- Indonesia RKAB approvals remain key supply variable.

- Chinese stainless demand continues to remain sluggish.

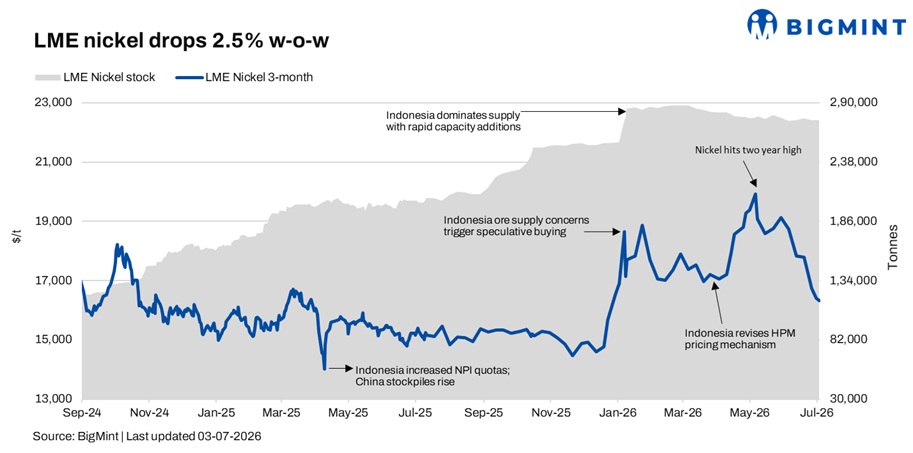

London Metal Exchange (LME) nickel prices remained under pressure during the week ended 3 July 2026. LME three-month nickel futures declined 2.5% w-o-w to $16,330/t from $16,740/t a week earlier, while cash prices fell sharply from a mid-June peak of around $18,545/t to $16,070/t on 2 July. LME inventories remained largely stable at 274,620 t, compared with 274,806 t in the previous week.

Macro factors

Macro factors amplified the downward pressure on prices last week. The US Federal Reserve’s guidance that interest rates may stay elevated bolstered the US dollar, which typically makes dollar‑priced commodities less attractive to overseas buyers and weighs on metal prices; that stronger‑dollar effect likely contributed to nickel’s pullback alongside profit‑taking and softer demand signals from downstream buyers. On the demand side, Chinese stainless‑steel restocking trends remain the primary near‑term driver: weaker restocking or slower stainless output would add to downside risk, while any pick‑up in orders for stainless or EV battery feedstock could quickly tighten balances and reverse the recent decline.

Indonesia output and RKAB in focus

Indonesia’s refined nickel production reached 8,800 t in June 2026, a 10.2% decline month-on-month but a 7.3% increase year-on-year. The six-month cumulative tally from January through June stood at 57,400 t, representing a strong 69.3% year-on-year rise as new HPAL and ferronickel capacity continued to come on line. Reported equipment capacity among Indonesian refined nickel producers is about 10,000 t/month, with utilization running near 88%, and July production is estimated unchanged at 8,800 t up 18.9% year‑on‑year. These figures underscore how rapidly Indonesia’s downstream footprint is expanding, even as month‑to‑month output fluctuates with maintenance and feedstock availability.

A key supply narrative moving into the second half of 2026 is Indonesia’s approved nickel ore production quota (RKAB) for the year, which market sources say has reached the upper end of the government’s annual target. That development has focused attention on whether authorities will grant supplementary allocations in H2. The timing and scale of any additional RKAB approvals will directly affect ore availability for smelters and could materially change the near‑term supply balance. Smaller miners have already felt the impact: PT Central Omega Resources announced plans to seek extra RKAB approvals in July after its quota was cut by 35% year‑on‑year to 1.9 mnt, illustrating how quota moves can quickly tighten feedstock for local refining lines.

Despite ample exchange inventories, Indonesia’s RKAB approvals remain the key upside risk for nickel prices. Meanwhile, Chinese stainless steel production, restocking activity and EV battery demand will continue to dictate near-term consumption. Any improvement in these sectors could support prices, while prolonged weak demand is likely to keep the market under pressure.

Other updates

MMG extends Anglo American nickel acquisition deadline amid EU regulatory review

MMG has extended the completion deadline for its proposed acquisition of Anglo American’s nickel business in Brazil from 30 June to 31 October 2026, after the European Commission moved its merger assessment into a Phase II review. While all other regulatory and transaction conditions have been fulfilled, the deal now awaits EU competition approval. Once completed, the acquisition is expected to strengthen MMG’s presence in the global nickel market and enhance its exposure to battery metals, supporting its long-term growth strategy.

Outlook

Nickel prices are expected to remain volatile in the near term as market participants await clarity on Indonesia’s supplementary RKAB approvals. While stable LME inventories and expanding Indonesian refined nickel production continue to weigh on prices, any delay in additional ore allocations could tighten feedstock availability and provide price support. Recovery in China’s stainless steel demand and EV battery sector will remain the key indicators for the next price direction.

Leave a Reply