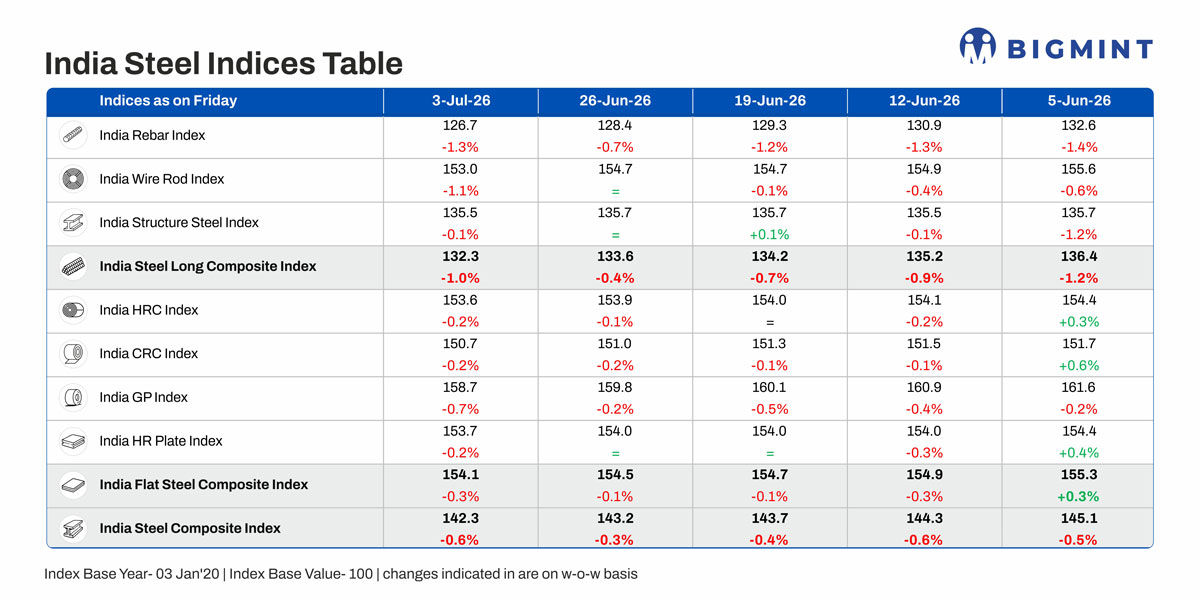

Morning Brief: BigMint’s India steel composite index fell by 0.6% w-o-w, as assessed on 3 July 2026, as domestic steel prices continued to weaken due to seasonal slowdown in construction and fast-developing inventories with mills and distributors. However, as in previous weeks, the pace of decline remained uneven across product categories – long steel prices dropped sharply due to market slowdown and inventory liquidation pressure, while flat steel softened at a much more moderate pace amid the conflicting pulls of policy-related support and market slowdown.

The longs index dropped 1% on-week led by a 1.3% drop in the rebar index, while the flat steel composite index dropped just 0.3%, with HRC declining by 0.2% w-o-w.

Highlights of price movements

Weak downstream sentiment pressures rebar: BigMint’s benchmark assessment for rebar (IS 1786 Fe 550D, 12-32 mm, BF route) was assessed at INR 48,900/t on 3 July against INR 50,500/t on 26 June, down by INR 1,600/t. Prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Higher inventory with distributors kept procurement sentiment cautious at prevailing prices, resulting in a mixed sentiment. Demand remained largely need-based across both retail and project segments. Heavy rainfall, delayed project execution, labour shortages, and temporary restrictions on construction activity in parts of Mumbai (due to water shortages in late June) weighed on the rebar market, with prices in June falling to a six month low.

IF-route rebar prices declined across markets tracking the weakness in billet and sponge iron prices. BigMint’s billet index fell to a seven -month low in early July. Trading activity remained limited as buyers restricted purchases to immediate requirements, while mills and traders offered discounts to stimulate demand amid slow buying activity. Mill inventories were at around 10-15 days.

HRC market remains stable: BigMint’s assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai remained stable w-o-w at INR 58,200/t ($609/t) on 3 July. The benchmark assessment for CRC (IS513, Grade O, 0.9 mm/CTL) was unchanged at INR 65,200/t ($683/t) on 3 July.

Trading activity slowed further last week as procurement was largely limited to immediate requirements, with buyers adopting a need-based approach. Payment collection issues and the onset of monsoons weighed on downstream demand. Unlike long steel demand, which entered its seasonal off-period in June, flat steel demand remained supported by the safeguard duty on imports, continued expansion in manufacturing activity, and the differential with landed cost of imports.

Buyers continued to defer fresh bookings in anticipation of a potential price correction. The prevailing wait-and-watch sentiment was further reinforced by expectations surrounding steelmakers’ price announcements for July, prompting distributors to hold back purchases until greater clarity on pricing emerges.

EU slashes import quotas, export offers drop sharply: Indian HRC export offers to the EU declined by $20/t w-o-w to around $600/t FOB, while offers to the Middle East and Vietnam remained stable.

Export sentiments weakened further as the European Union formally adopted a new steel trade framework which saw a sharp reduction in India’s export quotas to the EU. Indian exporters under the country-wise quota allocations announced by the EU on 30 June have been allocated around 0.59 mnt of HRC annually.

On the other hand, importers in Vietnam are showing subdued interest while logistical disruptions in the Middle East weighing on India’s export prospects.

Bulk HRC imports decline: Bulk HRC imports, as per vessel line-up data, reached around 209,000 t in June, dropping sharply from over 400,000 t in May. The decline in imports undoubtedly offered support to domestic HRC prices. Moreover, thanks to the 11.5% safeguard duty, the differential between imported (from both FTA countries and China) and domestic prices remained in the range of INR 5,700-7,300/t in June.

Chinese HRC prices were at a 20-month high in June. But softening sentiments are prodding major Asian mills to cut prices. Likewise, domestic HRC also softened somewhat in June. Therefore, the differential in July is also likely to be significant, thereby discouraging imports.

Outlook

The domestic market is waiting for list price announcements by the primary mills. It is widely expected that the integrated producers will trim BF-origin rebar prices due to the pressure of mounting inventories and seasonal slowdown in demand.

On the other hand, policy support and strong Chinese prices should have favoured a rollover of domestic HRC prices by the major mills.

However, softening sentiments in China and the rest of Asia, as well as rapidly shrinking export prospects in key markets such as the EU, may put pressure on mills to trim prices marginally.

Although HRC will fare better than rebar, steel prices are expected to edge down across product categories in the coming weeks.

Leave a Reply