- Prices close higher despite mid-week profit booking-led corrections

- SHFE prices dip on weak demand; MCX firms up on need-based buying

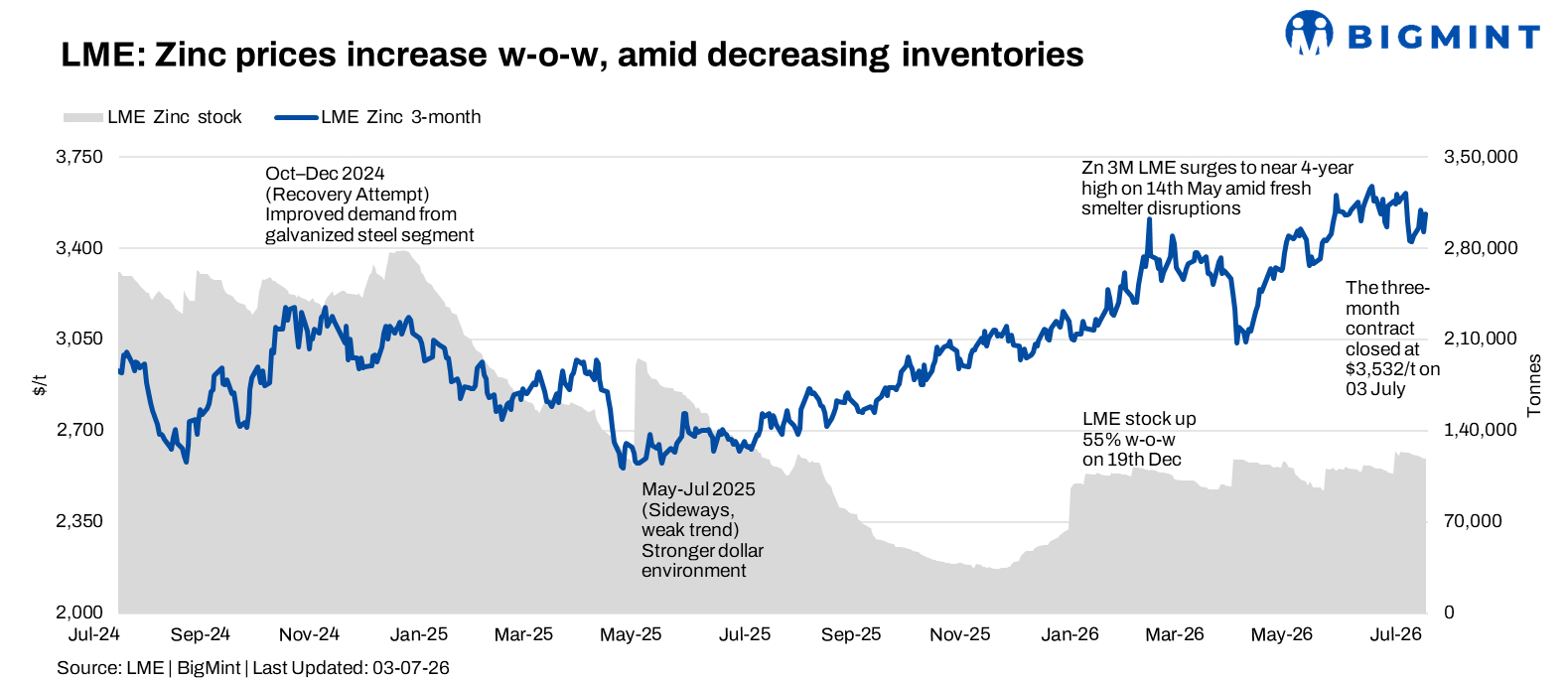

London Metal Exchange (LME) zinc prices inched up during the week ended 3 July 2026, with market participants balancing healthy physical demand against cautious macro sentiment. Although prices witnessed sharp intra-week swings, the market remained resilient and ended the week marginally higher than the previous Friday, supported by continued inventory drawdowns and renewed buying interest towards week-end.

On a w-o-w basis, LME zinc cash settlement prices increased 2.5% to $3,546/t on 3 July from $3,460/t recorded on 26 June. While intermittent corrections weighed on sentiment during the reporting week, improving physical fundamentals and declining exchange inventories helped prices recover from early weakness.

Price trends

LME zinc cash settlement prices opened the week at $3,491/t on 29 June before advancing to a weekly high of $3,565.5/t on 30 June amid stronger buying interest.

However, prices retreated sharply to $3,529/t on 1 July and further to a weekly low of $3,475/t on 2 July as profit-booking and cautious sentiment across the broader base metals complex weighed on the market. Buying interest returned towards the close of the week, lifting prices to $3,546/t on 3 July.

The three-month contract broadly mirrored movements in the cash market. Prices rose from $3,479/t on 29 June to $3,546/t on 30 June before easing to $3,512/t on 1 July and $3,465/t on 2 July. The contract recovered to settle at $3,532/t by week-end, indicating resilient forward market sentiment despite short-term volatility.

Inventory analysis

LME zinc inventories continued their downward trajectory throughout the reporting week, reflecting sustained warehouse outflows.

Stocks declined from 121,300 t on 26 June to 120,525 t on 29 June before falling further to 119,825 t on 30 June. The downward trend continued through the remainder of the week, with inventories easing to 119,200 t on 1 July, 118,950 t on 2 July, and 118,675 t on 3 July.

Overall, exchange inventories declined by 2,625 t w-o-w. The continued drawdown in warehouse stocks provided underlying support to market sentiment, suggesting that physical demand remained sufficiently firm to absorb available supplies despite periods of price volatility.

MCX zinc trends (29 June-3 July)

On the Multi Commodity Exchange (MCX), zinc futures traded within a broad range, largely tracking movements in overseas markets.

The July contract settled at INR 358,350/t on 29 June before strengthening to INR 364,200/t on 30 June as global prices firmed. The contract subsequently eased to INR 361,550/t on 1 July and further to INR 359,750/t on 2 July amid weaker international cues.

Buying interest improved on the final trading session, with the contract rebounding to settle at INR 366,650/t on 3 July, the highest closing level of the reporting week.

Open interest remained relatively stable during the week, rising from 2,434 lots on 29 June to 2,610 lots on 3 July, indicating fresh participation alongside renewed buying interest as prices recovered.

Domestic trading activity remained largely need-based, with consumers closely monitoring international price movements while maintaining cautious procurement amid continued market volatility.

SHFE zinc trends

On the Shanghai Futures Exchange (SHFE), zinc prices inched down during the reporting week as market participants weighed domestic demand expectations against broader macroeconomic uncertainty.

SHFE zinc stood at $3,556/t on 29 June before declining sharply to $3,338/t on 30 June. Prices subsequently recovered to $3,393/t on 1 July, eased marginally to $3,385/t on 2 July, and strengthened further to $3,420/t on 3 July.

The recovery during the latter half of the week reflected improving market confidence, although participants largely remained cautious while assessing the pace of downstream industrial demand in China.

Market updates

Market sentiment remained balanced during the week. While profit-booking and broader macro uncertainty triggered corrections during the middle of the week, sustained declines in LME warehouse inventories continued to provide support to zinc prices. Physical buying remained largely need-based, with adequate material availability preventing aggressive restocking.

In China, market participants continued to monitor downstream demand from the galvanising, infrastructure, and manufacturing sectors. Although buying activity remained selective, improving physical market fundamentals and continued inventory drawdowns helped underpin prices, allowing LME zinc to finish the week comfortably above the key $3,500/t level.

Outlook

BigMint expects LME zinc prices to remain broadly stable in the coming week, supported by declining exchange inventories and stable physical demand, while macroeconomic developments and investor sentiment may continue to generate short-term volatility.

Immediate support is likely around the $3,500-3,530/t range, while resistance is seen near $3,580-3,620/t. Inventory movements, Chinese downstream demand trends, and broader developments across global base metals markets will remain key indicators for zinc’s near-term price direction.

Leave a Reply